Jiro Yasu and Patrick Rial of Varecs Partners presented their in-depth investment thesis on CRE Inc. (Tokyo: 3458) at Asian Investing Summit 2018.

Thesis summary:

CRE Inc. is a real estate company that develops and manages distribution warehouses. It is one of largest managers of such facilities in Japan. It develops a couple of warehouses per year and sells them off to its own REIT. It also gets the contract to manage them.

Revenues for the development business can be lumpy, depending on how many warehouses are developed and sold each year. On the other hand, the growing property management and REIT management businesses are recurring and quite stable.

Jiro and Patrick expect the market quotation to improve in the coming years as the weight of the recurring businesses grows. Japan needs more cutting-edge, large warehouses because many of the existing warehouses are aging and small. Many companies can cut logistics costs by moving to newer, larger warehouses. Also, the growth of e-commerce should provide stable demand growth for such warehouses.

At the recent share price, CRE’s market cap is 23 billion yen and enterprise value is 28 billion yen. A couple of warehouses are sitting on the balance sheet (will be sold this fiscal year). The sale proceeds and equity holdings explain most of the enterprise value, with little value assigned to the recurring revenue businesses.

Read an article by Jiro, entitled “A Snail’s View on Investing“.

The following transcript has been edited for space and clarity.

We have been honored to participate in these presentations since 2013, and we love to pitch ideas here. Some people have found our ideas interesting and contacted us, and we enjoy meeting those people globally. Let me start with some follow-ups on our past ideas before I move on to our new idea, which is a company called CRE.

Background

Our firm, VARECS Partners, is a Tokyo-based independent investment adviser. We started the business almost 12 years ago as a value investing firm. Value investing resembles a large tent – we have been trying out many different types, but we are narrowing down our focus these days.

Our strategy involves investing in undervalued Japanese equities. Typically, we focus on family-controlled businesses, and we prefer ones with high margin, modest growth, and a stable revenue stream. That’s where we are focused these days. We are long-term investors: our average holding is over five years. We have about 25 holdings in our portfolio at present, and maybe a quarter of them we have owned for over 10 years.

Our assets have grown a bit lately, and today we manage about $250 million. My family, which has a long history of running a brokerage business in Japan, exited a couple of years ago but invested about $20 million in that fund.

Our team is quite small – it’s Patrick Rial, Yosuke Yano, and myself.

Recap of Past Ideas

Since 2013, we have made four presentations. We first talked about two Japanese animation companies – Toei and Sotsu. We sold out of Toei in December 2015, but the share price has doubled since then, so it was too early to exit. We kept Sotsu, but this one has been struggling a bit. The share price has appreciated 80% since we made the presentation, and the company has animation rights, but it has had a tough time coming up with new hits. As a result, profit has grown only modestly in the last few years. The owner didn’t like the results and made a management change, so we are hoping for some progress at the company from now on. At present, 50% of Sotsu’s market cap is in cash, and it trades at only 5.4x EBIT.

In 2015, we presented a company called EM Systems. Its share price has performed well, more than tripling since the presentation. This is a software company providing software for dispensing pharmacies in Japan. It has the largest market share (30%) and has been enjoying margin improvement for the last two years, with operating margin doubling in three years.

EM Systems also has an immense property in Osaka. It still owns the building, which is fully occupied. We estimate the value of the building to be almost half of the current market cap.

Excluding the cash and property, the company is trading at around 6.5x EBIT, so this is still a cheap valuation for a highly profitable software company. Most of the revenues are of the recurring kind. Some similar companies overseas tend to trade at far higher multiples, so we are still keeping this as one of our largest holdings.

EM Systems is working on a major software upgrade and has partnered with some venture firms specializing in artificial intelligence. It has also started working with NEC, a huge Japanese software company.

In 2016, we made a presentation on an agrochemical company called Agro Kanesho. The share price has been performing well, appreciating 160% since then. Three years ago, the thesis was simple. The company has a lot of net cash on its balance sheet, so it is traded at almost no enterprise value. It has just started the development of three new products, and its R&D expenses have doubled, which has put some pressure on the operating margins. For this reason, the share price went down, and enterprise value became almost nothing.

