This article by Michael Lee is excerpted from a letter of Hypotenuse Capital.

Perhaps you have wondered why our Partnership has such a concentrated investment approach (currently, our five largest investments constitute about 65% of the Fund’s net assets). I want to spend some time discussing why we do not diversify as much as other investment funds; I believe this is an important aspect of our investment strategy.

Our Fund aims to outperform the broader equity marketplace over long periods of time and the only way to do that is by selecting a subset of the market that we believe will outperform the average. In other words, if one is trying to outperform the S&P 500 Index, one cannot do so by owning all 500 stocks in the index but only by selecting some subset of that index. This is, of course, an obvious truism, but it is an important starting point for reasons that should become clearer below.

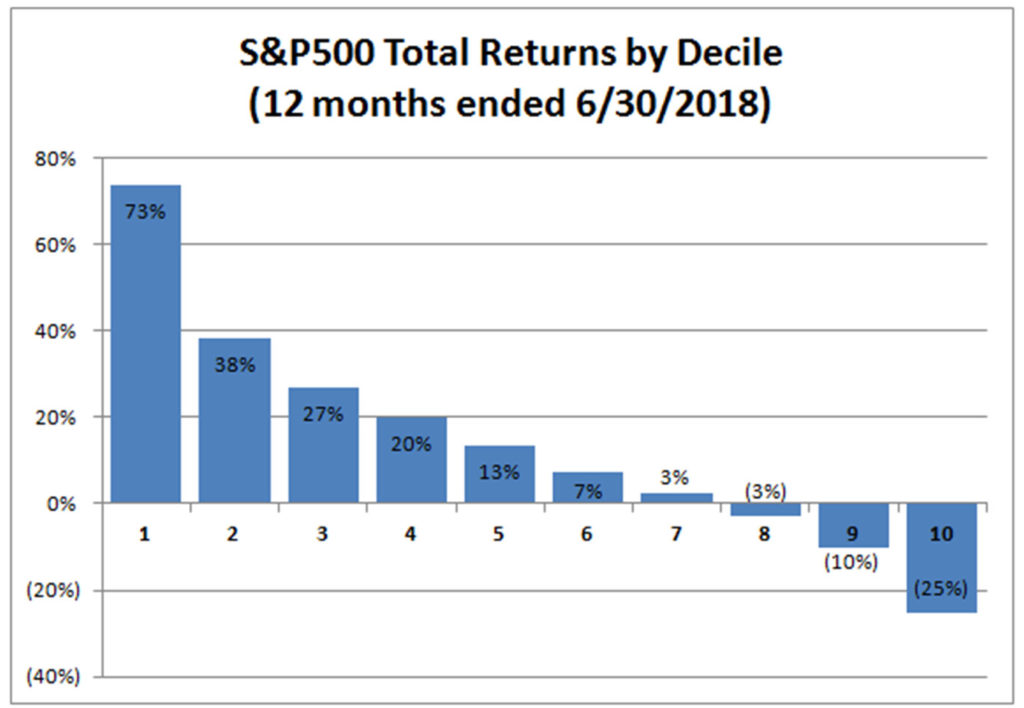

The chart below illustrates the performance of the S&P 500 components over the twelve months ended June 30, 2018 by decile.

Source: CapitalIQ and Hypotenuse Capital analysis

Now, it seems reasonable that if one wants to assemble a portfolio that outperforms the index, one has to select a portfolio of securities with as many individual selections from the left hand side of the chart, i.e., the first five deciles, and as few as possible from the bottom five deciles or the right hand side of the chart. How hard is it to pick a portfolio of stocks from a given part of the chart, say just the top decile?

To get at this question we can turn back to a little bit of probabilistic math that we all learned (or at least “were taught”) in high school. We can reframe the question like the “marbles in a bag” probability problems you may remember from back then. For example, imagine that you have a paper bag filled with 500 marbles of which 50 are red and all the other marbles are blue. If you reach into the bag and draw a marble at random, what are the odds that it will be red (i.e., top decile)? In this scenario, the math works out relatively simply to 10% or one out of every ten attempts.

