This article is authored by MOI Global instructor Rohit Chauhan. He is an instructor at Asian Investing Summit 2018, the fully online conference featuring more than thirty expert instructors from the MOI Global membership community.

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

This is a quote about gold from legendary investor Warren Buffett.

Gold has been called an unproductive asset and a barbaric relic. The reality is that gold produces no cash flows of its own and hence its price depends on what others are prepared to pay for it.

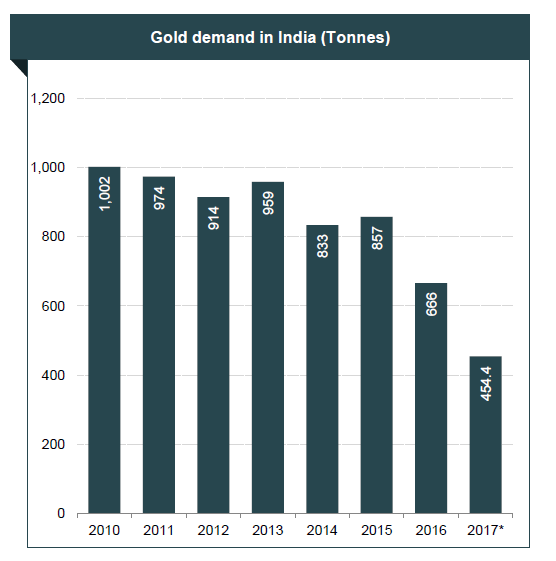

Indians Love Gold

While its commonly accepted that Gold is an un-Productive asset, in the Indian context, it’s different.

Irrespective of the views held about gold, Indians have always loved the yellow metal. Indians have been buying gold for a long time and this demand continues to grow irrespective of the price.

Source: IBEF, Gems and jewelry industry analysis.

By various estimates, Indians privately hold around 24000 tonnes or roughly 800 Bn dollars of the yellow metal (35-40% of GDP).

Although economists and policy makers consider gold as an unproductive asset, it is not an irrational purchase for the majority of buyers in India. Gold is seen as a store of value, especially in rural India where banking and other financial services are not available.

Gold also functions as an asset against which one can borrow in absence of access to a formal credit channel.

