This article is authored by MOI Global instructor Steve Gorelik, portfolio manager at Firebird Management, based in New York.

Headlines:

“Sistema shares dive after Russian court freezes assets – CNBC.com”

“Law firm accuses ENRC of bribes, sanctions-busting and overpayment”

“Russia Laundered Millions via Danske Bank Estonia”

“Graham, Menendez crafting bill to crack down on Russia”

Eastern Europe has for the last two decades featured daunting headlines that would keep most reasonable people away from its capital markets. The Eastern European equity total return index is still more than 40% below its 2008 peak, and there are numerous current concerns. These include the authoritarian tendencies of various governments, and Western sanctions on Russia.

We at Firebird Management have been investing in the region for over 24 years and have seen it develop from newly independent countries gingerly entering the path of capitalism to diversified, vibrant economies prepared to face the challenge of economic cycles. Over this time, despite corrections in 1994, 1998, 2001, 2008, 2012, and 2014, our investors have been compensated for the volatility with generous returns for those invested over the longer term.

Below are a few reasons why we believe the current opportunity is as good as any that we have seen in our time investing in the region.

High-Quality Growth

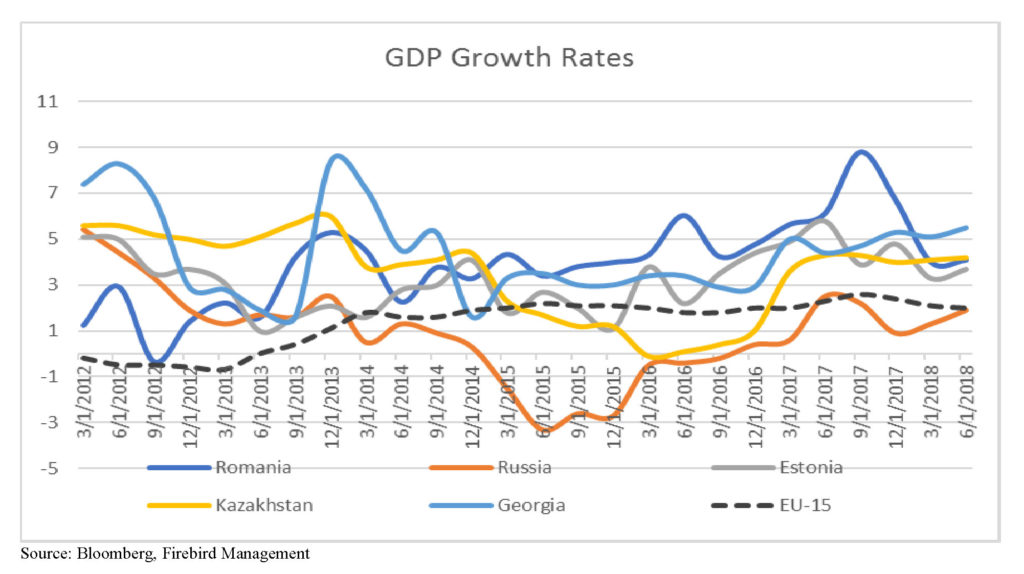

Thanks to highly educated populations, increasingly globalizing economy, and low starting point, the EU convergence part of Eastern Europe (i.e., CE3, Baltics, Balkans) have been consistently generating GDP growth 2-3% above Western Europe. Countries like Romania and Poland serve as a vital part of the supply chain for companies in Western Europe. Starting as manufacturing hubs, these countries are increasingly looked upon as service, R&D and back office centers for larger companies.

While the region has been growing for some time, the structure of growth has changed. Prior to the 2008 crisis, 6-7% annual increases in GDP were driven by foreign liquidity pumped in via the banking systems, and high current account deficits used to finance consumption.

When liquidity left the markets in 2008, the result was severe recessions, with GDP in some countries falling as much as 15%. In response, companies and governments cut spending, improved efficiencies, and cracked down on corruption that had prevented them from accessing EU structural funding. They were therefore able to build a base for the next phase of growth that we see today. As for Russia, corporates and the government refinanced much of their foreign currency borrowing into rubles, while floating the currency.

2018 brought higher global interest rates and with them a renewed bout of volatility in emerging markets dependent on foreign fund flows. Unlike Turkey, Argentina, and South Africa, the countries where we invest have balanced fiscal accounts and fund any current account deficits from stable sources such as FDI, tourism, and remittances. They have proven much more resilient.

