This post by John Huber is excerpted from a letter of Saber Capital Management. John writes about his investment approach at Base Hit Investing.

“The outside world can push you into Day 2 if you won’t or can’t embrace powerful trends quickly. If you fight them, you’re probably fighting the future. Embrace them and you have a tailwind.” –Jeff Bezos, 2016 Amazon Letter to Shareholders

Jeff Bezos wrote about four things that an industry-leading company must do to stay on top (or in what he calls “Day 1” – the healthy growth phase of a company’s life cycle, as opposed to “Day 2”, which is the beginning of a company’s demise). One of the keys to staying hungry, according to Bezos, is to embrace these big, sweeping, fundamental trends.

One of these big trends is the Chinese ecommerce market, which has recently passed the US as the largest in the world, and yet is still growing at around 20% annually.

Buffett once talked about companies he considered to be what he called “the inevitables” – durable businesses that he felt were sure to do well over time due to structural competitive advantages. The Chinese ecommerce market could be described as one of these “inevitables”.

Studying the online shopping market in China led me to learn about other industries benefiting from the same general tailwind – mobile advertising, video consumption, mobile payments, cloud computing, and many other related industries are certain to grow significantly over time as tens of millions of people in China enter the middle class each year and allocate higher percentages of their growing purchasing power toward these areas.

And unlike burgeoning industries of yesteryear such as automobiles or airlines that produced rapid growth in volumes but created little to no lasting value for owners, the Chinese ecommerce and digital advertising market are dominated by a select few companies that are highly profitable, well-managed, and are well-positioned to create enormous value from these industry tailwinds over time.

As Bezos said in his letter, “these big trends are not that hard to spot” – and the growth in China’s online shopping industry is certainly not hard to spot. But just as large-cap stocks can occasionally become sizably mispriced despite their wide following, the usefulness of an insight does not necessarily correlate to how original it is. In other words, it is widely known that China’s ecommerce market is huge and rapidly expanding, but there are still plenty of opportunities to capitalize on that obvious trend as investors.

While there will be many bumps in the road, productivity and consumer spending will continue to rise in China over time, and some of the best companies in the world will come from business models that capitalize on this extremely powerful fundamental trend.

One of our investments that will benefit immensely from this tailwind is Tencent Holdings.

Tencent (TCEHY)

In June, I did a presentation for MOI Global (the value investing community) on Tencent Holdings, a company we invested in late last year.

Tencent is a Chinese internet holding company with one of the most powerful network effects in the world. The company operates in numerous businesses that generate significant free cash flow, take very little capital to grow, and have huge runways for growth in China and around the world. These businesses and investments consist of video game publishing, music and video subscriptions, ecommerce, mobile payments, and online advertising among other assets.

But the company’s crown jewel is WeChat, which is a mobile app that is unlike any application that exists in the West. WeChat dominates China, and its 963 million users spend more time on WeChat than US users spend on Facebook and Instagram combined. And it’s far from just a messaging and social media application. WeChat is used for just about everything in China including messaging, work communication, calls, social networking, online shopping, paying bills, transferring money, and much more. Incredibly, one-third of WeChat users spend more than 4 hours a day inside the WeChat universe.

This is a clip from an Economist article that outlines a sampling of what WeChat is used for in China:

“Like most professionals on the mainland, her mother uses WeChat rather than e-mail to conduct much of her business. The app offers everything from free video calls and instant group chats to news updates and easy sharing of large multimedia files…

“Yu Hui’s mother also uses her smartphone camera to scan the WeChat QR (quick response) codes of people she meets far more often these days than she exchanges business cards. Yu Hui’s father uses the app to shop online, to pay for goods at physical stores, settle utility bills and split dinner tabs with friends, just with a few taps. He can easily book and pay for taxis, dumpling deliveries, theatre tickets, hospital appointments and foreign holidays, all without ever leaving the WeChat universe.”

WeChat is an asset that has barely been monetized yet, but is in prime position to capitalize on numerous fast-growing industries like mobile advertising, online shopping, and mobile payments.

Tencent has a truly exceptional collection of businesses. Despite a vast untapped potential in some of those markets referenced above, the company is already highly profitable. Revenue is growing at close to 50% annually. Thanks to 30% net profit margins, Tencent turns a good chunk of that revenue into free cash flow for the company to reinvest. I estimate that the company is producing about 35% returns on incremental capital investments, and is growing its already sizable $8 billion of free cash flow at 40% per year.

