This article is excerpted from a letter authored by Will Thomson and Chip Russell, managing partners of Massif Capital, a value-oriented investment partnership focused on the small- and mid-cap space, with special attention on industrial and commodity-related businesses.

Over the last decade, there has been a growing body of analysis examining the rise of intangible investments and how accounting standards have made the job of ascribing value to intangible heavy businesses (and investments) more difficult.[1] For a company that invests heavily in intangible assets, the recording of capital spent on investment has migrated from the balance sheet to the income statement-making reported earnings and book value less descriptive of economic value.

Despite this trend, we are beginning to see significant capital flow into real asset businesses (where the primary investment and value creation is derived from tangible rather than intangible resources). In the last 24 months, roughly 51 SPACs have either gone public or been announced that are capital-intensive businesses focusing on the energy transition. These companies have IPOed for a combined ~$15 billion. Today, the combined market capitalization stands at ~$84 billion. The share-price of those firms has grown an average of over 200%.

Capital flowing to SPAC’s certainly does not represent all money flowing to real asset businesses, but the trend provides a decent proxy for the current sentiment. A sentiment supported by think tanks and companies the world over. The Rocky Mountain Institute, an energy-focused think tank, expects $40 trillion to flow into new low carbon assets before 2050.[2] The critical link between all these investments, though, is that the companies involved are all either growing fast (some of them are young and growing fast), turning over their balance sheets quickly, investing heavily in next-generation processes and technology, or adjusting business models that in some cases (for example steel, bulk chemicals, cement, etc.) have not changed in more than fifty years. The world of capital-intensive tangible asset businesses, long considered boring compared to the exciting tech world, is fast becoming a driver of economic change.

Given the impetus and interest in financing solutions to combat climate change, paired with technologies in the energy, transportation, materials, and utility industries that appear on the cusp of large-scale commercial adoption, we feel comfortable stating that:

1. We have not seen this level of future growth in capital intensive industries for decades.

2. Investors searching for high growth opportunities have not had capital intensive businesses in their hopper of growth opportunities over roughly the same time horizon.

This has profound implications and raises important questions. Namely, how do you value high growth capital intensive tangible asset businesses?

Like the dilemma faced by value investors who have had to wrestle with the growth of intangible assets over the last twenty years, this new dilemma requires that investors’ analytical approach be flexible enough to understand the crucial drivers of value in changing industries. A failure to adjust means there is a blind spot developing in the market. Typical surveyors of tangible asset businesses are not accustomed to the growth trajectories they might experience, and investors familiar with growth models are not usually, in our experience, acquainted with capital intensive industries.

If we accept this proposition, there are two implications:

First, we need to dissociate “tangible asset businesses” from “mature businesses.” Most investors today have little investing experience before 1965. Innovation since 1965 (technological or otherwise) has, as aptly put by Peter Thiel, been in the form of bits rather than atoms. We associate growth with software companies and capital-light business models. Real asset businesses can grow, but often at or below some GDP (or sector-specific) growth rate. Valuation techniques often rely heavily on steady-state terminal value assumptions. Today, many capital-intensive businesses are becoming growth companies, if for no other reason than the end markets they serve are still nascent themselves[3] and/or are rapidly changing. Thus, it is difficult to describe the characteristics of a mature business in such a market. How we value capital intensive companies when we have no prior experience with new end-market characteristics is a question to answer.

Second, growth capital investors must refamiliarize themselves with evaluating balance sheets. If strategic resources of the market’s next wave of growth companies and disrupted industries are tangible assets, understanding a company’s prospects for creating value will be found on the balance sheet.

We believe project-focused companies offer a legitimate proxy for how to ascribe value to capital intensive growth businesses to chart a path forward. An important point made by Miller and Modigliani in their seminal paper 60 years ago[4] was that the value of a company could be thought of in two parts: the first, a steady-state which assumes a firm can sustain its current profitability into the future; and second, the present value of growth opportunities which is a function of the magnitude of investments, return on investment and the period of time that investment opportunities are available.

Single project mining firms, the best and most descriptive example of a project company, almost exclusively derive their value from the second variable in Miller and Modigliani’s formulation. They are mostly companies with no terminal value. For many, management does not even conceive of a permanent steady-state and does not assume the firm can sustain profits into the future beyond a single project. These firms are growth companies, with little possibility of a terminal value or consistent risk expectations on future cash flows.

