The more money you make from tech, the more you shield your family from its effects pic.twitter.com/ZG2K5MUrCv

— Rami (@rbaassiri) August 28, 2018

Paratek Pharmaceuticals: Deep Sell-off Renders Shares Cheap

August 25, 2018 in Equities, Ideas, LettersThis article is excerpted from a letter by MOI Global instructor Jim Roumell, partner and portfolio manager of Roumell Asset Management (RAM), based in Chevy Chase, Maryland. Jim is a valued participant in The Zurich Project.

PRTK is a biotech company focused on developing new novel antibiotics, principally Omadacycline (OMC). I met with Evan Loh, President, COO and CMO, Adam Woodrow, COO and Ben Strain, Investor Relations at their office in King of Prussia, PA. Ben recently left a very good job at Biogen, where he worked for the past eight years, to join PRTK.

The PRTK team remains convinced that the market needs a broad-spectrum antibiotic, particularly with an IV to oral capability for community acquired bacterial pneumonia (CABP). This, of course, has been their claim since the beginning. The August 8th FDA Advisory Committee meeting is expected to produce a favorable vote for three indications. There will be 14 to 15 people on the committee.

The FDA significantly weighs the Committee’s recommendation, but it is not bound by the committee’s vote. The three indications are: IV to oral skin; oral-only skin; and IV to oral CABP. I will be attending the FDA Advisory Committee meeting on August 8th in Washington, DC.

PRTK’s next challenge will be winning the commercialization battle. PRTK has always articulated a clear, thoughtful approach to gain market acceptance.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Disclosure: The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. The top three securities purchased in the quarter are based on the largest absolute dollar purchases made in the quarter. Roumell Asset Management, LLC claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Roumell Asset Management, LLC has been independently verified for the periods January 1, 1999 through December 31, 2017. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm’s policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation. The Balanced Composite has been examined for the periods January 1, 1999 through December 31, 2017. The verification and performance examination reports are available upon request. Roumell Asset Management, LLC is an independent registered investment adviser. The firm maintains a complete list and description of composites, which is available upon request. Results are based on fully discretionary accounts under management, including those accounts no longer with the firm. Past performance is not indicative of future results. The U.S. dollar is the currency used to express performance. Returns are presented net of management fees and include the reinvestment of all income. Net of fee performance was calculated using actual management fees. From 2010 to 2013, for certain of these accounts, net returns have been reduced by a performance-based fee of 20% of profits, paid annually in the first quarter. Net returns are reduced by all fees and transaction costs incurred. Wrap fee accounts pay a fee based on a percentage of assets under management. Other than brokerage commissions, this fee includes investment management, portfolio monitoring, consulting services, and in some cases, custodial services. Prior to and post 2006, there were no wrap fee accounts in the composite. For the year ended December 31, 2006, wrap fee accounts made up less than 1% of the composite. Wrap fee schedules are provided by independent wrap sponsors and are available upon request from the respective wrap sponsor. Returns include the effect of foreign currency exchange rates. Exchange rate source utilized by the portfolios within the composite may vary. Composite performance is presented net of foreign withholding taxes. Withholding taxes may vary according to the investor’s domicile. The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite for the entire year. Dispersion calculations are greater as a result of managing accounts on a client relationship basis. Securities are bought based on the combined value of all portfolios of a client relationship and then allocated to one account within a client relationship. Therefore, accounts within a client relationship will hold different securities. The result is greater dispersion amongst accounts. The 3-year annualized ex-post standard deviation of the composite and/or benchmark is not presented for the period prior to December 31, 2012, because 36 monthly returns are not available. Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. The investment management fee schedule for the composite is as follows: for Direct Portfolio Management Services: 1.30% on the first $1,000,000, and 1.00% on assets over $1,000,000; for Sub-Adviser Services: determined by adviser; for Wrap Fee Services: determined by sponsor. Actual investment advisory fees incurred by clients may vary.

This article is excerpted from a letter by Luis Sanchez and John Pelly, co-founders and managing partners of Overlook Rock Asset Management, based in New York.

