This article is authored by MOI Global instructor Soumil Zaveri, a managing partner of DMZ Partners. Soumil is an instructor at Asian Investing Summit 2018, the fully online conference featuring more than thirty expert instructors from the MOI Global membership community.

I had a fantastic week in St. Moritz at Ideaweek during the insightful sessions John Mihaljevic and Shai Dardashti put together for a group of like-minded investors from around the world. It was an opportunity to share a few thoughts on the nuances of investing in listed Indian equities and to learn from far more experienced investors.

I was on the receiving end of thought provoking questions which helped me isolate the “source-code” of some of my opinions. One such question was, “Isn’t your investment thesis very strongly tethered to India’s macroeconomic progress?” i.e. Isn’t your investment approach basically a big macro call on India? In anticipation of my participation at the Asian Investing Summit in April I’ve elaborated a few of my reflections on this point below.

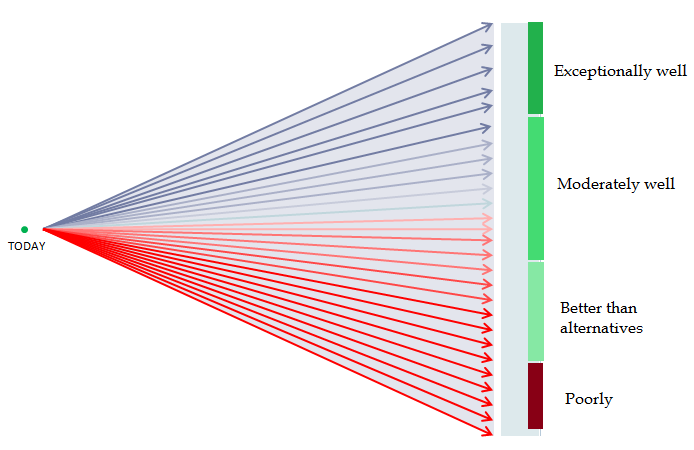

There may be reasons to agree with this viewpoint given that the 8 – 12 companies we tend to consider appealing at any point in time are certainly not immune from economic or social catastrophe. In a small adverse range of potential outcomes our companies are undoubtedly unlikely to do well (see image 1). That said, an important characteristic we seek in investment-worthy candidates is resilience. Given that we would like to own a few high quality businesses for long periods of time, we find it important to understand whether they are likely to do reasonably well in a relatively wide range of future outcomes.

So in essence, while our investment thesis is tethered to the general socio-economic & political stability of the country it is not overly-reliant on whether the GDP growth rate from 2018-2020 will be 7% or 5%. While our view on our companies’ long-run prospects is bolstered by the idea that a several hundred million strong middle class will generally produce and consume more over a decade, it is not subject to whether the total market size for a consumer product over that time frame is likely to be 200 million units or 150 million units.

While we are certainly not macro experts, I derive comfort from the idea that we are starting off a very low and narrow consumption base and that small marginal changes in consumer behaviour and consumption patterns are still very potent in terms of the business niches/ sectors they engender. Our view is that this is a relatively likely outcome irrespective of political dynamics, progressive/ regressive regulatory changes, GDP growth, commodity prices etc. – the last 20 years have also been a testament to this idea.

A range of future alternative outcomes for our portfolio companies

As a side-note, we don’t intend to trivialize such factors as they certainly play an important role in accelerating/ delaying the entry of several million people into better socio-economic conditions – a cause we care deeply about. Also, better macro-conditions, needless to say, provide the most conducive environments for our portfolio companies to flourish. That said, from an investing perspective, we believe that the majority of companies we own are likely to continue to do reasonably well even in relatively lackadaisical/ sluggish and perhaps even mildly regressive environments – an opinion buttressed by two key factors. One, our portfolio companies typically have very low market shares relative to the currently addressable universe. Two, in our view, our companies offer customers very compelling alternatives to products/ services provided by industry incumbents.

This gives us conviction that our companies are likely to take meaningful chunks of market share even if and when their sectors slow down. Our businesses tend to have low single-digit market shares or adoption rates relative to their potential. Sometimes they operate in very fragmented or unorganized markets which are slowly consolidating and formalizing. At other times, they are in sectors with very large incumbents which are poorly calibrated to compete due to legacy issues that foster deep-rooted inefficiencies. At times, our companies operate in specialized niches that are unappealing for industry “Goliaths” to encroach upon.