These attributes are not unique to project companies but occur far more frequently than in mature, stable operating businesses. Johnson and Johnson rarely has an event that causes a fundamental change to the operating business’s risk or an event resulting in investors questioning its likely long life to come. Project companies are different because asset development can fundamentally change the risk profile of investment from one year to the next, and because those projects have an end.

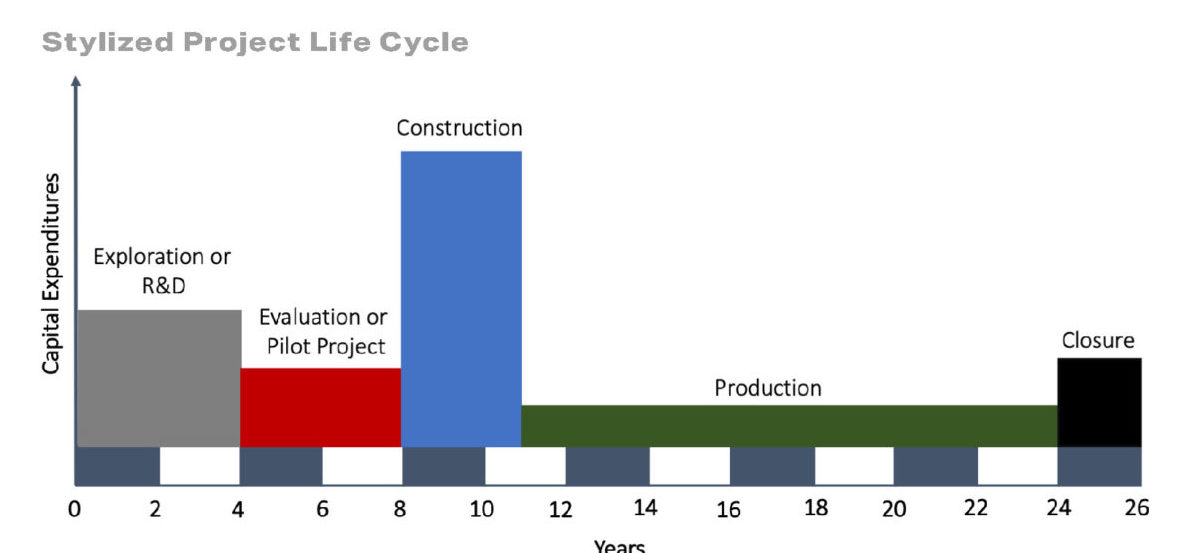

From a minority shareholder perspective, the risk of development uncertainty decreases as management shepherds a mining project through development and production. We can reflect that change by reducing the discount rate applied to future cash flows. A stylized life cycle of a mine or any significant capital-intensive property, plant and equipment (steel mill, oil refinery, wind turbine, electric vehicle charging network, utility-scale battery station, hydrogen electrolyzer, etc.) is as follows:

