We are pleased to share a profile of noted corporate leader Bruce Flatt, who has become synonymous with the enourmous value creation at Brookfield Asset Management (NYSE: BAM, TSE: BAM.A) over the past couple of decades.

Bruce joined Brookfield in 1990 and became CEO in 2002. Under his leadership, Brookfield has developed a global operating presence in more than 30 countries, while assets under management have grown to more than $600 billion.

This article is authored by Alex Gilchrist, a research associate at MOI Global.

Background

Bruce Flatt was born in 1965, in Winnipeg, the capital of the Canadian province of Manitoba, which shares borders with the US states of North Dakota and Minnesota. Bruce graduated suma cum laude in 1985 from the University of Manitoba. He trained as an accountant at Clarkson Gordon (later acquired by Ernst & Young), before joining Edper (the precursor of Brookfield) in 1989 as CFO of Edper’s financial hub, Hees.

In 2002, Bruce took on as CEO of the Edper controlled but publicly listed Brascan (Brascan changed its name to Brookfield in 2005). Since then Bruce has diversified Brookfield of its non-core cyclical holdings and centred the company around Asset Management, Real Estate, Renewable Power, Infrastructure and Private Equity. Brookfield currently has AUM in excess of $500 billion and over the last twenty years has achieved a CAGR of 17% per annum versus 6% for the S&P 500 over the same period.

Focus on incentives and transparency with shareholders

Soon after Bruce took became CEO of Brascan, he forced board members to hold a minimum amount of equity and increased holding periods of options issued to staff. By 2012, Bruce wrote that, “[Senior management is] commit[ed] to align our interests with yours by holding the vast majority of our individual net worth in Brookfield equity.”

Bruce increased transparency by emphasizing key metrics: “We have two principal financial performance metrics: operating cash flow and total return, both measured on a per share basis. We define total return as the change in underlying value together with distributions to shareholders.”

He communicates Brookfield’s investment goals clearly to shareholders: “Our goal is to invest capital for our clients in opportunities which have reasonable returns in a downside scenario (6% to 8% on equity), have the potential to generate good returns under most scenarios (12% to 15%), and in the upside cases will generate excellent returns (20% plus).”

A value investing approach has supported these goals

“We consider ourselves value based investors who own and operate real asset based businesses on a global basis.” Bruce emphasizes the importance of “purchas[ing] assets at a discount to their replacement cost, building a margin of safety into our acquisitions.” Obtaining such opportunities necessitates going against the crowd. Brookfield offices all contain a picture of the herd running of a cliff. This serves as a reminder employees of the contrarian mindset that is necessary to execute a value strategy.

Notable examples of this contrarian mindset include acquiring in 2002 “a 1.2 million square foot divided interest in Three World Financial Center… at a substantial discount to replacement value,” due to a hangover of fear from the September 2001 attacks.

Having maintained a strong balance sheet Brookfield went on a shopping spree for $4.1 billion of equity investment during 2008 and 2009. Many of these investments were made through “the purchase of debt for conversion to equity,” benefitting from over leveraged capital structures.

During the sovereign debt crisis, Brookfield bought “various distressed real estate and infrastructure investments” in Europe. In 2015, Brookfield was able to purchase assets in Brazil, “that would never otherwise have been available” with pricing “at fractions of replacement cost” that “discounted almost every negative scenario.”

Recently Brookfield has been able to utilise its competitive advantages of size and operating expertise to continue to find value in more expensive markets, acquiring a number of businesses that have “inherent defensive protections.” These include “a long-term contracted” “natural gas gathering and processing business for $3.3 billion” in Canada; as well as “an $11.4 billion portfolio of largely office and residential properties in four premier markets in the U.S,” that was acquired “with few competitors due to size and diversity of assets.”

Brookfield has also made use of more fully priced markets “to sell mature stabilized assets and redeploy the proceeds at higher yields or return the capital to our investors,” selling a total of $12 billion of assets in 2017.

