Kenneth Jeffrey Marshall discussed his book, Good Debt Cheap: Value Investing in Bonds, Preferreds, and Other Fixed Income Securities, at MOI Global’s Meet-the-Author Forum.

Research director Alex Gilchrist hosts MOI Global’s Meet-the-Author Forum. The event brings together members and a select group of book authors in the pursuit of worldly wisdom. We are delighted to have an opportunity to inspire your reading.

Watch the conversation (recorded in late 2024):

About the book:

Most fixed income securities return barely better than a bank savings account. Those that promise more often carry big risks.

But value investors are able to find bonds and preferreds that outperform without increasing risk. They use common sense and simple analyses to identify fixed income securities that beat even exceptional stocks. Their advanced perspective reveals remarkable opportunities that others miss.

This book moves you towards becoming such an expert. You’ll learn to:

- SELECT great securities wrongly tossed into the junk bond dumpster.

- DODGE the conventional metrics that mislead others.

- FORESEE the exercise of embedded options.

- FOCUS on the yield measures that matter and skip those that don’t.

- ANALYZE contexts to view a preferred more as debt or more as equity.

- INTERPRET economic indicators to predict conversions and redemptions.

This book shares with you a model for gauging fixed income securities from a value investing perspective. It brings key concepts to life with case studies that span industries from franchising to software to manufacturing, and geographies from the U.S. to Germany to Japan. And it does all this with straightforward language and clear math that anyone can understand.

In developing your skills you’ll master the nuances of debentures, notes, convertibles, floaters, zeros, bills, munis, paper, corporates, and sovereigns. You’ll understand duration, solvency, covenants, seniority, liquidity, and credit ratings. You’ll breeze through basics like bond ladders, yield curves, and tap issues. Most importantly, you’ll develop the justified confidence necessary to navigate the biggest, oldest securities market in the world. Make your experience in fixed income one of insight and success with Good Debt Cheap.

About the author:

Kenneth Jeffrey Marshall is an author, professor, and value investor. He is the author of the McGraw-Hill book Good Stocks Cheap: Value Investing with Confidence for a Lifetime of Stock Market Outperformance, which was also published in Chinese; Small Steps to Rich: Personal Finance Made Simple; and Good Debt Cheap: Value Investing in Bonds, Preferreds, and Other Fixed Income Securities. He teaches value investing and personal finance at Stanford University; industry analysis in the masters in engineering program at the University of California, Berkeley; and investing in the masters in finance program at the Stockholm School of Economics in Sweden. He holds a BA in Economics, International Area Studies from the University of California, Los Angeles; and an MBA from Harvard University.

The content of this website is not an offer to sell or the solicitation of an offer to buy any security. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth on this website. BeyondProxy’s officers, directors, employees, and/or contributing authors may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated herein.

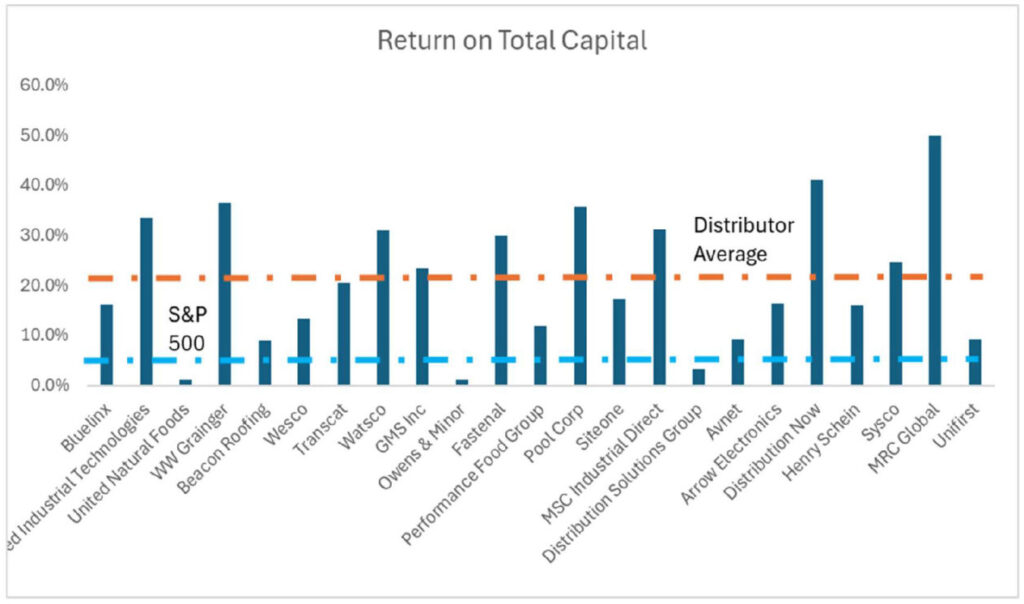

Source: Bloomberg, Firebird Value Advisors Research

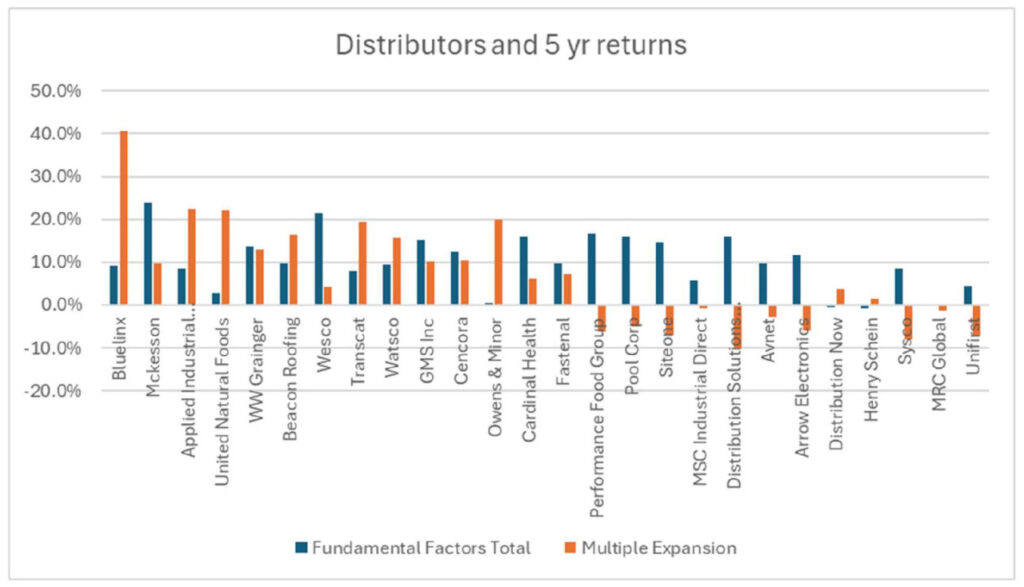

Source: Bloomberg, Firebird Value Advisors Research