This article is authored by Ideaweek and Zurich Project participant David Eborall, Managing Director of SaltLight Capital, based in Johannesburg, South Africa.

Discovery Holdings is a financial services company that successfully uses behavioural economics to change customer behaviour (be healthier, drive better and, soon, be a better credit risk). The company is slowly integrating its data platform into some of the world’s largest insurers, such as John Hancock, AIG, and Ping An. Discovery is gathering a vast database on their customers’ health, what they eat, where they drive, how they drive, and, in the near term, what they spend their money on. Investors often talk about Kahneman and Cialdini in their investment processes; Discovery is actually using those principles to change behaviour.

Discovery is a two-year research project culminating in a new investment. Briefly, the overarching investment thesis is that Discovery is ‘closing the loop’ as a consumer aggregator in financial services and will continue in enhancing their customer’s lives through digital measurement + behavioural change.

Discovery offers ‘commoditised’ medical, life and P&C insurance products to their four million domestic and international customers. Within a few months they will be launching a banking platform. Some market participants think this venture is likely to sink the ship in a very competitive banking market.

It is my opinion that Discovery knows more about their customers than any other technology company I can think of – even Google or Facebook.

Let’s compare Google and Discovery: Google has a considerable advantage around knowing who you are and how likely it is that you will click on an advert.

Discovery knows what a customer eats, when they exercise, what their health issues are and is even experimenting with collecting DNA[1].

It would seem unconscionable that Facebook or Google would have such detailed information about their users. Yet, Discovery’s customers willingly provide their health records, their driving behaviour, their food purchases and, in a short time, a full picture of their spending habits.

It seems that by providing ‘earned’ incentives, customers are less likely to have qualms about privacy.

Strategically, Discovery has mimicked Apple’s integrated architecture playbook rather successfully. Clayton Christensen notoriously advanced the theory that excess profits are made in an interdependent product architecture[2].

An example would be helpful: Apple has created considerable customer switching costs by designing an integrated product architecture between disparate products (say a watch and a phone) with the addition of a ‘services’ layer (the Apple App Store) on top of their products. The App Store creates network effects that binds third- party developers and multiple devices together with Apple’s customers – continuously growing the value of being an Apple customer as one adds each device and each app.

Discovery similarly integrates and differentiates their products with an ‘incentive’ layer on top. The incentive layer, called Vitality, interlinks the various financial services products and is the ‘secret sauce’ to lower lapse rates and lower overall insurance claims.

Most insurers are passive observers of their customer’s lifestyle habits. At best, they manage anti-selection risk and avoid ‘sickly’ customers through pricing. Vitality uses modern behavioural finance techniques[3] as a ‘carrot’ and ‘stick’ to actively change behaviour. Customers are incentivised to be more active, drive more carefully and save more for retirement. These activities reduce the insurance claims down the line and Discovery ‘shares’ the saving with their customers.

More beneficially to customers over the long term (if a Vitality member meets their goals on physical activity, routine tests and adherence to programmes) management indicates that those who use the Vitality product are likely to add years to their life[4].

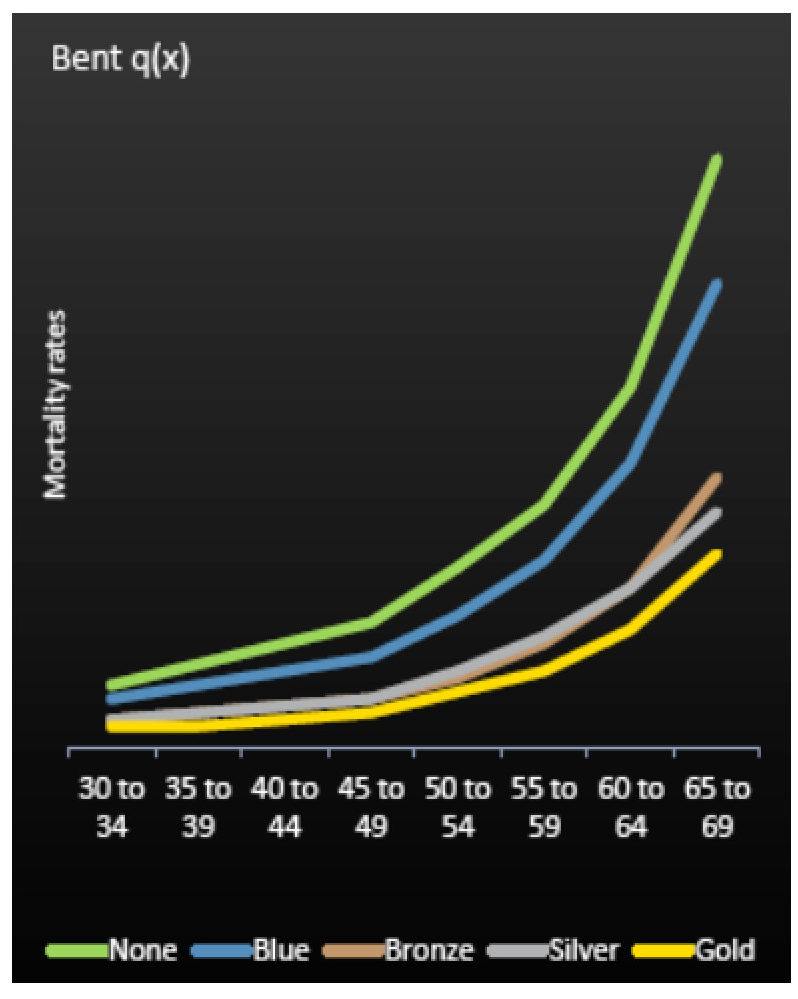

Mortality Bent Curve (by Vitality Status)[5]

A Widening Moat

Discovery has two elements that create a formidable moat: (1) the best ‘marshmallows’ and (2) better data leading to better pricing.