Core principles

“Over time, we have found that the five most important principles to successful real asset investing are to: stick to what we know; ensure that we are diversified; buy at a discount to replacement cost; focus on quality assets and businesses; and finance with asset specific non-recourse debt.”

Brookfield employs a series of strategies to reduce risk:

1. Long-term leases – an average length of 10-20 years provides visibility to cash flows

2. Balance sheet strength and high levels of liquidity, allow Brookfield to withstand adverse economic circumstances implement its value investing strategy

3. Matching debt to asset characteristics – Often long-term leases are matched to long-term fixed debt

4. Debt expiration – Debt maturities are diversified over extended periods of time with only 10-20% being renewed annually

5. Non-recourse debt – Debt has recourse to the asset and not to the corporation

6. Make use of a diversified funding base including fundraising and preferred securities

7. Interest rates strategy – Locking in low long term fixed debt when available

8. Currency Risk is often hedged to USD

9. Transactional approach to emerging markets – Sell assets once they reach intrinsic value rather than hold on for longer in emerging markets to protect from future uncertainty

10. Cutting losses short – “[S]ome businesses, no matter how deep the discount to replacement cost, are just bad businesses.”

11. Avoid participating in structured financial assets

12. Being prudent in the face of development and approval risks

Increased size is an advantage to real asset investors

“[I]nfrastructure (as well as real estate and private equity) usually becomes more attractive as investments get larger. The competition for larger acquisitions is less and the sophistication required to operate these assets increases because of their complexity, therefore favoring large and experienced managers. Lastly, the larger assets acquired are generally also higher quality – they often have better counterparties, and stronger management teams. As a result we believe that our infrastructure business can scale to many times the size it is today.”

Re-organising Brookfield’s structure

Early on, Bruce realised the inherent potential of real assets to be attractive to a wider investor base, “aim[ing] to establish Brookfield as an asset manager of choice for institutions and other investors.”

“We expect that over the next 10 years, most institutions will increase their allocations of real assets to between 25% and 40%.”

Bruce re-organised Brookfield’s holding structure, grouping activities into key businesses and then listing each of these as listed partnerships both on the Toronto and New York Stock Exchanges.

Brookfield Asset Management sits on top managing and owning part of the share capital of the four listed partnerships:

- Brookfield Property Partners

- Brookfield Infrastructure Partners

- Brookfield Renewable Partners, and

- Brookfield Business Partners

Further to the listed partnerships, Brookfield also offers investors private funds and public securities. Total assets under management were in excess of $600 billion as of 2021. Neuberger Berman’s Charles Kantor, cites that through the listing of its partnerships and Brookfield’s significant contribution to its investment funds, Bruce created a “brilliant” structure of “lifelong entities” with essentially permanent capital.

