This article is authored by MOI Global instructor Todd Wenning, a senior investment analyst at Ensemble Capital Management, based in Burlingame, California. Visit Ensemble’s Intrinsic Investing website for additional insights.

Investors who’ve studied the works of Warren Buffett and Peter Lynch know that so-called “boring” stocks can present wonderful investment opportunities.

There’s something to it. In Lynch’s One Up on Wall Street, for example, he writes, “Blurting out that you own Pep Boys won’t get you much of an audience at a cocktail party, but whisper ‘GeneSplice International’ and everybody listens.”

Boring companies typically don’t make for media darlings. Often there’s not much variance in quarter-to-quarter or year-to-year growth – due to high recurring revenue, pricing power, etc. – so there isn’t a lot to debate.

In a 2013 paper, the British asset management firm, Fundsmith, set out to explain how and why boring companies are consistently undervalued.

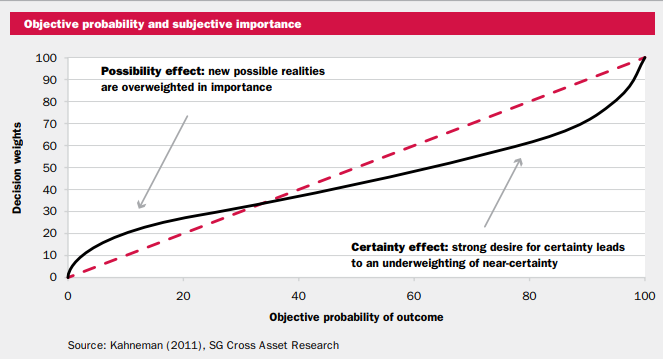

As the below chart shows, people tend to be overconfident in low-certainty events (e.g. lottery tickets) and underconfident in higher-probability events (60-80% certainty). As certainty approaches 100% (e.g. a Treasury bond), people become more correctly confident.

Source: Fundsmith.

Source: Fundsmith.

Many high-quality, low-volatility stocks find themselves in the 60-80% certainty category. As Fundsmith wrote, these stocks “have regular bond like returns and low share price volatility but they are still stocks with uncertainty about share price and dividend payments whereas bonds have the relative certainty of redemption values and coupons.”

Put another way, this set of businesses is about as fundamentally certain as you can get in the market, but investors have systematically underinvested in them relative to their level of certainty.

To be sure, patient investors in boring stocks have been handsomely rewarded. From June 1990 through mid-July 2019, the S&P 500 low volatility index outperformed the overall S&P 500 Index by about 100 basis points per year (11% vs. 10% CAGR).

Source: Bloomberg, as of July 16, 2019. Normalized, total returns.

Source: Bloomberg, as of July 16, 2019. Normalized, total returns.

Now, during most bull markets, you would expect economically-sensitive, high-volatility stocks to outperform low-volatility stocks, as they did from December 2002 to October 2007, as measured by the S&P 500 high beta index (purple line) vs the Low Volatility index (white line).

Bloomberg, as of July 17, 2019. Normalized, total returns.

Bloomberg, as of July 17, 2019. Normalized, total returns.

Yet here we are today, riding a 10-year bull market and hitting all-time highs, and low-volatility companies continue to crush high beta names.

Bloomberg, as of July 19, 2019. Normalized, total returns.

Bloomberg, as of July 19, 2019. Normalized, total returns.

Don’t get us wrong – at Ensemble, we also love boring, defensive companies flying under Wall Street’s radar. They often have economic moats and get stronger during recessions.

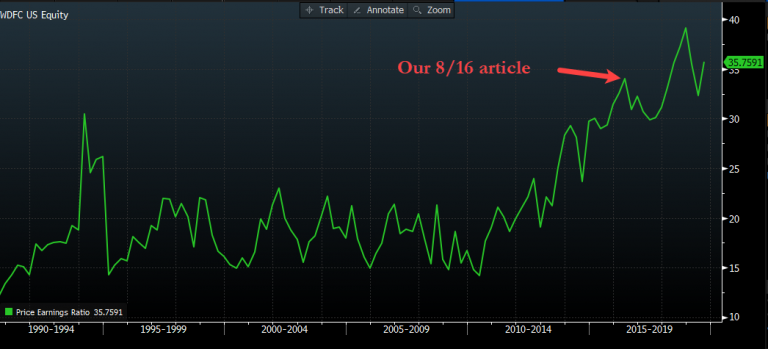

Yet some of these companies’ valuations have been challenging to justify. In August 2016, for instance, we wrote about former holding WD-40 being a case study of the “bubble” in safe stocks.