“At some price, every company is a buy; at some price, every company is a hold; and at a still higher price, every company is a sell.” –Seth Klarman

We agree with fellow value investor Seth Klarman, price discipline is extremely important, if not the most important factor for good investment results. Experienced stock market investors recognize that the market is fickle. Stocks that are dear in the first quarter can quickly become despised by the third quarter and prices can swing on the turn of a dime. This is true for large blue chip stocks that frequently make headlines. This is especially true for lesser-known small capitalization stocks that can trade wildly on sentiment or rumors.

Let’s use the last four years of Walmart’s stock price as an example. If four different investors bought Walmart at four different points in 2015 and sold the stock at the end of the last quarter, they could have had widely different investment returns. The table below shows the average dividend adjusted stock price Walmart traded at during each quarter in 2015. The range of possible returns is over 40%! Keep in mind that Walmart is one of the largest and most-followed stocks in the entire world.

As active managers, we take advantage of the volatility in the stock market to buy and sell at opportunistic prices. However, we are presented with a problem when new clients become partners at Overlook Rock and when existing clients provide us with more capital to invest. The problem is that over the course of time the opportunity set of what is trading for an attractive price changes. In other words the stocks we bought for clients in the first quarter may no longer be the best stocks for new money in the second or third quarter.

We have decided the best way to maximize investment returns for all clients is to invest fresh capital in the best opportunities at the time capital is deployed. For most active managers, this approach is out of the question because it would be impractical to conduct research on a new set of companies while maintaining research coverage on existing investments. However, we have leveraged our combined technical and analytical proficiencies (something we believe is quite unique in the investment industry) in a way that allows us to effectively maintain multiple portfolios which represent the best opportunities according to our process at the time of formation.

Our software and human analysts evaluate the top investment ideas on a daily basis. Because we are always on top of the best investment ideas at any given time, we have the ability to fully invest a new portfolio with little notice. In addition, our software monitors each investment idea and provides the human analysts with the determination on when to sell. As a result, our software plus human oversight investment process is highly scalable. Not only does our technology enable us to better pick stocks but it enables us to better manage money.

While there may be a day in the not so distant future when we allow clients to send us money to be invested with little to no advanced warning, for now we have decided to gate inflows to just once or twice a year in “vintages”. Each vintage will be invested in the top ideas at the time capital is deployed. Our first vintage was deployed in January 2018 and we are currently collecting investor interest for our second vintage which will be established in the second half of 2018.

Disclaimer: Overlook Rock Asset Management is a registered investment adviser. Information presented is for discussion and educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. The information and statistical data contained herein have been obtained from sources, which we believe to be reliable, but in no way are warranted by us to accuracy or completeness. We do not undertake to advise you as to any change in figures or our views. This is not a solicitation of any order to buy or sell. We, any officer, or any member of their families, may have a position in and may from time to time purchase or sell any of the above mentioned or related securities. Past results are no guarantee of future Results. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. These comments may also include the expression of opinions that are speculative in nature and should not be relied on as statements of fact. Overlook Rock Asset Management is committed to communicating with our investment partners as candidly as possible because we believe our investors benefit from understanding our investment philosophy, investment process, stock selection methodology and investor temperament. Our views and opinions include “forward-looking statements” which may or may not be accurate over the long term. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise. While we believe we have a reasonable basis for our appraisals and we have confidence in our opinions, actual results may differ materially from those we anticipate. The information provided in this material should not be considered a recommendation to buy, sell or hold any particular security.

Facebook and the Challenges of Investing in an Expensive Market

August 22, 2018 in Equities, Ideas, LettersThis article is excerpted from a letter by Zeke Ashton, managing partner of Centaur Capital Partners, based in Southlake, Texas.

We view Facebook’s ~20% stock price decline in late July as sort of a “sequel” to its initial decline earlier this year when the stock suffered a similar fall. We had taken the Fund’s position in Facebook to as high as 20,000 shares back in March as the data usage controversy reached its most intense level. As the stock rallied into the summer and the world’s attention moved to other subjects, we trimmed the position at incrementally higher prices such that we had reduced the Fund’s position to 13,000 shares going into the late July Q2 earnings report.

We believe that Facebook’s management has elected the path of absorbing some short term pain in order to protect the longer term value of the business. Facebook’s biggest risk factors appear to be reputational and regulatory in nature, and the company needs to show that it takes responsibility for the potential negative societal impacts introduced by its products in order to mitigate these risks.