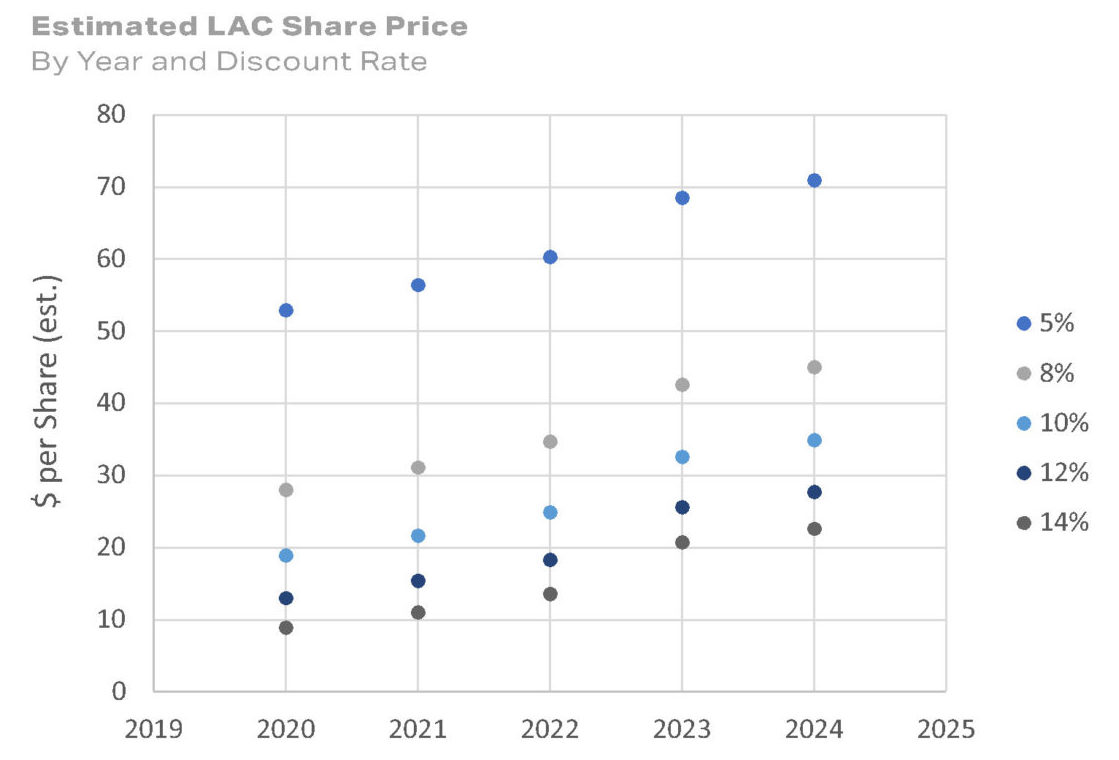

At the early exploration stage, the risks are at a maximum, as is the optionality. A land package could hold a world-class asset that is easy to mine, it could have a mediocre asset that is difficult to mine, or there could be nothing of interest. Speculative investment opportunities exist, but this is the venture capital stage of project development.[5] Many of the SPACs currently coming to market are of this nature: the risk is high, the timeline to development uncertain, and payoff cloudy. R&D at incumbent capital-intensive firms, such as attempts at developing hydrogen-powered steel furnaces or cement clinkers with carbon capture, are also at this stage. There is potential energy, but no evidence of a catalyst and measurement of that energy is difficult. As the project advances, the risks that future cash flows are never earned decreases. Lithium America (LAC)[6], a junior lithium miner with two development assets, is illustrative of this dynamic.

We first evaluated LAC in April of 2019 and invested in February 2020. At the time of our investment, a discounted cash flow analysis of the firm’s projects produced a $6.5 valuation versus the share price of roughly $2.8. Today, a year later, we think LAC is worth $18 per share. What changed over the last 12 months such that we revised our estimate up by 170+%?

1. The risk associated with project development, and;

2. Time to production

LAC’s South American brine operation secured sufficient funding to bring the project to commercial production (financial de-risking). Their North American clay project received critical environmental permits and made substantial progress on the firm’s processing technology to turn lithium-sulfur into lithium salts (operational de-risking). These developments allowed us to lower the discount rate used on future cash flows to reflect where LAC sits in their development cycle. LAC is also one year closer to production, which means cash flows are accretive to the firm sooner.

The chart above shows the dynamic between time to production and the risk of production today.

This risk reduction quality of project companies is not unique to the world of tangible assets but is undoubtedly underappreciated. It is one reason why early-stage natural resources projects remain some of the more interesting reoccurring opportunities in public markets. The wasting nature of the assets means there is a continuous pipeline of new firms and opportunities to assess. Capital-lite growth businesses can be evaluated similarly (dynamically adjusting the risk and time to cash flow realization). There are some important differences between tangible and intangible asset growth companies, namely around pricing models and resulting earnings power.

In either scenario, a shared thread among most growing businesses is elevated volatility. Perhaps obvious, but again, consider the valuation ramifications. Discounted cash flow analysis treats volatility as risk, and value is subtracted from the business. Option analysis treats volatility as an opportunity and rewards the potential asymmetry. Growth investors frequently think in terms of options, traditional value more in terms of cashflows. Tangible asset businesses, which are historically the value investor’s domain, now need to be evaluated with greater attention being paid to both aspects of the companies future, with investors’ judgment determining where the majority of the weight lies in the final intrinsic value calculation.

We want to poise an open question: how comfortable are you valuing a capital-intensive, pre-revenue R&D operation, selling a compelling product into a market that does not yet exist (hydrogen producer, electric vehicle charging company) or an incumbent that fundamentally changed their business model without changing their product (green aluminum, or steel, a coal-burning utility that is now a fast-growing renewable utility)?

A second commonality between growth companies and project companies is the uncertainty about terminal value assumptions.

