This article is authored by Sean Stannard-Stockton, president and chief investment officer of Ensemble Capital.

Most people think that if something is good, more is always better. But that’s rarely true. One of the most important concepts in economics, The Law of Diminishing Returns, shows us that each new unit of something good tends to produce less good than the previous unit. The easiest way to think about this is eating candy. No matter how much you love chocolate, the 10th piece doesn’t give you as much pleasure as the first piece and the 100th piece makes you sick.

Despite the economic roots of this concept, many economists (and much of Wall Street) think this issue doesn’t apply to the diversification of equity portfolios. But as we’ll show, more is not always better and the value of diversification diminishes much faster than most people think.

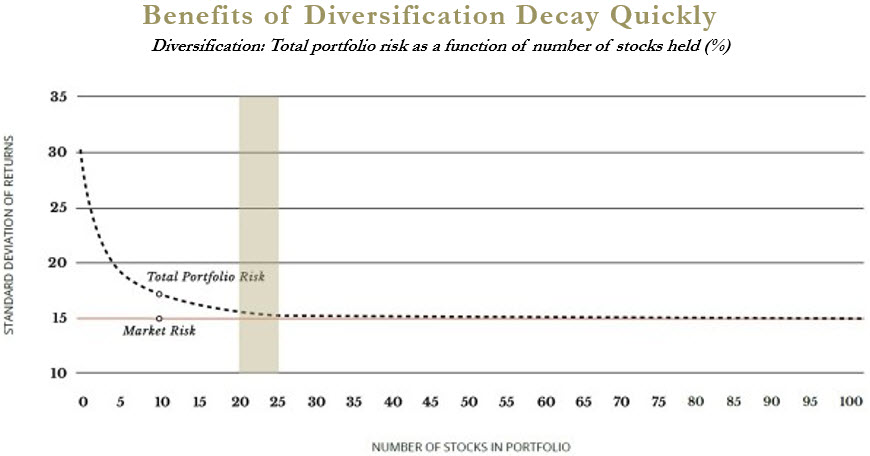

The chart below, based on data from the classic book A Random Walk Down Wall Street by Burton Malkiel, shows how adding a third or seventh or fifteenth position to an equity portfolio materially reduces the volatility of returns. However, by the time a portfolio has twenty or so holdings, the incremental reductions in portfolio volatility from new holdings is very small.

Burton Malkiel, a strong proponent of diversification and a skeptic of active management, says in the book:

By the time the portfolio contains close to 20 equal-sized and well-diversified issues, the total risk (standard deviation of returns) of the portfolio is reduced by 70 percent. Further increase in the number of holdings does not produce any significant further risk reduction.

Malkiel’s research was based on randomly selecting stocks, so if an investor builds a portfolio of 20 energy companies or 20 technology companies, their portfolio will exhibit far more volatility than the chart suggests. But so long as the members of the portfolio are companies with diverse end markets, business models, etc, a purposely selected (rather than randomly selected) portfolio of 20 or so companies is very likely to capture the bulk of available diversification benefits.

Of course, investors do not seek only to reduce risk. They also want to maximize returns. If you are actively picking stocks that you hope will outperform, it becomes clear very quickly that it is quite hard to find a lot of good ideas. A realistic investor knows that even their best idea has a very good chance of underperforming, despite their best efforts. So a smart investor will build a portfolio of a number of stocks that they expect will beat the market. But there are limits to the number of stocks an investor can know well and have a reasonable basis to believe will outperform. So while more stocks will reduce volatility, it also requires adding stocks to the portfolio that the investor believes has less potential to outperform.

A 50th or 100th “best idea” isn’t likely to add much in the way of potential outperformance. But it also isn’t likely to add much in the way of lower volatility or reduced risk. So why do most professionally managed, active investment portfolios own well over 100 stocks?

There are two key reasons for professional active investment managers to own way more stocks that they need to.

The first is because it helps them not underperform by too much, but the price they pay is reducing their potential to outperform. If you own 25 rather than 200 stocks, the volatility of your portfolio won’t be much higher. But the tracking error of your portfolio to the benchmark will likely be higher. That’s because while your portfolio will be diversified from a volatility standpoint, it will be quite different from the benchmark. This is called having a high “active share” and research shows having it is a critical key to potential outperformance. But having a portfolio that is quite different from your benchmark means that while it might not be more volatility, it won’t “track” the benchmark as closely. Most managers don’t have any confidence that their clients (or their bosses) will tolerate any length of time where they underperform, so they own more stocks in order to reduce their tracking error. But this has the effect of greatly reducing their ability to potential outperform over time.

The second key reason is that the collective market cap of the stocks you own in your portfolio places a limit on how much assets you can manage in your strategy. A portfolio of 25 stocks will have a collective market cap that is lower than a portfolio of 200 stocks, so the manager, who gets paid for managing more assets, can make more money if they manage a strategy with more stocks in the portfolio. This is why you see relatively focused funds close their doors to new money, while the typical, excessively diversified fund rarely closes to new investors.

So diversification is great, but its benefits are realized with far fewer stocks that most people realize. If your goal is to match the market performance (which is a perfectly reasonable goal) than buying every stock in the market (ie. broad diversification) makes perfect sense. But if your goal is to beat the market, the level of diversification should be optimized, not maximized. What you want to avoid at all costs is attempting to beat the market by investing in strategies that are excessively diversified.

Thanks to Lawrence Hamtil of Fortune Financial for urging us to address this topic. Read Lawrence’s blog.

Readers are encouraged to contact Ensemble Capital directly with thoughts. The information contained in this post represents Ensemble Capital Management’s general opinions and should not be construed as personalized or individualized investment advice. No advisor/client relationship is created by your access of information on this site. Past performance is no guarantee of future results. All investments in securities carry risks, including the risk of losing one’s entire initial investment. If a security is mentioned in this post, you will find a disclosure regarding any position Ensemble Capital currently has in the security. Ensemble Capital is a discretionary investment manager and does not make “recommendations” of securities. Each quarter Ensemble Capital files a 13F, which discloses all of their holdings. Please contact Ensemble Capital if you would like a current or past copy of their 13F filing.

About The Author: Sean Stannard-Stockton, CFA

Sean is president and chief investment officer of Ensemble Capital and oversees the firm’s services for foundations and philanthropic families. Before joining Ensemble Capital, he was a member of a private client advisor team working with high net-worth individuals at Scudder Investments. He holds a BA in Economics from the University of California, Davis, the Chartered Financial Analyst designation, and is a Chartered Advisor in Philanthropy.

More posts by Sean Stannard-Stockton, CFA