The best ‘marshmallows’

Discovery’s insurance products are as much as a ‘grudge purchase’ as any other. In my discussions with customers, there are more than a few that would love to leave Discovery – yet they don’t. “Why not?”, I ask. Customer response: “oh, they give me 30% off flights” and “I’d lose my gym discount”.

Discovery seems to have successfully tapped into the depths of the human psyche by giving customers the best Marshmallows[6] (flights, coffee, discounted gym memberships etc) resulting in suppliers (including medical practitioners) being forced to follow them. Discovery subsidises 1m flights per year (22 planes per day) and 70,000 gym visits per day. Customers forgive Discovery despite have a reputation of being tight-fisted in paying claims.

Benefits like these are, theoretically, easy to replicate – competitors should simply be able to buy them. However, in reality, competitors are severely disadvantaged. With a 40% share of the private medical insurance market, no competitor has been able to match (on a per unit benefit cost basis) Discover’s benefit range. Discovery has contractually locked up the most- desired consumer-incentive suppliers (airlines, gym brands, coffee chains and healthy gear) by being early but also by providing significant market power.

Therefore, competitors are always at a price and value disadvantage to replicate the same benefits. This has created a positive feedback loop where Discovery directs more customers to a supplier, which means better terms (more transferred value and lower pricing), which, in turn, means more customers.

The result: Discovery’s supplier advantage has forced many competitors to capitulate and rather compete on distribution or other factors.

Better data leading to better pricing

If ‘Big Data’ is the new moat, Discovery is years ahead of its one-dimensional competitors. Most life insurers price their life insurance products using standard actuarial life tables with some idiosyncratic adjustments (smoking or demographic factors) to account for an estimated mortality. Discovery has a substantially wider data advantage to pin-point an individual’s life expectancy and other behavioural tendencies with superior accuracy[7].

This ‘commoditised product’ + ‘differentiated layer’ strategy has been rolled out in each product segment that Discovery has entered into (retirement products, short-term insurance and, in the future, banking).

Why go into banking?

The purpose of starting a bank is to (1) know where/how a customer is spending their money and (2) grab more share of a customer’s wallet. As with health data, Discovery is likely to utilise this data to change a customer’s spending and savings behaviour.

Discovery is already deducting points if a customer puts a chocolate rather than a lettuce in their shopping basket. I speculate a scenario where their app deducts points if you haven’t saved ‘x’ in a particular month?

Discovery’s banking initiatives come with significant risks as the South African banking sector has extremely high barriers to entry. The ‘benign oligopoly’ that has existed for decades is unlikely to easily allow new entrants. Discovery’s target market is the middle to upper income cohorts – the ‘bread and butter’ of the stodgy oligopolistic incumbents. History has shown that, in the last two decades, the only new entrants that have succeeded have targeted the ‘unbanked’.

So why could Discovery possibly succeed?

Think back to Apple. Apple succeeds because of its integrated product eco- system. The value of a customer’s individual products become more valuable as each new product (Watch, iPad) is added to the platform. The differentiating layer (the App Store) binds these pieces together. Similarly, Discovery has followed this same process. The medical insurance market in the early 2000s had major incumbents offering a commoditised product. Two decades later and Discovery has 40% market share of the private medical market because they offered a ‘differentiated layer’ (Vitality) on top of a commoditised product.

By creating an integrated solution, customers accumulate more value by moving across to Discovery’s commoditised products. The sum of value is greater than the parts[8].

Furthermore, given that banking products have a smaller absolute cost than insurance products, it makes strategic sense to use a banking product as a ‘gateway’ product that could be leveraged to encourage non- customers to buy other Discovery products.

These competitive advantages raise my view of their odds of success with a significant ‘market-share grab’ opportunity[9].

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

[1] Source: https://www.humanlongevity.com

[2] Theory of Interdependence and Modularity: The Innovator’s Solution, Clayton Christensen (chapter 5)

[3] Daniel Ariely is a consultant to Discovery (link) and much of his work has been implemented in changing customer behaviour.

[4] Source: Company: After 10 years on Vitality, average reduction in mortality is 16%

[5] Source: Company: The reduction in mortality (actuarially expressed as the probability of death) by age 65 is significant on the highest levels (gold status) of activity. The lower the value on the y-axis, the lower the probability of mortality.

[6] Marshmallow Test: https://en.wikipedia.org/wiki/Stanford_marshmallow_experiment

[7] For example, based on their data, there is a high correlation to indicate that healthier people are a better credit risk (if you’re disciplined enough to go to a gym three times a week, you’re likely to be more disciplined in paying your bills).

[8] For example: A discovery health customer obtains a larger discount on a flight purchase if they use a Discovery Credit Card to pay for it.

[9] Most banks have their own loyalty products however they are significantly inferior in isolation. Furthermore, they lack the smooth integration that Discovery has.

About The Author: David Eborall

David has thirteen years' experience in financial services in South Africa and the United Kingdom. He has previously worked for Morgan Stanley, Rand Merchant Bank and KPMG across asset classes in research and trading positions. Prior to founding SaltLight, he co-founded FeverTree Finance, a specialist financial services firm involved in private equity, structured finance and retail credit. He has a B.Com (cum laude), Hons from the University of Johannesburg, CA(SA) and CFA and studied at London Business School in their Entrepreneurship Program.

More posts by David Eborall