Growth obviously will slow down at some point (40-50% growth rates only last so long), but given its unique competitive position and the huge size of the markets it operates in, there is likely a very long runway ahead for the company, despite already being one of the most valuable companies in China.

To summarize, there are four things I like about Tencent: the huge network effect of WeChat, the massive runway for growth, the high returns on capital and significant free cash flow (despite barely scratching the surface of WeChat’s potential), and the fact that the company is run by its driven, long-term focused founder who remains one of the major shareholders.

We bought shares of TCEHY in late 2016 for an average price of $25.

The stock has risen significantly (it has gained around 80% year-to-date), and I have no idea where the stock goes in the next year or so (as is the case with any stock), but I think over a long period of time Tencent shares will likely compound at a rate that roughly mirrors the growth of the company’s intrinsic value – and I think this rate of compounding will be quite high (15-20% annually) for a number of years to come.

The slide presentation further details my thoughts on Tencent, and also outlines how I think about the valuation of Tencent, which I view as a long-term compounder.

Large Caps

The tailwind of these big, external trends is an insight (albeit not a particularly unique one) that I’ve been thinking about this year. Another insight that I feel is much less commonly held is that large-cap, well-followed stocks can be excellent investments at times. As I’ve mentioned before, I don’t intend to be investing in large-caps exclusively. On the contrary, I am always hunting for off-the-radar ideas that might be undervalued. But sometimes large-caps can offer significant value, and my objective is to find value, not to win style points by locating the most unique investment idea.

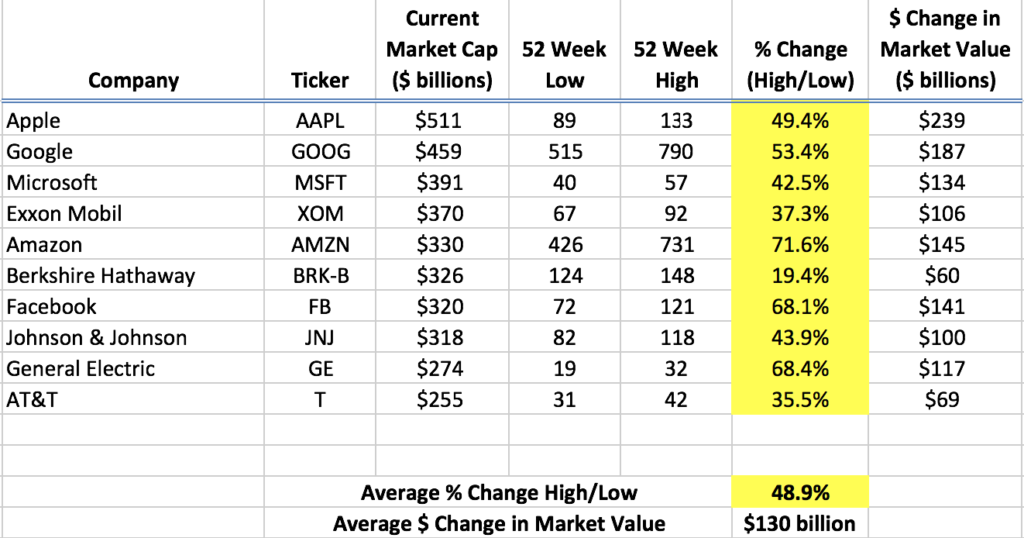

As a quick summary, here is a chart that I put up in last year’s mid-year letter, demonstrating how much large cap stocks bounce around:

Large Cap Stocks vs. Small Cap Stocks

Top 10 Largest Companies in S&P 500 (as of 6/24/16)