In a way, project companies can be simpler to evaluate as you can exclude the terminal value from the analysis and focus on the period in which the firm plans to invest, extract, and monetize its resource. Growth companies that intend to remain a going-concern business do not have as neat of an end-date to point to. However, the practice of bifurcating the value of a growth phase vs. a mature phase can be beneficial (and is how Miller and Modigliani laid out their taxonomy of value). It is incomplete to suggest that a project company’s value is merely the value of their current endeavor. The management team may very well expand via acquisition or geological discovery if the business is a miner. However, like a growth company feeding into nascent end-markets, determining the value of that ‘could be’ is exceptionally challenging.

More broadly, the invisibility of a terminal value (or a mature state) impacts time horizon expectations. For an investor, this becomes particularly important at the portfolio level. When considering a return calculation, the time element is one of three variables: the value you buy, the price you pay for that value, and the time it takes for that value to be realized. Focusing on two of those variables (the value you buy and the price you pay) without due consideration for the third is a mistake, albeit a common one.

Indeed, one could attribute the froth in current clean-tech SPAC valuations to a distortion in the perception of time. Too many valuations are based on theoretical market sizes (just considering theoretical future value) rather than on a balanced view of all three variables. The result is that the necessary growth rates to achieve the value suggested by market prices neglect to consider the physical nature of most of the products sold by SPACs. Real asset businesses do not grow property, plant, and equipment or produce goods at the speed of software firms, nor can they be valued in the same way. Large quantities of capital chasing returns are being invested in businesses with limited nearterm economic prospects. Near-term prospects in the world of real assets or tangible asset-heavy businesses is five to ten years, which is likely not what the market means when it thinks near term.

An excellent example of the importance of time when evaluating a project with no terminal value is the single asset mining firm Lucara Diamonds. A business focused on monetizing a single balance sheet item and has a life cycle that runs from development to harvesting and the asset’s eventual closure. A project company has a point of maximum theoretical value, after which the value declines. This feature of project companies is even more pernicious when the company is a natural resources business with a depleting asset. It also means that the best opportunity to buy is rarely at the outset, from a risk-adjusted perspective, and the best time to sell is rarely before operations start.

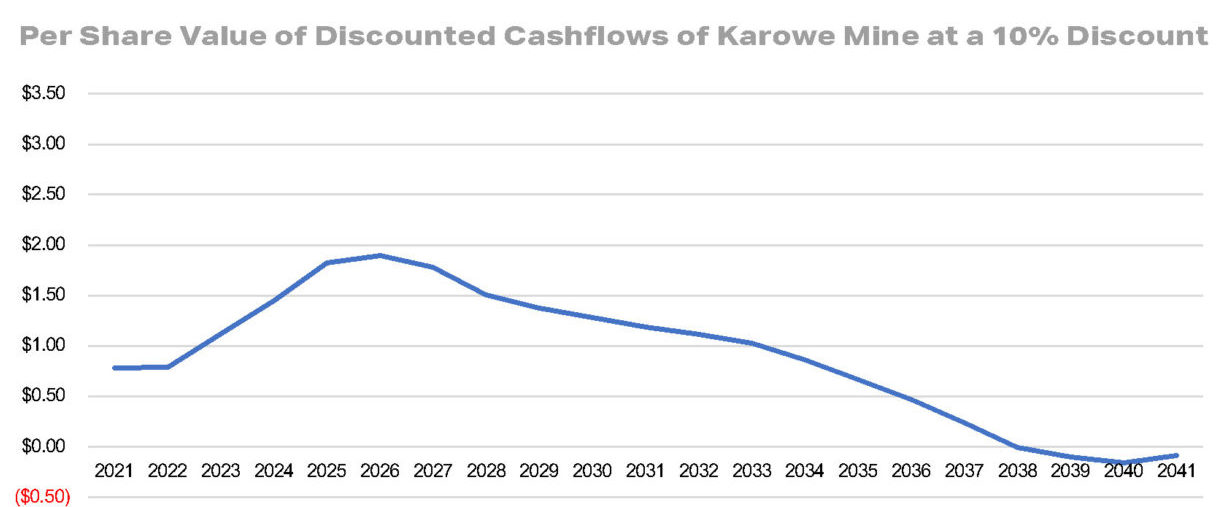

Lucara is a long-term holding which we have recently reduced in size, in part, because of these factors. Lucara owns the Karowe Diamond mine in Botswana. The mine currently has enough developed reserves to operate through the end of 2025 (roughly) and a plan to extend the mine’s life underground, adding approximately 10 to 15 years to the mine’s life at a cost of roughly $514 million. The firm’s peak fundamental value[7] is in 2026, the year in which major CapEx expenses for the underground mine are in the past, costs that reduced the firm’s FCF in the period between the present and 2026, reducing its per-share value and production growth is ahead of the firm.