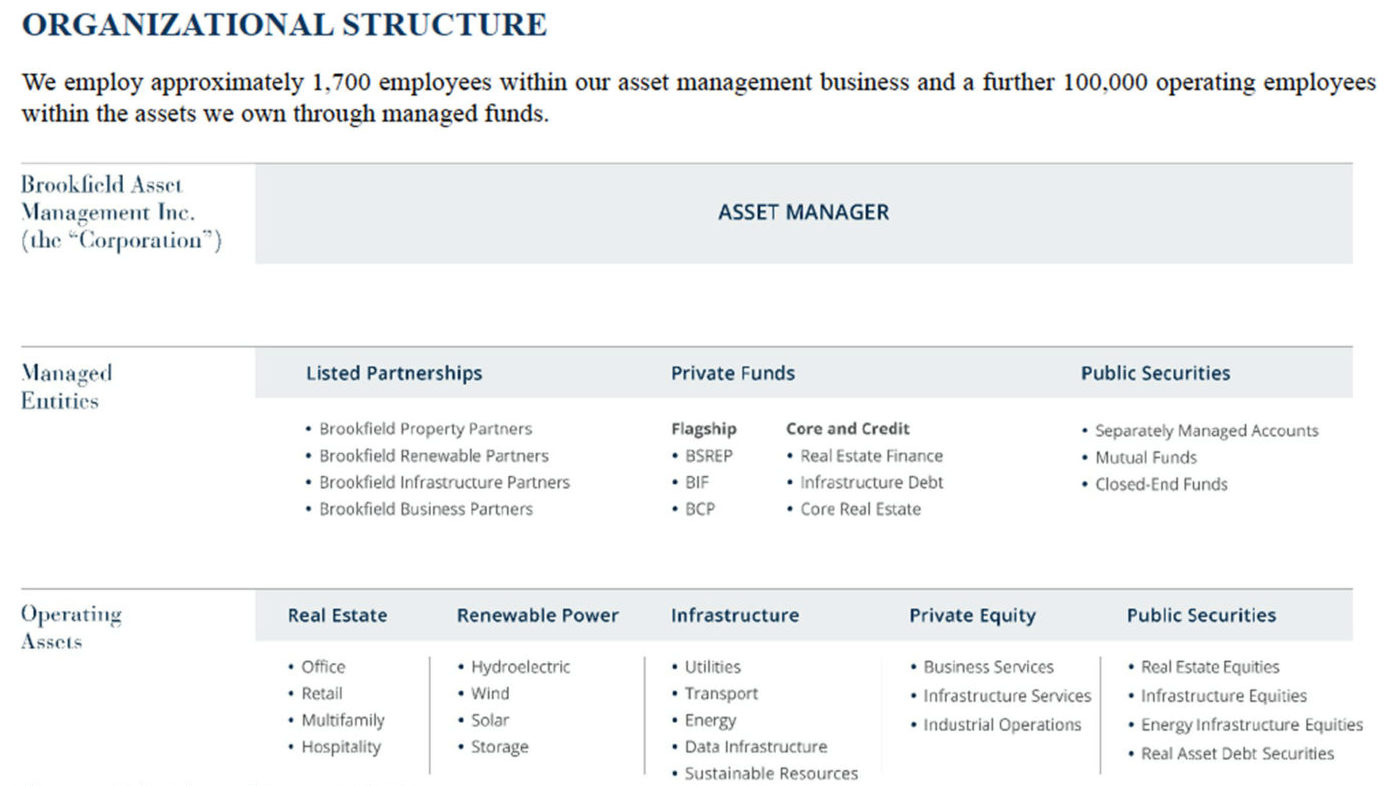

The diagram below, captures the relationship between asset management, ownership vehicles and operating assets.

(Source: BAM Annual Report, 2018)

Acquiring Oaktree

In March 2019, Brookfield announced its takeover of Oaktree. The acquisition allows Brookfield to offer a larger range of credit strategies. Simultaneously it represents the joining of forces of two titans in the value investing world. Howard Marks explained that Brookfield’s offerings mesh with Oaktree’s “without significant overlap and cannibalisation, with the same reputation, with the same growth record, with the same culture.” Furthermore “Oaktree is known for being able to ‘ring returns’” during sluggish periods “when it isn’t right for them [Brookfield] to grow.” Oaktree is a hard to replicate business that would have taken “a long, long time” for Brookfield to “buil[d] it ourselves,” in the “one area that we were lacking.”

The acquisition of Oaktree was financed with $2.4 billion of cash and the issuing of 53 million Brookfield shares. Bruce expects it to create value in excess of the 11% FCF yield that otherwise would have been returned to shareholders. Bruce’s remains focused as ever to “generat[e] increased cash flows on a per share basis and as a result, higher intrinsic value per share over the longer term.”

Antoine Gara’s description of Brookfield as “the safest growth stock on the planet” captures perfectly Bruce’s phenomenal achievements as an investor and operator at Brookfield.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

About The Author: Alex Gilchrist

Alex Gilchrist is a London-based research associate at MOI Global.

More posts by Alex Gilchrist