To get at this question we can turn back to a little bit of probabilistic math that we all learned (or at least “were taught”) in high school. We can reframe the question like the “marbles in a bag” probability problems you may remember from back then. For example, imagine that you have a paper bag filled with 500 marbles of which 50 are red and all the other marbles are blue. If you reach into the bag and draw a marble at random, what are the odds that it will be red (i.e., top decile)? In this scenario, the math works out relatively simply to 10% or one out of every ten attempts.

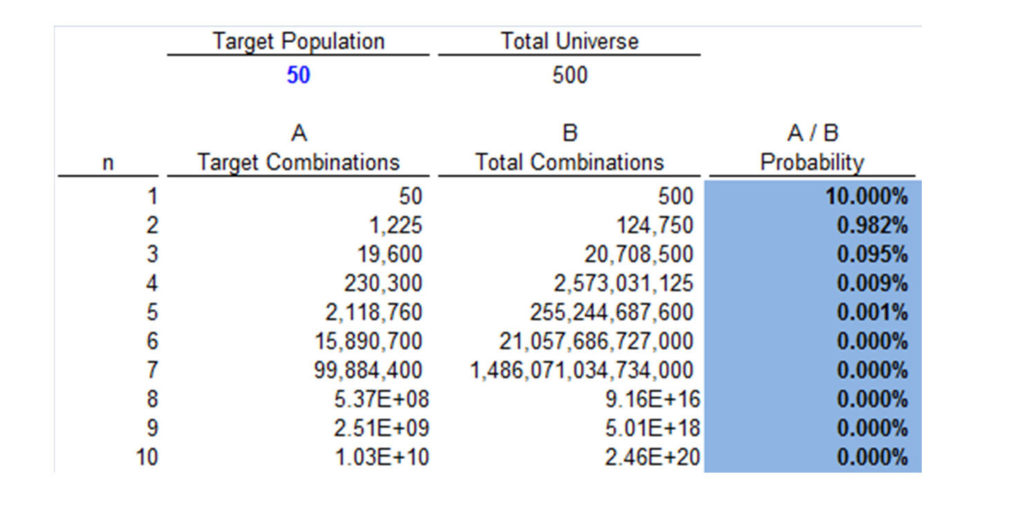

What happens to our odds if we reach into the bag and randomly select two marbles? What are the odds that both marbles will be red? What happens if we select ten marbles? The math starts to get a little complicated and involves combinations and factorials, but I will spare you the detailed algebra. The probability of drawing two marbles that are both red are about 1% or one in a hundred. The probability of drawing ten marbles at random and having them all be red is about one in one hundred billion. Statistically speaking, you are more likely to win the lottery than you are to randomly pick ten red marbles from this bag or ten top decile stocks from the index.

Table 1: Odds of a Randomly Selected Portfolio Being All Top Decile Stocks Based on Portfolio Size (n)

You might note in the table above that the odds of getting all red marbles get worse as you increase the number of marbles (n) you draw from the bag. This is somewhat intuitive; you are more likely to flip a coin and get heads once than you are to flip a coin ten times and get ten heads in a row. It is important to notice that the odds not only get worse, they get worse very rapidly. The probability of drawing all red marbles decays exponentially, not linearly, with increasing (n).

One can improve the odds by changing some parameters. For example, if one was just targeting “above average” performance of stocks, that would be like assuming that 250 marbles in the bag of 500 were red marbles. In this case, the odds of drawing 10 red marbles are about one in one thousand. However, changing this parameter means accepting lower returns and therefore takes us farther away from our goal of outperforming the index. Ultimately, the number of stocks in a portfolio (n) is one of the most important drivers of the probability that that portfolio can outperform the index. Consequently, ceteris paribus, concentrated portfolios are more likely to outperform the index than are diversified ones.

The tradeoff here, of course, is variance. A single stock “portfolio” where the only investment files for bankruptcy is obviously a huge disaster whereas a portfolio made up of one hundred equally sized investments will not suffer nearly as greatly if any one of those investments fares badly. Hence, many investors have a natural and understandable inclination to diversify their portfolios and mitigate the risk of anything going wrong with any single investment. However, risk and returns go hand in hand; the more one diversifies a portfolio, the less likely it is to outperform the index. Trying to outperform the index with a broadly diversified portfolio is a Herculean task that runs counter to the fundamental principles of mathematics; it is a bit like trying to land a rocket on Mars without factoring in gravity.