Improved Corporate Governance

Despite the occasional negative headline, the overall quality of corporate governance has improved dramatically. Twenty-five years ago, after a half century in a centrally planned system, founders were starting companies from scratch in an unstable economic environment. The skill set required to launch a business in such conditions was different from the one it takes to succeed in a small open economy connected to global networks. In Russia as well, by now a new generation of mostly foreign educated managers has replaced the Red Directors who were in charge in the mid-1990’s.

As economies and businesses developed, so did business leaders. Owners started seeing the benefit of reinvesting profits in their companies instead of their offshore accounts. Running a clean company makes it easier to resist predation by corrupt government officials and others. Owners are also starting to see the wealth effect from higher market multiples of their companies.

The companies are also becoming better at allocating capital. Gone are the days of global empire building. Since 2008 easy funding for such projects has been hard to come by. As a result, companies have retrenched around their core competencies and started focusing on ROIC in their capital allocation decisions.

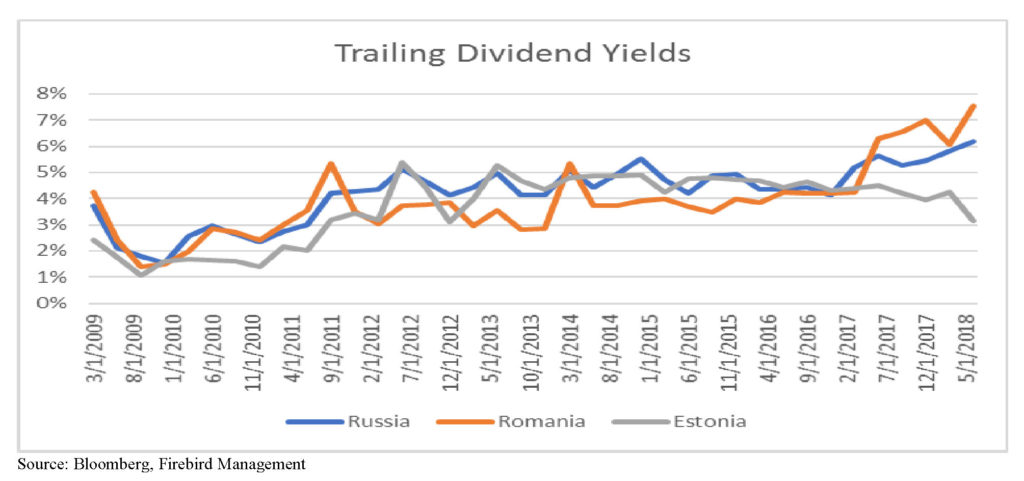

Better capital allocation decisions drive better returns for shareholders. Since 2009, the dividend yields of regional indices has increased dramatically, with many of the largest companies paying 6-8% dividends. The Russian RTS Index currently yields close to 6% while trading at 5.9x P/E. In 2003, when the Russian market was trading at similar valuations, the dividend yield was below 2%.