We thought the high level of R&D would continue for some time, but if we were lucky, we’d have new products. Even if the company could not bring anything to market or failed in the development, it was okay because margins would come back as R&D cost went down.

Since 2016, the company has finished the development of one product. It gave up on another one and continues work on a third, so R&D costs have started declining this year, and we have noticed some margin improvement.

The company has bought land in Yamaguchi prefecture and is building a new factory, spending $40 million. The share price has appreciated a lot, but 50% of the market cap is still in cash, and it’s trading at 8.5x EBIT. This is still an attractive business to own for a long time, and we are keeping it as our core holding.

In 2017, we talked about a company called Amuse. This is a management company which has contracts with about 400 Japanese artists such as singers, rock bands, and actors. The share price did okay, appreciating by about 23%. Earlier in 2018, it traded as high as ¥4,000, but the share price has since corrected about 30%.

Amuse had quite a difficult year in 2017. One of its actors was involved in a scandal, and the company had to cover some costs for a movie. In addition, the vocalist of one of its major bands lost his voice, so they had to cancel some live events, and some new albums were delayed. As a result, the company missed its profit guidance, and the share price corrected from the high.

However, we still like the business and hope next year will be a good one for Amuse. The company will celebrate its 45th anniversary and is planning a lot of events for the occasion. Net cash makes up 40% of the market cap, and Amuse is trading at 7x LTM EBIT. We still have high hopes for the company and are keeping it.

Investment Thesis on CRE

CRE is listed on the Tokyo Stock Exchange under the code 3458. This is a real estate company focusing on logistic assets and is almost like a full-service company. Everything it does is related to logistics and warehouses: it develops warehouses, provides master-lease services for smaller warehouses owned by individuals, manages a public REIT, and offers other services related to warehouses.

The company is trading at ¥1,800 per share, and its market cap is a little over $200 million. It has used some debt, so its net debt is ¥5.7 billion, or about $54 million, which includes some debt for new developments. When it finishes development and sells the warehouse, it tends to pay down the debt right away.

CRE has two major investments: it owns a REIT and also has an investment in a service company specializing in the clean-up of contaminated land. The enterprise value is a ¥22.6 billion, traded at 4.2x EBIT and 6.3x price-to-earnings, both for the last 12 months.

This company has a good risk-reward profile. We always seek some downside protection. In the case of CRE, properties under development and investments sitting on its balance sheet represent almost 80% of the market cap plus net debt. We are paying ¥22 billion today, but almost $180 million or so is covered by assets. We see a 60% upside potential from here.

When speaking of growth prospects and valuation improvement potential, it should be noted we are a little behind in Japan in terms of the e-commerce penetration, lagging the United States and other countries. We believe this penetration will continue and will bring robust demand for warehouses in the future.

The company is also building a recurring revenue business, mostly the asset management business for their own REIT. The multiple will improve over the years as the recurring revenue stabilizes and profit grows.

Unlike most other Japanese companies, CRE is an excellent capital allocator. It has a great track record of acquisitions and a unique shareholder return program, which we like.

CRE was established in 2009, after the financial crisis. The owner set up a shell company and bought bankrupt warehouse operators.

The founding family still controls about 51%. Kenedix, another real estate company in Japan, has 14.7% and our fund owns about 9% of the company. Only 13% is owned by foreign investors. By the way, we are counted as a foreign investor because our funds are offshore. Excluding us, only 4% is owned by foreign investors at this point. The company went public about 2015, so it’s still new in the market.

If you look at the key members of the management team, you’ll see the chairman is 44 years old, while the president and the head of the REIT business are both 43. In other words, CRE is a company run by quite younger generation people who are also well-connected.

I’ve known the chairman, Mr Yamashita, since we were six years old; we grew up together. His family is famous in Japan – his grandfather was the first president of a Japanese quasi-government-owned oil exploration company. The family controls an extensive portfolio of real estate assets in Japan, so he’s well-connected to both real estate markets and financial institutions. This is a somewhat unique company because Japanese companies are mostly run by old people.