Fortunately, when it comes to picking stocks, we don’t have to pick blindly from a bag of marbles. The world of stocks and investing is rich with information and, practically speaking, there is a limitless amount of data that one can use to research the companies, products, and people behind stocks. It should be possible to use this vast amount of data and information to analyze stocks and identify which ones are more likely to perform well than not, thus allowing us to filter out blue marbles from the bag and increasing our odds of picking red marbles.

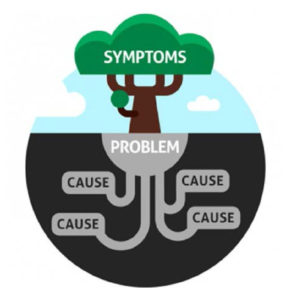

The question then becomes, what protocol or algorithm does one use to screen out all the blue marbles and keep the red ones? This is a crucial factor for investing success. If it was as simple as just buying stocks that went up in the past, then success in investing would be a trivial matter; everyone would be able to do it. I have found that many “fundamental” investment analysts spend a lot of time obsessing over short-term changes in a company’s financial performance. They ask CEOs why revenue is going up or down in a particular quarter, or why profit margins are going up or down. The issue with these types of questions is that they focus on the symptoms and outcomes of business performance but not the core causes. Growth and margins are indicators of business health but not the cause of good business health itself. If we want to identify stocks that will perform well, we should seek to identify the root cause of what makes those stocks successful.

The question then becomes, what protocol or algorithm does one use to screen out all the blue marbles and keep the red ones? This is a crucial factor for investing success. If it was as simple as just buying stocks that went up in the past, then success in investing would be a trivial matter; everyone would be able to do it. I have found that many “fundamental” investment analysts spend a lot of time obsessing over short-term changes in a company’s financial performance. They ask CEOs why revenue is going up or down in a particular quarter, or why profit margins are going up or down. The issue with these types of questions is that they focus on the symptoms and outcomes of business performance but not the core causes. Growth and margins are indicators of business health but not the cause of good business health itself. If we want to identify stocks that will perform well, we should seek to identify the root cause of what makes those stocks successful.

Although there are many reasons why a stock might go up, I would like to propose a simple framework that I believe will lead to a higher probability of success in stocks. I believe that stocks tend to perform well when the underlying business is thriving. This implies that the business has satisfied customers who purchase its products and/or services. This would suggest that the company offers high quality products and services at compelling prices. A company is more likely to provide good products and services if it has passionate employees who care about the customer and the quality of their work. It is easier to recruit and retain such employees when there is a strong team culture that promotes engagement and collaboration amongst its members. A strong culture is often the handiwork of an exceptional and visionary leader who sets the tone for the organization and gets everyone moving in the same direction.

This “root cause analysis” for successful investing is simple and perhaps rudimentary. Yet, in my years in finance and investing I have come across very few people in the securities industry who think this way. Nonetheless, I find it difficult to imagine that if one follows this line of logic and invests accordingly that the outcome will be disappointing over long periods of time. For this reason, the Hypotenuse Capital mission is “To find outstanding companies led by exceptional individuals and invest intelligently in them.”

By focusing on companies that have strong leaders and cultures, we hope to identify businesses that have the best chances of thriving over the long run. In other words, we think these kinds of businesses are most likely to be the red marbles in the bag that lead to superior investment performance over time.

Importantly, the marble in the bag problem is compounded by portfolio turnover. Picking a new stock portfolio is like putting all the marbles in the bag again and trying to pick 10 red ones from scratch. Hence, higher frequency turnover reduces the odds of producing good results. Consequently, we aim to make long duration investments and change them infrequently; we’re trying to pick businesses that will do well not just over the next day, quarter or year, but over three, five or even thirty years. We focus on finding businesses with long runways for future growth. We look for companies with durable competitive advantages that help them widen the gap between them and their competition over time. Cheetahs are the fastest sprinters on the planet but only over short distances. Gazelles can survive cheetah attacks because they are more nimble and can outlast a cheetah running over long distances. We’re looking for gazelles.