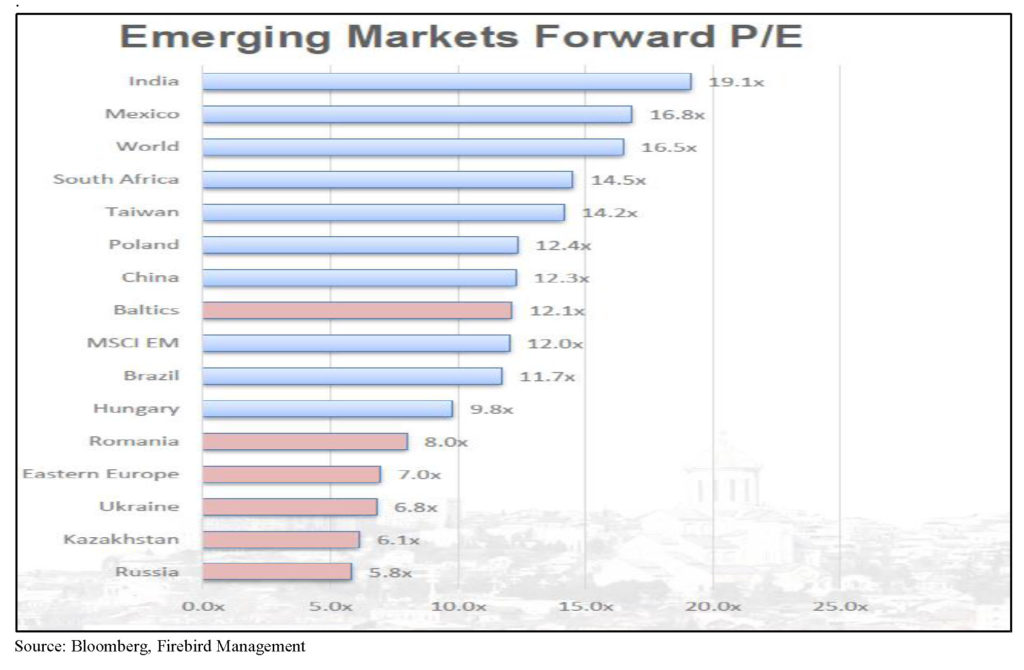

Cyclically Low Valuations

While the world’s equity markets have seen significant multiple expansion over the last few years, the additional liquidity that drove this rerating has largely passed by Eastern Europe. Most of the regional indices are still trading firmly in single-digit P/E range.

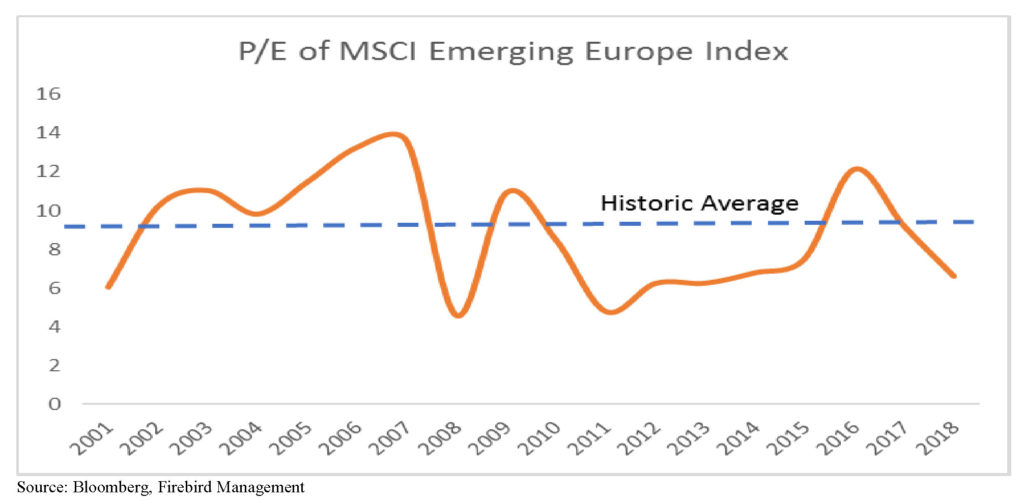

Even though multiples have not expanded, company earnings have. Companies making up the RTS Index grew sales and net income by 26% and 50% respectively since the beginning of 2016.

As a result of earnings growth, trading multiples contracted and are now close to historical lows.

Lack of Competition

A market in its most fundamental form is an equilibrium of supply and demand from buyers and sellers. Over the last few years, liquidity flooded the global markets and increased demand for investment options. This phenomenon resulted in record low yields spreads for bonds and high earnings multiples for many equity markets.