Finally, a few of our companies offer novel, only recently viable solutions that provide compelling alternatives to the conventional methods of transacting/ doing business in a particular industry – here adoption may be still very low but growing – our companies’ prospects in such cases are seldom linked to industry level growth. These factors fuel our conviction that our portfolio companies can do relatively well even in quite suboptimal macro environments.

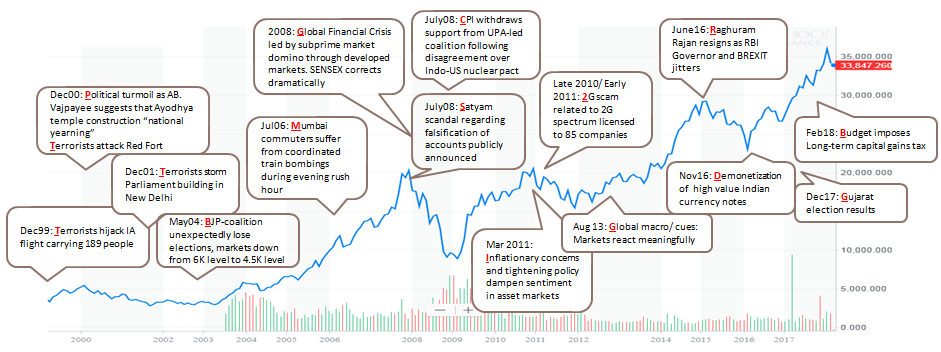

Macro-noise from 1999 – 2018 superimposed on India’s Sensex Index graph

As anecdotal evidence, image 2 provides a small cross-section of the frenzy of “macro-noise” that has dominated Indian markets over 20 years. Examples of what commentators have viewed as gloomy macro events include demonetization in 2016 or fraud accusations related to public sector banks more recently. In our experience, irrespective of this macro-noise, companies we have admired over the past decade or two have largely been insulated through these phases. This insulation in our view, is as much a function of how they do things differently, as it is a function of their size relative to the size of markets they address or seek to address.

This makes us confident that although our simplified expectations of India’s progress over the next 20 years may be more upbeat than its last 20 years – our investment approach is somewhat agnostic to such outcomes. This leads me to conclude that by virtue of our portfolio constituents, we are not really taking a “big macro-call on India”.

Disclosures: DMZ Partners Investment Management LLP is a SEBI registered Portfolio Manager (SEBI Registration No.: INP000005944). Positions held by DMZ Partners Investment Management LLP (DMZ Partners) and its partners, employees, clients and associates may be inconsistent with views mentioned herein. DMZ Partners or its associates accept no liability for any errors or omissions in the given content. The material presented herein does not constitute a recommendation or offer for the purchase or sale of any securities and is provided solely for informational purposes. Unauthorized usage, alteration or distribution of this information is prohibited.

About The Author: Soumil Zaveri

Soumil Zaveri moved to the US in 2005 to study Economics and Biology at Duke University, in North Carolina. He had the good fortune of being taught by phenomenal professors including Dr. Emma Rasiel. At Duke he presided over the Investment Club with, now good friend, James Schulhof. In the summer of junior year, He interned with Goldman, Sachs & Co. in New York on the healthcare team with in the Research division. He was extended a full time offer and joined the banking team there after graduation. He witnessed an exponential learning curve while working with Richard Ramsden, Brian Foran, Quan Mai & Ryan Fulmer through the financial crisis. Given the magnitude of changes affecting the western economies, the resilience of Asian ones and his desire to be back home, after a few years in New York, he moved back to Mumbai to start his own investment firm, and to work directly on allocating personal and family capital.

DMZ Partners was founded on 1st April 2011 as a partnership firm. His grandfather, who was very fond of him, was Dinesh Mahsukhlal Zaveri (initials DMZ), and co-incidentally his father’s great grandfather who was a successful businessman of his time, Dahyalal Makanjee Zaveri also carried the same initials.

More posts by Soumil Zaveri