Importantly, the marble in the bag problem is compounded by portfolio turnover. Picking a new stock portfolio is like putting all the marbles in the bag again and trying to pick 10 red ones from scratch. Hence, higher frequency turnover reduces the odds of producing good results. Consequently, we aim to make long duration investments and change them infrequently; we’re trying to pick businesses that will do well not just over the next day, quarter or year, but over three, five or even thirty years. We focus on finding businesses with long runways for future growth. We look for companies with durable competitive advantages that help them widen the gap between them and their competition over time. Cheetahs are the fastest sprinters on the planet but only over short distances. Gazelles can survive cheetah attacks because they are more nimble and can outlast a cheetah running over long distances. We’re looking for gazelles.

Furthermore, we use our research to screen out potential disasters. For example, by avoiding companies with high levels of debt we can reduce the risk of insolvency and bankruptcy as an outcome in our investment portfolio. We look for management teams with high integrity and who treat their employees, suppliers and customers well. When all the stakeholders in a business benefit, everyone wants the business to succeed. Conversely, companies that treat their employees, suppliers or customers poorly attract competition, lawsuits, and regulators, i.e., things that imperil companies; so we avoid companies that behave in these ways. Through careful selection, we can mitigate the risks inherent in investing in a concentrated portfolio. We can’t eliminate the risk of short-term volatility of any single security in our portfolio but we can minimize the risk of permanent capital impairment from any one given investment.

Furthermore, we use our research to screen out potential disasters. For example, by avoiding companies with high levels of debt we can reduce the risk of insolvency and bankruptcy as an outcome in our investment portfolio. We look for management teams with high integrity and who treat their employees, suppliers and customers well. When all the stakeholders in a business benefit, everyone wants the business to succeed. Conversely, companies that treat their employees, suppliers or customers poorly attract competition, lawsuits, and regulators, i.e., things that imperil companies; so we avoid companies that behave in these ways. Through careful selection, we can mitigate the risks inherent in investing in a concentrated portfolio. We can’t eliminate the risk of short-term volatility of any single security in our portfolio but we can minimize the risk of permanent capital impairment from any one given investment.

There are some natural implications of our approach to investing. Our process yields a very limited number of investable ideas at any given point in time. Consequently, we expect ourselves: (a) to be extremely patient and wait for “fat pitches” and, (b) to swing with conviction when those pitches come. We would rather invest in a single exceptional idea than spread ourselves thinly over a hundred marginal ones. Our returns have been and will be volatile. I believe that, if we stick to this approach consistently, the results will be very satisfactory over time.