If Facebook is successful in its efforts to the extent that both users and advertisers perceive that its services are less prone to societal harm, then the business will likely be far healthier and better insulated from these hard-to- quantify risk factors in the future.

However, it is also apparent that Facebook will be investing heavily to better monitor the 2.5 billion users and many millions of advertisers across its platform. As a result, the company’s near term financial outlook seems somewhat less attractive than it did prior to the recent controversies, and our estimated value range for the stock is also somewhat lower today than it was six months ago.

Importantly, in our view Facebook’s business remains immensely strong and user behavior has largely been unchanged by the recent negative events and corresponding media coverage. Now that expectations for the business have been re-set, we hope that the company can move forward with less drama and the stock price will move higher as the market regains comfort with the company’s strategic direction. As of this writing the Fund’s position of 15,000 shares is roughly a 4% portfolio weighting with the stock trading at around $175 per share.

Challenges of Investing in an Expensive Market

While the Fund has made money on its Facebook investment so far in 2018, we feel somewhat fortunate to have done so because the stock itself has not produced a gain. Our experience has been somewhat better only because we bought shares on weakness and sold shares on strength.

However, I think Facebook is a good case study in the difficulties of investing in a market in which nearly all high quality businesses trade at extremely full valuations, and in most cases one can really only hope to find relative (not absolute) value. The problem is that when prices are full, stocks are vulnerable to sudden changes in future expectations.

In the case of Facebook, we can make a strong argument for relative value at prices we paid, but we know that the margin of safety in the event we are too optimistic in our estimates is much lower than we’d like.

While most of the Fund’s investments aren’t in high growth companies like Facebook and therefore aren’t quite as sensitive to changes in expected future growth rates and profit margins, we still have less room for error than we’d like on the valuation side across the portfolio.

This means we have to be very diligent with respect to watching for emerging risk factors that could affect our portfolio companies. It also means we need to be aware of how the potential risk/reward pay-offs for our securities change as prices move around, and take reasonable action to increase or decrease exposure when opportunities present themselves.

Disclaimer: This report is being furnished by Centaur Capital Partners (“Centaur”) on a confidential basis and does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services. This report is being provided to existing limited partners for informational purposes only, and may not be disseminated, communicated or otherwise disclosed by the recipient to any third party without the prior written consent of Centaur. An investment in the Fund (“CVF”) involves a significant degree of risk, and there can be no assurance that its investment objectives will be achieved or that its investments will be profitable. Certain of the performance information presented in this report are unaudited estimates based upon the information available to Centaur as of the date hereof, and are subject to subsequent revision as a result of the CVF’s audit. The performance results of CVF include the reinvestment of dividends and other earnings. Past performance is not necessarily a reliable indicator of future performance of CVF. An investment in CVF is subject to a wide variety of risks and considerations as detailed in the confidential memorandum of CVF. References to the S&P 500, NASDAQ Composite and other indices herein are for informational and general comparative purposes only. There are significant differences between such indices and the investment program of CVF. CVF does not invest in all or necessarily any significant portion of the securities, industries or strategies represented by such indices. References to indices do not suggest that CVF will or is likely to achieve returns, volatility or other results similar to such indices. This presentation and the accompanying discussion include forward-looking statements. All statements that are not historical facts are forward-looking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events. The information in this presentation is not intended to provide, and should not be relied upon for, accounting, legal, or tax advice or investment recommendations. Each recipient should consult its own tax, legal, accounting, financial, or other advisors about the issues discussed herein.

.@WarrenBuffett once said, “What the wise man does in the beginning, the fool does in the end.” This tells you 80% of what you have to know about #MarketCycles and their impact. I consider this the number-one piece of #investment wisdom. –HM

— Howard Marks (@HowardMarksBook) August 21, 2018

This article is authored by MOI Global instructor Steven Kiel, chief investment officer of Arquitos Capital Management.