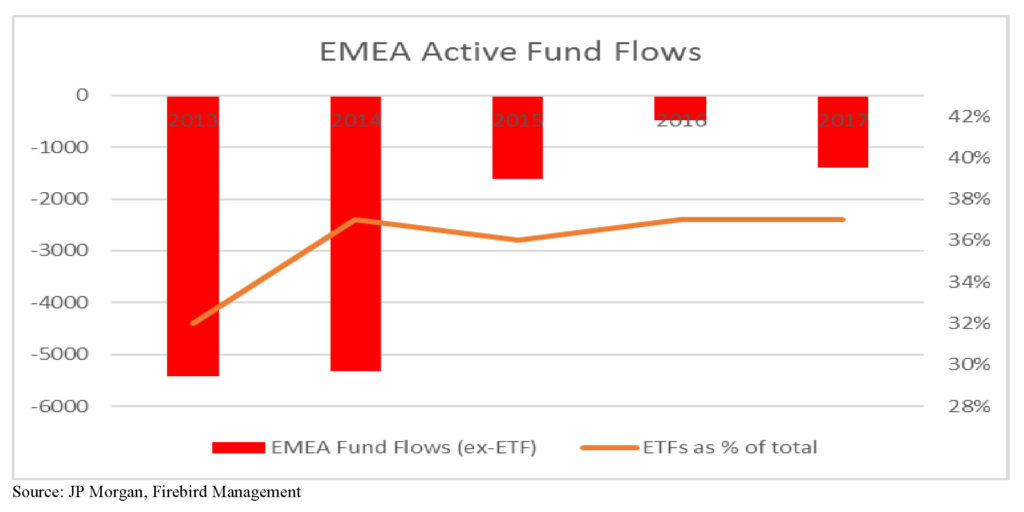

As the rest of the world enjoyed the fruits of central banks’ labor, foreign investors remained concerned about political headlines emanating from Eastern Europe. Regional conflicts and a perceived rise of authoritarianism combined to create an environment that was easier to overlook than to invest in. It also did not help that many of the smaller countries in the region are too small for large international investors. As an example, combined daily trading volume of the three exchanges in the Baltics is below $2 million. Lack of liquidity and negative headlines combined to create environment in which actively managed Eastern European equity funds have experienced net outflows for over five years.

Our markets, with few exceptions, are still lacking a natural domestic investor base that would come from retail and pension fund investors. Poland, with its well-developed pension funds required to invest in domestic equities, was an outlier with higher valuations and a mature equity market. Thanks to entrepreneurs viewing IPOs as a viable source of growth capital, Poland has over 800 listed companies.

In other countries, the domestic funding condition is bleaker. Pension funds as institutions have only started gathering scale in the last few years and for now are more comfortable investing in fixed income markets. Domestic equity allocation for the largest pension funds in the Baltic States is below 5% of total assets under management.

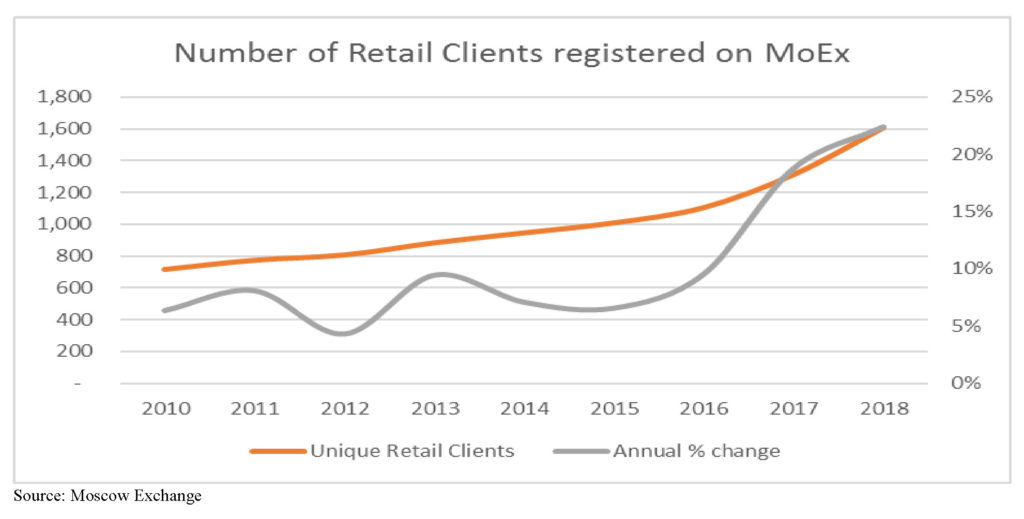

The good news about the lack of domestic sources of demand is that any change to the status quo would be positive. In Russia, where yields on bank deposits have fallen dramatically, we are seeing retail investors joining the market in record numbers.

In other countries, like Estonia, governments are working on various programs to encourage deepening capital markets.

Being a professional investor in this environment is challenging but potentially very rewarding. The reverse of low P/Es are high earnings yields. We are buying high-quality growing companies at valuations that can deliver IRRs of 15% or more without any multiple expansion. And if the valuation does improve, then the returns on investments in Eastern Europe could be much higher.

About The Author: MOI Global Editorial Team

The MOI Global Editorial Team, led by John Mihaljevic, CFA, includes community builders, event organizers, writers, editors, research associates, security analysts, and fanatical member support advocates. Our sole purpose is to serve the members of MOI Global as well as we possibly can in order to help them learn, invest intelligently, and build lifelong friendships with like-minded people.

Who is MOI Global? In recent years, The Manual of Ideas has expanded to become more than simply “the very best investing newsletter on the planet” (Mohnish Pabrai). We are now a thriving global community of intelligent investors, connected through great ideas, thought-provoking interviews, online conferences, live member events, and much more.

Members of MOI Global enjoy complimentary access to a growing array of resources and content related to the art of intelligent investing. Members also enjoy preferential access to selected offline events as well as exclusive access to other events hosted by MOI Global, including the Zurich Project Summit, the Latticework Conference, and Ideaweek.

More posts by MOI Global Editorial Team