This article is authored by MOI Global instructor Mark Walker, a global equity investor and managing partner at Tollymore Investment Partners, based in London.

An investment process is a set of guidelines that govern the behaviour of investors in a way which allows them to remain faithful to the tenets of their investment philosophy, that is the key principles which they hope to facilitate outperformance. An investment process should allow the manager to stay the course in periods of underperformance or other source of self-doubt. It is the process which gives investment managers a better chance of making good decisions consistently though a market cycle. The investment process is a set of inputs that are designed to drive an output – satisfactory investment returns.

Some friends of mine at large asset managers claim that my investment operating system is not a process. The main sources of contention seem to be that a real investment process is easily described, and that it is repeatable. Institutional capital allocators also seem to broadly require that an investment process have this quality of repeatability for a strategy to be investable.

Repeatability is indeed a desirable characteristic, but often repeatable is inappropriately conflated with quantitively led processes, characterised by the use of statistical screens highlighting cheap, out of favour stocks. Users of quant screens, sometimes in the form of proprietary idea generation engines, argue that simply by fishing in a certain pond, they are tipping the odds of achieving a satisfactory investment result in their favour.

There are several issues with this:

- While selecting investment opportunities from a screen may have helped the manager to outperform in the past, there is no guarantee it will in the future, especially considering significant business model changes from the industries of history vs. those of the future.

- Repeatability implies copyability. Predicating a source of investment edge on something that can be replicated tips the odds against you in achieving a satisfactory investment result. The capacity for contrarian thinking is limited by the preponderance of investors using screens as their primary or only idea generation filter.

- Screens miss one of the most compelling sources of mispriced securities: those companies whose reported financials poorly reflect the underlying cash earnings’ power of the business, due to for example high reinvestment rates, inappropriate accounting policies or business model transitions.

While less convinced about the value of stock screens than many in the asset management industry, I do use some basic screens to potentially highlight names that are “cheap and good”, but screens have driven a minority of investment ideas. Most investment ideas are driven by energetic engagement with company filings and transcripts, industry reports, fund manager letters and the authors of these letters in one on one and conference settings, and value investor publications. It is a multi-touchpoint approach that fosters both independent thinking and intelligent, intellectually generous and appropriately aligned collaboration.

Idea generation is an ‘always on’ activity, occasionally accelerated by buyside investment conferences. Recognising an opportunity when one sees it is a more valuable skill than looking for opportunities in an information-rich world. A very concentrated investment portfolio and a global opportunity set afford me the luxury of saying “No” to a significant majority of opportunities at a very early stage. For those ideas which look interesting, brief documentation of their potential investment merits helps to determine how time should be spent on more substantial due diligence efforts.

The research process is bottom-up, one company at a time. Blocks of uninterrupted focus are dedicated to gathering data, facts, logic or other evidence which help me to form an opinion about the company’s economic characteristics and private business value. These characteristics include business simplicity, capital structure, track record, competitive positioning, reinvestment opportunities, stewardship and valuation.

There are no predetermined ways that I am seeking to form a positive conclusion on the company’s business characteristics. I am looking for competitively strong businesses which ideally have avenues for profitable redeployment of capital for a long time, whose uses and sources of finance are appropriate for the business model, and whose management is properly incentivised to make the best capital allocation decisions that will create the most long-term value for owners. Each potential investment candidate is assessed at face value and using available facts. This is one step removed from saying that I am looking for capital light platform businesses with recurring revenues and high insider ownership, for example. The capital light, recurring revenue nature of the business may well be desirable, but there are other ways to create high quality business models and sustain competitive strength. Likewise, high insider ownership may or may not satisfy the requirement that managers are aligned with owners. Each business is assessed on its merits, from a blank sheet of paper.

The result is a portfolio that is concentrated with regards to the number of holdings but is diverse in terms of geographic and industry end markets, business models and organisational and ownership structures. All portfolio companies have strong competitive positions and enjoy high barriers to entry that should sustain supernormal profits on existing assets for a long time. They differ in the extent to which they can redeploy capital into growing the normal earnings’ power of the business, and the cost of that intrinsic value growth. Holdings can be grouped into three broad categories: capital light compounders, reinvestment moats, and legacy moats. Broadly speaking, the multiple of owner earnings I am willing to pay for a capital light compounder is higher than that for a reinvestment moat, which is higher than that for a legacy moat.