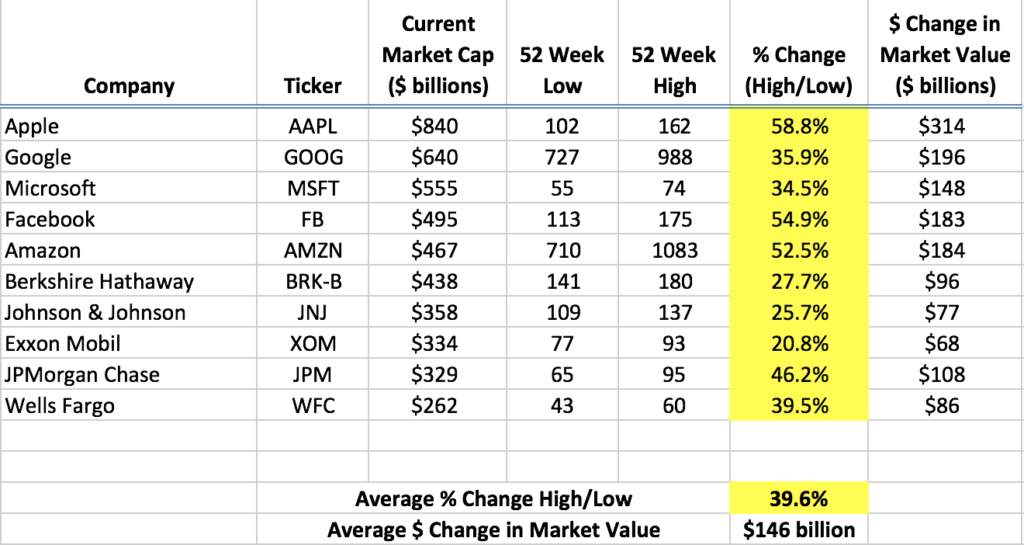

Here is the same basic chart updated for 2017:

Top 10 Largest Companies in S&P 500 (as of 8/15/17)

What’s remarkable is that even with volatility being at all-time lows for much of the past year, mega-cap stocks – ten of the largest, most well-followed companies on the planet – still saw an average of a 40% gap between their 52-week high and low prices.

Despite the army of analysts poring over unlimited bits of information that supposedly increases market efficiency, Apple is currently valued at a whopping $300 billion more (or nearly 60%) than it was just one year ago.

There are many others in that list that have seen similar fluctuations. In fact, our three largest investments in the last 18 months have come from capitalizing on significant downward fluctuations in the stock prices of very durable, very large, and very well-positioned companies with predictable earning power and good balance sheets. All three of these investments were shunned by many would-be value seekers who felt like they had no “edge”. While they most likely lacked an informational edge, they didn’t realize that a time-horizon edge is often more significant, and this type of edge can be used to invest in stocks of all sizes.

Along those lines, Apple remains our largest position, although it obviously doesn’t offer the same value as it did a year and a half ago when we first started investing in it. For new investors who want to read what I thought about Apple, I summarized my views here, and also in the 2016 letter.

Apple falls into what I refer to as “Category 2” investments – stocks of durable, mature companies that occasionally get mispriced by Mr. Market. These are stocks that might offer 30-50%, or even 100% on rare occasions, but typically will be sold as they approach a more reasonable value.

The ideal investments are the “Category 1” investments, or the compounders – businesses that produce high returns on capital and have long runways for potential growth.

The nature of the market is that most investment opportunities will be of the Category 2 type, while the biggest winners will be from Category 1.

I continue to seek out investment opportunities in both categories, and as category 2 investments become more fairly valued, I will look to reinvest capital into more undervalued ideas.

Returns are based on the “Saber Capital Portfolio”—a real money account that is managed alongside all other accounts. I also refer to this as Saber’s model portfolio. Performance data of this account is produced directly from Interactive Brokers. Returns are not audited. It is important to note that each client may experience slightly different results from the model depending on the timing of deposits, withdrawals, the opening/closing of the account, the fee structure specific to each account, and other timing issues. The valuations of your investments at the time of purchase may be significantly different than the valuations at the time of purchase in the model because of these timing issues. I expect the net results of the model account to roughly equal the results of client accounts over time, although there can be no guarantee because of the timing issues referenced above. The gross returns of the Saber Capital Portfolio are taken directly from Interactive Brokers. The net returns are estimated using a 1% management fee and 15% performance fee. Your net returns could vary from the model depending on the fee structure of your account. Your personal account statements with your account specific performance net of all fees will be coming in the mail each quarter, and can also be accessed anytime online. Please note that any performance fees earned during this year will show up in the following year’s 1st quarter statement. Also note that the time weighted return (TWR) on your account specific performance summary is net of all fees.

About The Author: John Huber

John Huber is the portfolio manager of Saber Capital Management, LLC, a value-focused investment firm that manages separate accounts for clients. Saber’s objective is to compound capital over the long-term by making investments in undervalued stocks of high-quality businesses. John writes about his investment approach on his website, Base Hit Investing.

More posts by John Huber