CRE went public on April 20, 2015. Before the IPO, I told my friend, chairman Yamashita, it was a stupid idea to go public because the share price moves every day and the CEOs of public companies sometimes get a call from angry shareholders. He would have to deal with many things he may not want to deal with. Still, he said he wanted to take the company public and ignored my advice. Right after IPO, the share price declined by almost 50%, and he called me up, saying maybe I was right. But it was too late, so he asked me to help realize some value.

We bought our shares in October 2015 almost at the lowest point, and we were able to buy some stock from the Yamashita family. The share price has been gradually recovering from the low and is now trading close to the IPO price.

The business model of CRE centers on providing a full range of services related to logistics real estate. These include development, leasing, master-leasing, property management, and REIT management. Every time CRE develops large warehouses, it sells them to its own J-REIT. As time goes by, it tends to develop about three to four new warehouses every year, so the AUM of J-REIT will grow over the years.

The company focuses on logistics and provides a full range of services. It prefers an asset-light business, so it doesn’t want to own the asset and sells them to the REIT. It is focusing on building recurring revenue.

In terms of development, the company is pretty much focused on its own projects, which comprise mid- to large-sized warehouses. In the past, it worked with some individuals, mostly farmers. In Japan, the farmers have been shrinking the farmland due to government guidance so they use the available land and ask CRE to build warehouses. Then CRE provides a master-lease service to such individuals or owners. These days, however, there aren’t many of them.

CRE also provides a property management service. Besides managing the warehouses owned by its REIT, it also buys warehouses owned by other REITs or real estate companies. By providing this service, it can learn which tenants are moving and what new warehouse a client wants. It gets a good deal flow and information by providing such services to many warehouses.

CRE Logistics REIT is a public REIT run by CRE REIT Advisors, which is a wholly owned subsidiary. Kenedix, which owns 15% of CRE, bought the stake in 2017 because it wanted to help the company smooth the IPO of the REIT. The REIT went public in February 2018.

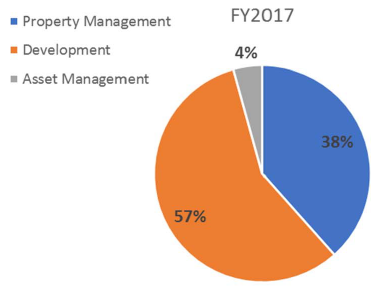

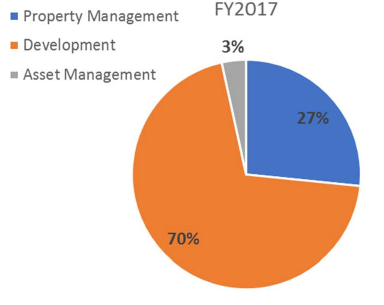

In terms of revenue, property management was about 40% of the total in fiscal 2017 and accounted for 27% of the operating profit.

CRE Inc. — Revenue Mix

CRE Inc. — Breakdown of Operating Profit

Source: Jiro Yasu and Patrick Rial at Asian Investing Summit 2018.

Development revenue has been growing: it was only ¥7.8 billion in 2015 but almost tripled to ¥23 billion in 2017. The segment reported operating profit of ¥4.2 billion, and development contributed 70% of total operating profit in 2017.

CRE has the capacity to develop maybe three to four warehouses every year, but revenue could be quite lumpy because it depends on the size and location of a warehouse. The 2018 guidance has only ¥13 billion of revenue and operating profit of ¥800 million from development. That’s why the company is trying to build more recurring revenue, which will come from property and asset management.

We expect development revenue and property to be lumpy in the coming years, but the property management and asset management businesses will become a larger part of the company.

Regarding the balance sheet, CRE was quite levered a few years ago. But as earnings grew, the equity ratio improved a lot, and the company now has a significantly better balance sheet.

Speaking of property management, it provides property management services to the assets owned by its REIT and other entities. This part of the business has been growing, and another thing is the more steady revenue, but this is a master-lease service for individual owners.

In terms of area, property management is larger, but the profit from master-lease is way bigger. This business can pay all the fixed costs of the company. It has been keeping a high utilization rate of the master-lease assets.

CRE has been highly disciplined. It tends to focus on lower-risk projects, avoiding large warehouses as it associates them with higher risk. Also, it knows who could be the tenants for some of its new developments and tries to get pre-commitments.