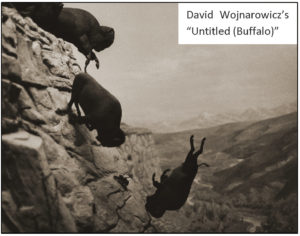

Thousands of years ago, before the use of horses, Native Americans utilized a hunting technique that preyed on animalistic instincts. This technique was called the buffalo jump. Hundreds of buffalo could be killed at a time without the use of weapons.

Thousands of years ago, before the use of horses, Native Americans utilized a hunting technique that preyed on animalistic instincts. This technique was called the buffalo jump. Hundreds of buffalo could be killed at a time without the use of weapons.

Tribesmen would set up a path lined with piles of rocks and tree stumps, creating a “road” towards the cliff. Hunters would then frighten a lead buffalo in a herd onto the path and cause a stampede.

Stampedes are not unique to buffalo and happen with humans as well, even today.

Psychological stampedes are more widespread than physical stampedes, though. The dot com bubble was a psychological stampede. The run-up in housing prices prior to 2008 was a psychological stampede. So were Beanie Babies, the Salem witch trials, tulips, the nifty-fifty, and too many more examples to list.

Stampedes (or bubbles or manias) are a staple of human nature. We have a fear of missing out. We are greedy and fearful. Like the buffalo, we feel safer in the crowd. As Keynes has said, “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.”

Sometimes it takes courage simply to be a bystander. We don’t have to be Michael Burry betting against sub-prime mortgages. During the housing bubble, we could have succeeded by simply sitting it out, not investing in lenders, homebuilders, and other ancillary businesses, staying away from AIG, Lehman Brothers, Bear Stearns. If we can be the hunter, then great, but we can also win by not being the prey.

How does that apply to our portfolio? I avoid companies in industries that attract risk-takers. It is very difficult for a company to go bankrupt if they don’t have debt, so I avoid margin leverage in the portfolio, and I avoid companies that rely on debt.

As a passive owner in a business, we want the decision-maker at the company to like vanilla ice cream and The Andy Griffith Show, and we want him or her to drive a Toyota Corolla. The more boring the better. Sure, we can get rich riding along with a daredevil, but how would we know when to get off the ride? We know compounding works in our favor, so why take the risk?

Ideal CEOs for us are people like Brian Moynihan at Bank of America and Mike Falcone at MMA Capital. Both are focused on creating long-term value for their shareholders and not taking unnecessary risks. Ironically, it can be unconventional to be a boring CEO!

There is both wisdom and madness in crowds. The point is to be thoughtful about who we follow, what companies we own, and how we go about making decisions. Without that thoughtfulness, we would have no chance of beating the markets.

Disclaimer: This letter is for informational purposes only and does not reflect all of the positions bought, sold, or held by Arquitos Capital Offshore Master, Ltd. or its feeder funds, Arquitos Capital Partners, LP and Arquitos Capital Offshore, Ltd. Any performance data is historical in nature and is not an indication of future results. All investments involve risk, including the loss of principal. We disclaim any duty to provide updates or changes to the information contained in this letter. Performance returns presented above are for Arquitos Capital Partners, LP and reflect the fund’s total return, net of fees and expenses since its April 10, 2012 inception. They are net of the high water mark and the 20% performance fee, applied after a 4% hurdle, as detailed in the confidential private offering memorandum. Arquitos Capital Offshore, Ltd. was launched on March 1, 2018. Returns from Arquitos Capital Offshore, Ltd. may differ slightly and are not presented here. Performance returns for 2018 are estimated by our third-party administrator, pending the year-end audit. Actual returns may differ from the returns presented. Positions reflected in this letter do not represent all the positions held, purchased, or sold. This letter in no way constitutes an offer or solicitation to buy an interest in Arquitos Capital Partners, LP, Arquitos Capital Offshore, Ltd. or any of Arquitos Capital Management’s other funds or affiliates. Such an offer may only be made pursuant to the delivery of an approved confidential private offering memorandum to an investor.

This article by MOI Global instructor Robert Leitz has been excerpted from a letter of iolite Partners, a value-oriented investment firm based near Zurich, Switzerland.

In 2007, a man started to play the violin at a metro station in Washington DC on a cold January morning. He played six Bach pieces for about 45 minutes. During that time, since it was rush hour, thousands of people went through the station.