Remarkably, since we wrote that post three years ago, WD-40 has further expanded its already-lofty P/E multiple and outperformed the S&P 500. In 2016, we would have considered this a low probability outcome, but here we are.

Bloomberg, as of July 16, 2019.

Bloomberg, as of July 16, 2019.

WD-40 isn’t alone. As of this writing, the broader S&P 500 Low Volatility Index P/E (blue line) is four full turns above the S&P 500 Index P/E (brown line).

Bloomberg, as of July 16, 2019.

Bloomberg, as of July 16, 2019.

So what might be going on here? Why are boring stocks trading with such high multiples?

We offer three suggestions: First, as we argued in our 2016 WD-40 article, investors might be placing a premium on “safer” equities due to bad memories from the financial crisis. Having experienced 30%-50%-plus drawdowns in 2008 and 2009, many investment managers don’t want to mis-time cyclical stocks and look foolish when their peers are hunkering down in safe stocks. Some amount of herding behavior is at play.

Second, index funds, ETFs, and quantitative screens have changed the game. While active fund managers in Lynch’s day (the 1980s) were worried about bad window dressing by holding boring companies, machines are narrative agnostic. Machines could care less if Stock A is boring or exciting – they see businesses as a set of data points. Because boring businesses often have attractive fundamentals, they might get more demand from passive investors seeking quality, low-volatility, and/or dividend yield factors than they otherwise would with active managers.

(As we researched this article, we found it notable that the S&P 500 Low Volatility and High Beta Indexes were launched in April 2011, just two years after the market bottom.)

Third, the continuation of the low interest rate environment. We think the debate between a return of the old normal or getting stuck in the New Normal is a critical one for investors to consider. If we are moving back to an Old Normal (a “normalization” of inflation, higher rates, etc.) then boring stocks are massively overvalued; however, if we’re stuck in a New Normal (persistent low rates, low inflation, etc.), boring stocks, along with the rest of the market, may be fairly- to undervalued, albeit – and this is a key point/trade-off – with expected equity returns below long-term historical averages.

Indeed, if you’re buying low beta/boring stocks at currently-lofty valuations, you’re making an implicit bet that rates will remain low and that future equity returns will be lower than historical averages. We’ve found we’d have to drop our cost of equity assumptions well below 9% to make current valuations work on some low-beta/boring companies.

All three factors are at play, with interest rates playing the largest role in boring stock valuations. In a low rate environment, the opportunity cost for that extra 20-30% certainty (illustrated in the chart earlier in this post) drops. If you’re getting 2% on 10-year government bonds with 100% certainty, you’re more willing to increase your bet on 70-80% certainty in the hope of getting 5-7% annualized returns. The systematic undervaluation of 70-80% certainty names gets “corrected” in a low-rate environment.

Our opinion is that we’re more likely to return to Old Normal than New Normal, though we’ve heard compelling arguments for both cases.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About The Author: Todd Wenning, CFA

Todd is a senior investment analyst at Ensemble Capital. Before joining Ensemble, Todd was an analyst at Johnson Investment Counsel, where he worked on the firm’s SMID cap strategy. Prior to that, Todd was a sell-side analyst at Morningstar, where he led Morningstar’s equity stewardship methodology and covered companies in the basic materials, industrials, and consumer sectors. Earlier in his career, Todd worked for The Motley Fool, SunTrust Asset Management, and Vanguard. He holds a BA in History from Saint Joseph’s University in Philadelphia and the Chartered Financial Analyst designation.

More posts by Todd Wenning, CFA