Over the last few years, floorspace has been growing, but 2018 could be a slower year for the company. Still, it does have a good pipeline. It has also announced another land acquisition, which is quite large-scale and could increase the total floorspace of the pipeline by maybe 30%.

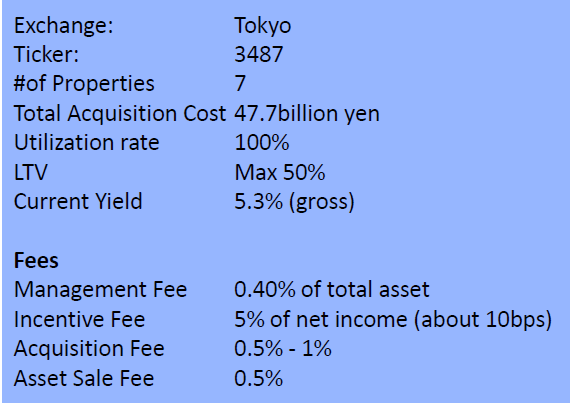

CRE Inc. — Overview of CRE Logistics REIT

Source: Jiro Yasu and Patrick Rial at Asian Investing Summit 2018.

Regarding the asset management business, CRE Logistics REIT currently has AUM of ¥96.6 billion. This number includes non-REIT assets. Long term, the company aims to grow AUM to ¥500 billion, which is almost $5 billion. It sounds as if it has a pipeline to build it to a billion dollars in a couple of years. Through our funds, we also own about 2% of CRE REIT because we believe the quality of the assets is quite high and the yield is attractive.

CRE Logistics REIT charges a management fee of 40 basis points (bps). There is an incentive fee of 5% of net income, which is about 10 bps. Also, when it buys and sells assets, it gets the acquisition and sale fees. When it buys assets from CRE, the acquisition fee is only 50 bps but 1% if it buys assets from other companies.

Assuming maybe 20% turnover, it can make another 10 bps from those fees, so the company will probably make about 60 bps from those assets. If it gets to a billion dollar AUM, it can make $6 million or so from this business.

There’s a virtuous cycle here. The company develops the warehouses that will drive AUM growth, and as the assets grow, it can easily issue shares for REITs, so that will give it money to buy more. By having a public REIT, the company’s capacity to do larger developments has improved.

When you compare it to other public REITs in Japan, you see CRE has maintained a highly disciplined approach to developments. It has mostly focused on the Tokyo area so far and has avoided super large-sized deals, perceiving higher risk in them. It has also been using leverage prudently.

The market cap is just ¥26 billion because the company went public only recently and is still the smallest of its peers. Currently, the REIT has seven properties, 94% of which are located in the Tokyo area, which is the highest proportion among peers. Some competitors have significant exposure to super large warehouses (over 100,000 square meters), but CRE has none of those. All seven properties are quite new, and the tenants have longer-term contracts, which makes us believe these are high-quality assets.

The yield is 5.3%, which is high and has to do with the fact the company is still new and small. Considering the quality of the assets, 5.3% is a highly attractive yield in Japan.

Let’s consider the growth opportunities in Japan. E-commerce penetration in the country is only 5.4% at this point, or about 2.7% behind the level in the United States. We expect e-commerce in Japan to grow: it’s ¥15 trillion now, and some research companies expect ¥20 trillion by 2020. As e-commerce grows, more warehouses will be needed, which will create robust demand for new facilities.

In terms of capital allocation, we consider CRE one of the few companies thinking about capital allocation logically. Yamashita set up his company in 2009 to acquire bankrupt businesses. In 2010, he only paid a ¥500 million to buy the master-lease and property management business of Commercial RE. This business now makes about ¥1.5 billion in operating profit.

In 2011, the company acquired another master-lease business, Tenko-Souken, which operates mainly in Kanagawa prefecture (next to Tokyo). Three years later, CRE acquired an investment advisory business called Strategic Partners KK. Today, that’s CRE REIT Advisors, which is the advisory manager of CRE’s own public REIT.

In 2015, the company bought a 20% stake in Enbio Holdings, which specializes in utilizing contaminated land. It paid about ¥800 per share, and Enbio is now trading at around ¥2,000, so it has more than doubled since the acquisition.