Disclaimer: THE INFORMATION PRESENTED HEREIN REPRESENTS THE VIEWS OF HYPOTENUSE CAPITAL MANAGEMENT, LLC (“HCM”) AND IS NOT TO BE CONSIDERED INVESTMENT ADVICE. NOTHING HEREIN SHOULD BE CONSIDERED A RECOMMENDATION TO PURCHASE OR SELL ANY PARTICULAR SECURITY OR OTHER FINANCIAL INSTRUMENT. THERE CAN BE NO ASSURANCE THAT ANY SECURITIES DISCUSSED HEREIN WILL REMAIN IN HYPOTENUSE CAPITAL PARTNERS, LP’S (THE “FUND”) PORTFOLIO OR, IF SOLD, WILL NOT BE REPURCHASED. FURTHERMORE, HCM MAY SEEK TO ADD TO THE FUND’S POSITIONS IN THE SECURITIES DISCUSSED HEREIN, OR HEDGE AGAINST SUCH POSITIONS. THE SECURITIES DISCUSSED IN THIS DOCUMENT DO NOT REPRESENT THE FUND’S ENTIRE PORTFOLIO AND MAY REPRESENT ONLY A SMALL PERCENTAGE OF THE FUND’S PORTFOLIO HOLDINGS. IT SHOULD NOT BE ASSUMED THAT THE HOLDINGS DISCUSSED IN THIS DOCUMENT HAVE BEEN OR WILL BE PROFITABLE, OR THAT RECOMMENDATIONS MADE IN THE FUTURE WILL BE PROFITABLE OR WILL EQUAL THE INVESTMENT PERFORMANCE OF THE SECURITIES DISCUSSED HEREIN. MOREOVER, THE RISK LIMITS AND HEDGES ON THE POSITION ARE NOT DISCLOSED. THIS DOCUMENT, WHICH IS BEING PROVIDED ON A CONFIDENTIAL BASIS, SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF ANY OFFER TO BUY WHICH MAY ONLY BE MADE AT THE TIME A QUALIFIED OFFEREE RECEIVES A CONFIDENTIAL PRIVATE OFFERING MEMORANDUM (THE “MEMORANDUM”) OF THE FUND, WHICH CONTAINS IMPORTANT INFORMATION (INCLUDING INVESTMENT OBJECTIVE, POLICIES, RISK FACTORS, FEES, TAX IMPLICATIONS AND RELEVANT QUALIFICATIONS), AND ONLY IN THOSE JURISDICTIONS WHERE PERMITTED BY LAW. IN THE CASE OF ANY INCONSISTENCY BETWEEN THE DESCRIPTIONS OR TERMS IN THIS DOCUMENT AND THE MEMORANDUM, THE MEMORANDUM SHALL CONTROL. THESE SECURITIES SHALL NOT BE OFFERED OR SOLD IN ANY JURISDICTION IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL UNTIL THE REQUIREMENTS OF THE LAWS OF SUCH JURISDICTION HAVE BEEN SATISFIED. THIS DOCUMENT IS NOT INTENDED FOR PUBLIC USE OR DISTRIBUTION. WHILE ALL THE INFORMATION PREPARED IN THIS DOCUMENT IS BELIEVED TO BE ACCURATE, HCM MAKES NO EXPRESS WARRANTY AS TO THE COMPLETENESS OR ACCURACY, NOR CAN IT ACCEPT RESPONSIBILITY FOR ERRORS, APPEARING IN THE DOCUMENT. AN INVESTMENT IN THE FUND IS SPECULATIVE AND INVOLVES A HIGH DEGREE OF RISK. OPPORTUNITIES FOR WITHDRAWAL/REDEMPTION AND TRANSFERABILITY OF INTERESTS ARE RESTRICTED, SO INVESTORS MAY NOT HAVE ACCESS TO CAPITAL WHEN IT IS NEEDED. THERE IS NO SECONDARY MARKET FOR THE INTERESTS AND NONE IS EXPECTED TO DEVELOP. AN INVESTOR SHOULD NOT MAKE AN INVESTMENT, UNLESS IT IS PREPARED TO LOSE ALL OR A SUBSTANTIAL PORTION OF ITS INVESTMENT. THE FEES AND EXPENSES CHARGED IN CONNECTION WITH THIS INVESTMENT MAY BE HIGHER THAN THE FEES AND EXPENSES OF OTHER INVESTMENT ALTERNATIVES AND MAY OFFSET PROFITS. THERE IS NO GUARANTEE THAT THE INVESTMENT OBJECTIVE OF THE FUND WILL BE ACHIEVED. MOREOVER, THE PAST PERFORMANCE (IF ANY) OF THE INVESTMENT TEAM SHOULD NOT BE CONSTRUED AS AN INDICATOR OF FUTURE PERFORMANCE. ANY PROJECTIONS, MARKET OUTLOOKS OR ESTIMATES IN THIS DOCUMENT ARE FORWARD LOOKING STATEMENTS AND ARE BASED UPON CERTAIN ASSUMPTIONS. OTHER EVENTS WHICH WERE NOT TAKEN INTO ACCOUNT MAY OCCUR AND MAY SIGNIFICANTLY AFFECT THE RETURNS OR PERFORMANCE OF THE FUND. ANY PROJECTIONS, OUTLOOKS OR ASSUMPTIONS SHOULD NOT BE CONSTRUED TO BE INDICATIVE OF THE ACTUAL EVENTS WHICH WILL OCCUR. ANY PROJECTIONS, MARKET OUTLOOKS OR ESTIMATES IN THIS DOCUMENT ARE FORWARD LOOKING STATEMENTS AND ARE BASED UPON CERTAIN ASSUMPTIONS. ANY PROJECTIONS, OUTLOOKS OR ASSUMPTIONS SHOULD NOT BE CONSTRUED TO BE INDICATIVE OF THE ACTUAL EVENTS WHICH WILL OCCUR.

About The Author: Michael Lee

Mike founded Hypotenuse Capital Management in 2013. Previously, he was a partner at Royal Capital Management, a multi-billion dollar investment manager in New York. Prior to Royal, Mike was a private equity associate at Parthenon in Boston and an investment banking analyst at Bear Stearns in New York.

More posts by Michael Lee