The rough fundamental valuation on a per-share basis of the firm as we advance through time thus looks like this:

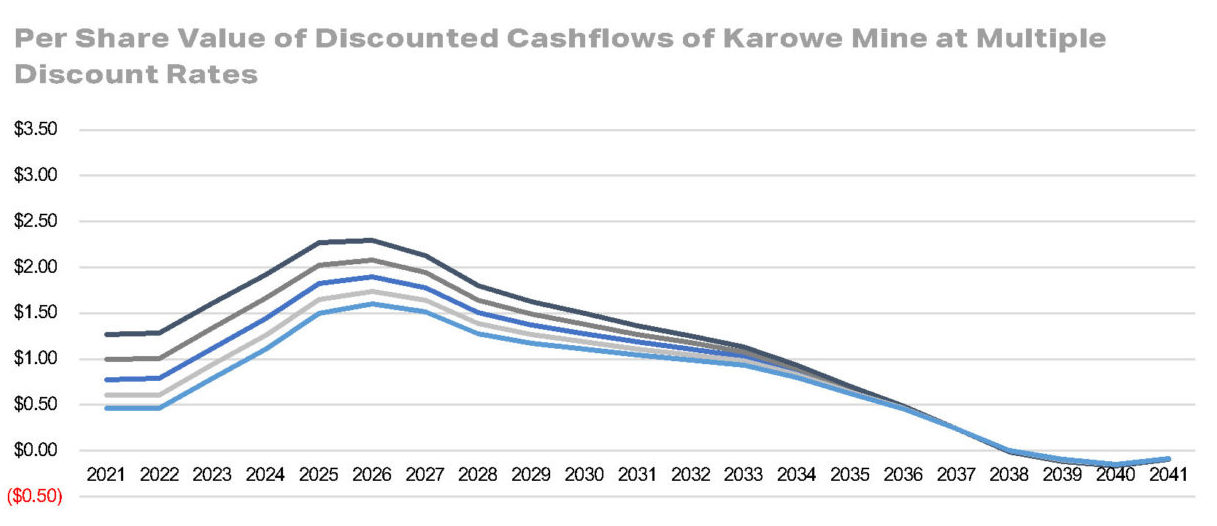

Many assumptions go into this chart, the most significant being production volumes, diamond pricing, financing structure, and discount rates (a risk estimate). The following chart shows how the value on a per-share basis changes with a varying discount rate assumptions:

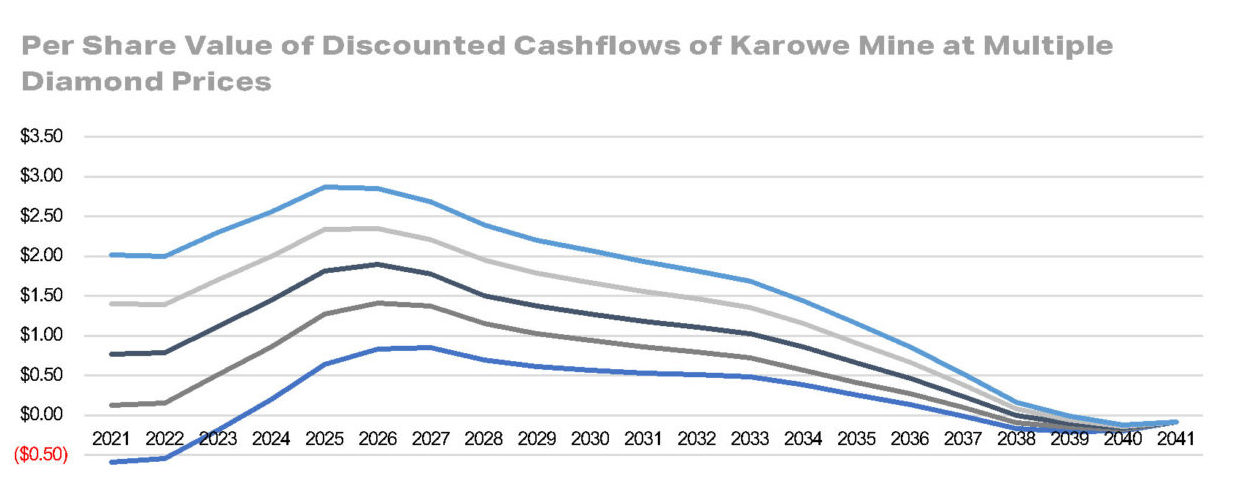

Varying financing structure assumptions (in essence, how much equity vs. how much debt is used in the financing of the build-out of the underground), or any of the other inputs, produces similar charts. For example, the following chart depicts the fundamental value at a 10% discount and multiple diamond prices:

The critical observation is that the shape of the fundamental valuation curve moves up and down along the Y-axis but does not change, which is to say the fundamental peak value is achieved in 2026, with assumptions defining the absolute peak but not the structure. After 2026, investors benefit only from a known set of fundamental shifts if they purchased the embedded value at a reasonable market price relative to the variables driving fundamental value or because of non-fundamental factors, perhaps market sentiment around the narrative of the company—for example, a story around a sudden growth in natural diamond demand by millennials.

From a portfolio management perspective, the critical takeaway is per share prices above the fundamental value-line post-2026 are increasingly driven by narrative, not project economics. In the run-up to 2026, though, there are non-commodity price catalysts that impact fundamental value. In short, buying real asset businesses well means buying them at the right time. Anything else is likely to be a purchase with narrative drivers but no fundamental corporate drivers. Furthermore, this creates a timeline for ownership. We know that if we buy the stock today, we have until 2026 to own it before experiencing a fundamentally driven deterioration in the underlying asset’s value. The timeline is essential for evaluating hurdle rates: assuming the market fails to recognize this asset’s fundamental value until 2026, do I meet my hurdle rate for inclusion in the portfolio. Do I have other opportunities that are superior?

We are enthusiastic and encouraged by the seismic undercurrents in the energy, industrial, and basic material landscape. Growth and innovation are desperately needed for these industries, and our base case is that it is coming. We encourage investors to have an open mind when valuing these businesses.

[1] Lev, Gu. “The End of Accounting”. Wiley Finance Series. 2016; Mauboussin, Callahan. “One Job”. Counterpoint Global Insights. Morgan Stanley. 2020. Damodaran. “The Dark Side of Valuation”. Pearson Education Inc., 2010.

[2] Seven Challenges for Energy Transformation, Rocky Mountain Institute, 2019

[3] Electric car charging infrastructure, green hydrogen, floating offshore wind, etc.

[4] Merton H. Miller and Franco Modigliani, “Dividend Policy, Growth, and the Valuation of Shares,” Journal of Business, Vol. 34, No. 4, October 1961, 411-433.

[5] Uncertainty can be viewed as either a risk or an opportunity. We elaborate on this in our LAC report referenced below, but it lends credence to the notion of employing option analysis to natural resource projects to quantify such optionality.

[6] For those interested in the details of our Lithium America Thesis, please see our recently released research report here

[7] The value derived solely from the firm’s fundamentals and strategy, with no attribution given for sentiment or variation attributable to macro-economic variables.

Opinions expressed herein by Massif Capital, LLC (Massif Capital) are not an investment recommendation and are not meant to be relied upon in investment decisions. Massif Capital’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is limited in scope, based on an incomplete set of information, and has limitations to its accuracy. Massif Capital recommends that potential and existing investors conduct thorough investment research of their own, including a detailed review of the companies’ regulatory filings, public statements, and competitors. Consulting a qualified investment adviser may be prudent. The information upon which this material is based and was obtained from sources believed to be reliable but has not been independently verified. Therefore, Massif Capital cannot guarantee its accuracy. Any opinions or estimates constitute Massif Capital’s best judgment as of the date of publication and are subject to change without notice. Massif Capital explicitly disclaims any liability that may arise from the use of this material; reliance upon information in this publication is at the sole discretion of the reader. Furthermore, under no circumstances is this publication an offer to sell or a solicitation to buy securities or services discussed herein.

About The Author: William Thomson

Will Thomson is currently a Managing Partner at Massif Capital, a value-oriented investor partnership focused on global opportunities in the small and mid cap space, with special attention given to industrial and commodity-related businesses. He has previous energy and mining related work experience in private equity, credit analysis, insurance and government policy. Massif Capital combines a fundamentals based approach to individual company assessment with in-depth capital cycle analysis to find compelling investment opportunities.

More posts by William Thomson