When my friend asked for help right after the IPO and the 50% drop in the share price, one area we focused on was the shareholder return program. The company has a stable business and a lumpy business, so we told the management simply paying a 30% dividend was not such a great idea. That’s because one year it has a solid profit and the next year a small one, so it would have to cut the dividend, which is not that good.

We want the company to grow its dividend every year. We also know its stable business will grow over the years, so the dividend policy is paying 50% of profits from recurring businesses (master-lease and asset management).

Also, I thought the company could do buybacks. There’s an opportunity for CRE to do this wisely because many people in Japan focus on short-term earnings. With this company, a large part of its profit currently comes from development. One year may be great, but the next could be a slow year, and it can see negative growth in operating profit and the share price may go down. The company can take advantage of this profit lumpiness and do the buyback when earnings and the share price are low.

It did some buybacks, using cash from development business to buy its own shares when the price was low. Since 2018 is quite a slow year, the company announced a ¥1 billion buyback program alongside its guidance – ¥1 billion is about 4.7% of the shares outstanding.

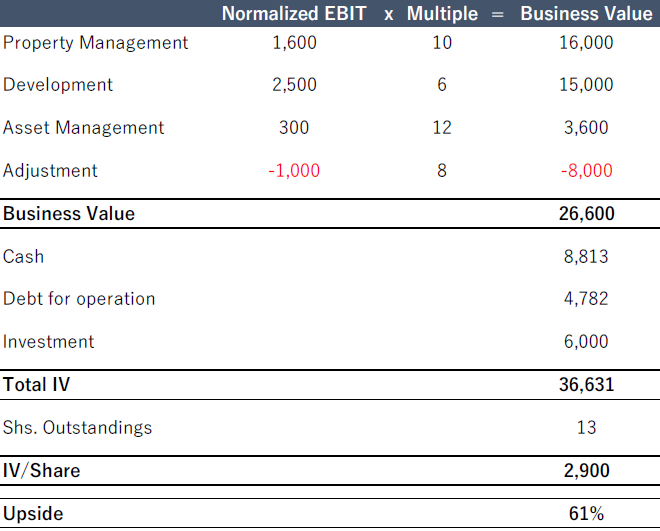

CRE Inc. — Intrinsic Value (yen in millions, except per share data)

Source: Jiro Yasu and Patrick Rial at Asian Investing Summit 2018.

With regard to intrinsic value calculation, we usually look at the deals in a similar industry. GLP was bought out in 2017, and there was previously a larger merger between AMB Property and ProLogis. These are quite high multiples because these companies not only develop warehouses but also own them and are structured as a REIT. An EBITDA multiple of 33 means 3% yield or something like that, so we can’t use this multiple to value CRE.

Asset management firms are a little easier to understand. There are some deals of independent asset managers bought out by larger groups. We see people paying over 10x EBITDA for some asset management businesses. This is the multiple we used to value CRE’s asset management business.

We applied 10x EBIT for property management, 6x EBIT for development (because of the lumpiness), and 12x EBIT for asset management. We also excluded the debt, which is only associated with the warehouse development and not used for business operation. We used normalized EBIT. CRE expects the development business to make only ¥ 100 million in 2018, but the company made over ¥4 billion in operating profit in 2017, so we cut in the middle and then used ¥2.5 billion as normalized EBIT for the business.

We came up with the business value of ¥26.6 billion. The company has cash and debt in investments and divided by shares outstanding, we see ¥2,900 as the intrinsic value and calculate a 61% upside.

Value per share will grow over the years as the AUM of J-REIT grow.

We have owned shares in the company since 2015, and it has good growth prospects. We hope the quality of earnings and the multiple will improve over the years.

The following are excerpts of the Q&A session with Jiro Yasu and Patrick Rial:

Q: Could you perhaps provide a longer-term perspective on this business in terms of how you see it evolving over a decade or two? How big can it potentially become due to the virtuous cycle existing between CRE and the REIT business?

A: The company has a good pipeline to grow AUM to a billion dollars. Its actual goal is $5 billion. Then the company can make about 60 bps. This amount, $5 billion, is the size of competitors like GLP and LaSalle.