Three minutes went by until somebody noticed there was a musician playing. A middle-aged man slowed his pace and stopped for a few seconds — and then hurried up to meet his schedule. A minute later, the violinist received his first dollar tip: a woman threw money into the player’s violin case and continued to walk. A few minutes later, a man leaned against the wall to listen to him, but then looked at his watch and started to walk again. Clearly, he was late for work.

The one who paid the most attention was a 3-year-old boy. His mother hurried him along, but the kid stopped to look at the violinist. Finally, the mother pushed hard and the child continued to walk, turning his head all the time. This action was repeated by several other children. All the parents, without exception, forced them to move on.

In the 45 minutes the musician played, only 6 people stopped and stayed for a while. About 20 gave him money but continued to walk their normal pace. He collected $32. When he finished playing and silence took over, no one noticed. No one applauded, nor did anyone recognize him.

The violinist was Joshua Bell, one of the best musicians in the world. He played one of the most intricate pieces ever written, with a violin worth $3.5 million. Two days before his playing in the subway, Joshua Bell sold out at a theater in Boston and the seats averaged $100. His performance in the metro was a social experiment by the Washington Post about the perception, taste and priorities of people.

If we do not notice one of the best musicians in the world playing the best music ever written, what else are we missing? The story tells us that we tend to see only what we expect, and that our perception is heavily driven by social conditioning.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Update on Rubicon: Successfully Leveraging Legacy Ad-Tech Strengths

August 20, 2018 in Equities, Ideas, LettersThis article is excerpted from a letter by MOI Global instructor Jim Roumell, partner and portfolio manager of Roumell Asset Management (RAM), based in Chevy Chase, Maryland. Jim is a valued participant in The Zurich Project.

RUBI reported a very strong quarter indicating that the company has successfully leveraged its legacy ad-tech strengths to position itself to be one of the leaders in the programmatic buying and selling of online advertisements. RUBI has steadily gained market share over the past several months. In March 2017, Michael Barrett implemented a number of key initiatives when he became the company’s second CEO, building upon decisions made in 2016, that are working. The evidence is increasingly clear that those initiatives have turned around the company’s fortunes since its dramatic fall from grace two years ago when the protocols for online ad-buying changed and RUBI was caught flat-footed.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Disclosure: The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients, and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

Facebook: Growth to Exceed Expectations for Years to Come

August 20, 2018 in Audio, Equities, Large Cap, North America, Transcripts, Wide-Moat Investing Summit, Wide-Moat Investing Summit 2018, Wide-Moat Investing Summit 2018 FeaturedNiraj Gupta of GCI Partners presented his in-depth investment thesis on Facebook (Nasdaq: FB) at Wide-Moat Investing Summit 2018.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Niraj Gupta has over 25 years of experience analyzing and investing in publicly traded companies as a buy-side analyst/portfolio manager and a sell-side research analyst, with particular expertise in the technology, media and telecom industries. Prior to starting GCI Partners in 2008, Niraj was associated with Pequot Capital, Citigroup, Schroders and Goldman Sachs.

Moats: Measuring, Exploitations and Challenges, Quality vs. Price

August 20, 2018 in Audio, Case Studies, Commentary, Equities, Skills, Transcripts, Wide Moat, Wide-Moat Investing Summit, Wide-Moat Investing Summit 2018, Wide-Moat Investing Summit 2018 FeaturedMichael Lee of Hypotenuse Capital Management shared his wisdom and insights into the nature and features of moats at Wide-Moat Investing Summit 2018.

The full session is available exclusively to members of MOI Global.

Members, log in below to access the full session.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About the instructor:

Michael J. Lee is the founder of Hypotenuse Capital Management, an investment management firm based in Los Angeles, CA. Hypotenuse seeks to invest intelligently in exceptional leaders running extraordinary companies that deserve to win. Prior to founding Hypotenuse, Michael was a partner at Royal Capital Management in New York, a private equity associate at Parthenon Capital in Boston, and an investment banking analyst at Bear Stearns. He sits on the board of directors of the P.F. Bresee Foundation, a non-profit organization devoted to breaking the cycle of poverty and violence in Central Los Angeles. Outside of investing and philanthropy, Michael enjoys rock climbing, swimming and playing board games with his wife and two children.