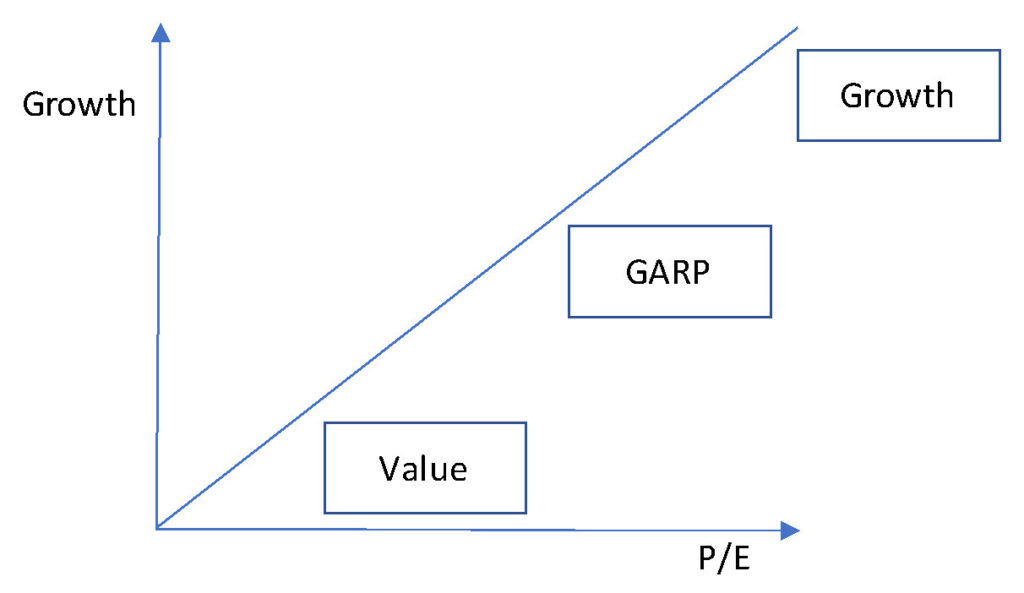

I have never found the concept of investing according to ‘style factors’ intuitive. Fund managers seem to explicitly or implicitly categorise themselves as ‘value’, ‘growth’, or ‘GARP’. By doing so they are placing themselves at various points on the PEG curve below. Investors are willing to pay higher multiples for businesses which can grow their earnings faster. The massive shortcoming in this framework is the lack of consideration for the cost of the company’s growth. If company A and company B both grow earnings at 10% pa, we should not be willing to pay the same multiple if company A can achieve that growth with modest capital reinvested, while company B needs to reinvest substantial portions of prior earnings. An investment approach focused on returns on capital allows an investment manager to consider the cost of earnings’ growth in estimating private business value.

There is a growing chorus of deep value investors lamenting the underperformance of their investment ‘style’ and calling a bubble in moats and compounder investing. Whether or not such a bubble exists, this bottom up, first principles process helps to safeguard against being on the wrong side of that bubble bursting. I have visited many quality-focused investment conferences over the last few years; most of the investor discussion seems to be oriented around deep value and capital cycle investment themes and ideas. The bottom line is that there just aren’t that many high-quality businesses, let alone attractively priced ones available on the public market. The discovery of mispriced great companies is a perennially tough challenge, and I am trying to find 10-15 in a universe of tens of thousands. For a diversified manager this challenge is immeasurably more difficult.

Estimating private business value typically involves using cumulative qualitative research to estimate the normal earnings’ power and achievable reinvestment rate of the business, and the incremental cash returns that could be earned on redeployed capital. The output of this is a range of IRRs that could be enjoyed at current prices. Ideally a conservative appraisal would lead to an IRR in the high teens. The goal of the portfolio management strategy is then to augment this return to equity owners by occasionally and sensibly responding to stock market volatility by averaging down or up in response to material market moves inconsistent with changes in fundamental business prospects. This is one of the major advantages of public vs. private equity investing. Public equity volatility can lower risk of permanent capital loss by allowing us to lower our average purchase price and avoids the temptation of employing leverage to juice returns. This approach to public market investing means that volatility is welcomed, and no efforts are made to smooth investment returns. Risks of permanent capital impairment are mitigated by avoiding leverage at the portfolio and company levels, employing a long only strategy, and averting intrinsic value erosion by investing in high quality businesses.

Valuation may be a reason to sell an entire position, but unless extreme overvaluation occurs, it is more likely to drive portfolio rebalancing decisions. Reasons to dispose of entire positions are more typically the result of fundamental shifts that undermine my perception of the company’s competitive position, or subsequent evidence which refutes my prevailing view of a business’s or management’s quality.

So, the key aspects of an investment process govern idea generation, investment research and portfolio management. Overarching these three pillars is a belief that execution is everything. A sensible long term, business owner investment philosophy is of no use if the investing ecosystem is a barrier to faithfully executing a thoughtful investment process. A great investing ecosystem must cultivate a bi-literate brain; one capable of navigating data and filtering noise; and one capable of deep work in a digital era. It seems to me the obvious source of investment edge is behavioural. Constructing a low-key physical working environment free from distraction and conducive to independent thinking, and having an investment philosophy and investor base matched to an investment manager’s temperament are crucial determinants of a long-term successful outcome.

About The Author: Mark Walker

Mark Walker is the Managing Partner of Tollymore Investment Partners, a private investment partnership investing in a small number of exceptional businesses to compound clients’ capital over the long term. Prior to founding Tollymore Mark was a global equity investor for Seven Pillars Capital Management, a long-term global value investing firm based in London. Mark joined Seven Pillars from RWC Partners, where he was part of a two-person team managing a newly launched, long term global equity fund. Prior to that Mark worked as an investment research analyst for Goldman Sachs and Redburn Partners. He is a qualified chartered accountant, and graduated from Edinburgh University with a First Class MA Honours degree in Economics, graduating first in his class.

More posts by Mark Walker