We are conservative thinkers but consider $1 billion almost sure and don’t see $5 billion as impossible. I don’t know how quick it can achieve that level, but we hope it can happen in 10 years or so. The company will continue to develop about three to four warehouses every year, so maybe those revenues could be anywhere from $150 million to $300 million. It also recently acquired two plots of land, and one of them could become a $200 million-plus warehouse.

Since it has a large public REIT, the company should have more capacity to do more developments, so the virtuous cycle could accelerate over the years.

Q: Could you elaborate a bit more on the nature of the customer contracts they have? Are the warehouses highly customized for those customers, and for how many years are those warehouses typically contracted to the same customers?

A: Contracts can be 5 to 10 years, so quite long. In terms of customization, it all depends on the tenants, but CRE tries to build warehouse anybody can use. It tries to minimize customization, but the client sometimes wants better customization. That’s the negotiation it has to do. With pre-commitment deals, it usually does deeper customization and seeks longer contracts. This is a trade-off of sorts. If it customizes more, it will seek longer contracts. If there isn’t much customization needed, it will be happy with shorter contracts, so it’s a flexible negotiation.

Q: On the REIT itself, what is CRE’s ownership there?

A: CRE currently owns about 15% of J-REIT, which is a little over $30 million.

Q: What risk is top of mind for you regarding your long-term thesis here?

A: Warehouses have been great assets for many people. When they find a good location, the competition can become quite stiff, and CRE may have to pay a higher price to acquire the land. If it becomes too aggressive, it could lose money on new developments – it happened with some other firms. We like CRE because it is highly disciplined. It doesn’t mind saying no if it doesn’t see at least 15% gross margin based on a conservative estimate of rents.

However, its competitors could get quite aggressive, and because CRE is a disciplined investor, it might have a tough time finding new land. If it cannot buy new land, it cannot do a development and revenues can go down.

Still, we don’t want it to become too aggressive. That’s why its relationship with Enbio Holdings is important – Enbio has good technology to clean up dirty, contaminated land cheaper, and this will give CRE some advantage when bidding for new land. Also, CRE has strong relationships with many clients and tends to get pre-commitment from tenants. With pre-commitments in place, it can be aggressive on price and more likely to win the land. But there’s clearly the risk of stiff competition among warehouse developers because they have to compete with far bigger firms like GLP or LaSalle.

About the instructors:

Jiro Yasu has more than 15 years of investment experience in the Japanese equity markets including at Varecs Partners, First Eagle Investment Management and Daiwa Securities America. As the Representative Director of Varecs Partners, Jiro spearheads the investment firm’s efforts to identify mid-sized listed Japanese companies where corporate value can be realized for all stakeholders by working together with management. Jiro holds a BA in economics with a specialty in econometrics from Keio University.

Patrick Rial joined VARECS Partners in 2015 as Senior Analyst. He joined from J.P. Morgan Securities Japan where he worked in equity strategy and small cap research. Prior to J.P. Morgan, he was a product manager at Morgan Stanley MUFG Securities. Mr. Rial began his career as a financial journalist covering Japanese equity markets. He has been a CFA charterholder since 2011. He holds a BA in economics and history from Georgetown University.

About The Author: MOI Global Editorial Team

The MOI Global Editorial Team, led by John Mihaljevic, CFA, includes community builders, event organizers, writers, editors, research associates, security analysts, and fanatical member support advocates. Our sole purpose is to serve the members of MOI Global as well as we possibly can in order to help them learn, invest intelligently, and build lifelong friendships with like-minded people.

Who is MOI Global? In recent years, The Manual of Ideas has expanded to become more than simply “the very best investing newsletter on the planet” (Mohnish Pabrai). We are now a thriving global community of intelligent investors, connected through great ideas, thought-provoking interviews, online conferences, live member events, and much more.

Members of MOI Global enjoy complimentary access to a growing array of resources and content related to the art of intelligent investing. Members also enjoy preferential access to selected offline events as well as exclusive access to other events hosted by MOI Global, including the Zurich Project Summit, the Latticework Conference, and Ideaweek.

More posts by MOI Global Editorial Team