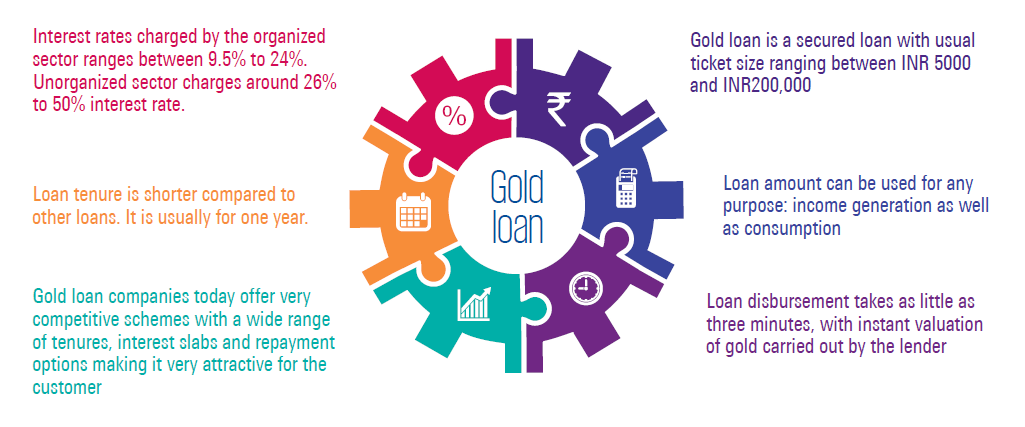

The Gold Loan industry

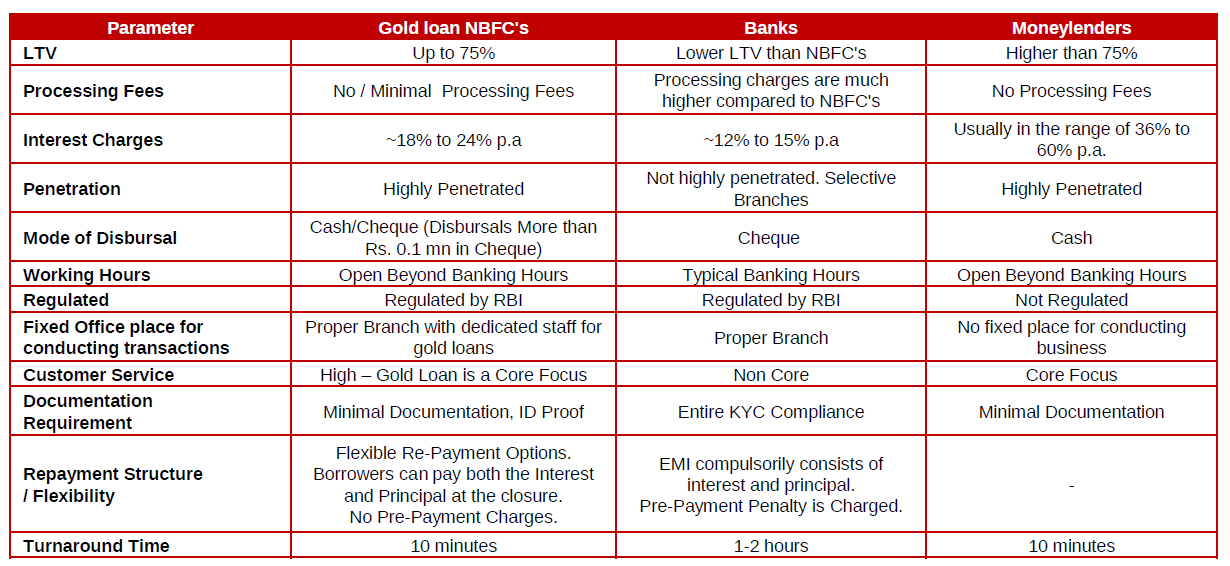

Let’s try to understand what a gold loan is – It’s a short-term credit extended to a borrower with gold serving as a collateral. This form of lending has developed in India due to the lack of credit data and verified personal details of the vast majority of the population. The following shows the features of this product.

Source: KPMG – India’s gold loan market: Is the glitter fading.

The Gold Loan Market can be divided in to a big unorganized market and a growing Organized one.

Unorganized Gold Loan Market

The gold buyer understands the value of this asset and its role in managing liquidity needs. The traditional method has been to pledge a portion of gold holdings to the local pawn broker for short periods of time ranging from 3 to 12 months.

The downside of using this channel is the high rate of interest in the region of 40-100% per annum. Inspite of the steep price, the local lender provides convenience, fast service and minimal documentation.

There are no precise estimates available for this market, but its size is in the order of billions of dollars.

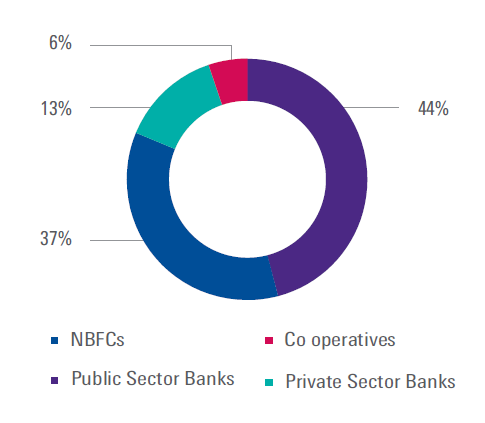

Organized Gold Loan Market

The organized sector is split between banks, non-deposit taking entities such as the NBFCs and cooperatives.

Share of organised gold loan market – 2016

Source: KPMG – India’s gold loan market: Is the glitter fading.

The organized sector has now started expanding in this space by increasing the number of customer touch points, providing high levels of service at lower interest rates and finally by providing security of the collateral backed by a known brand.

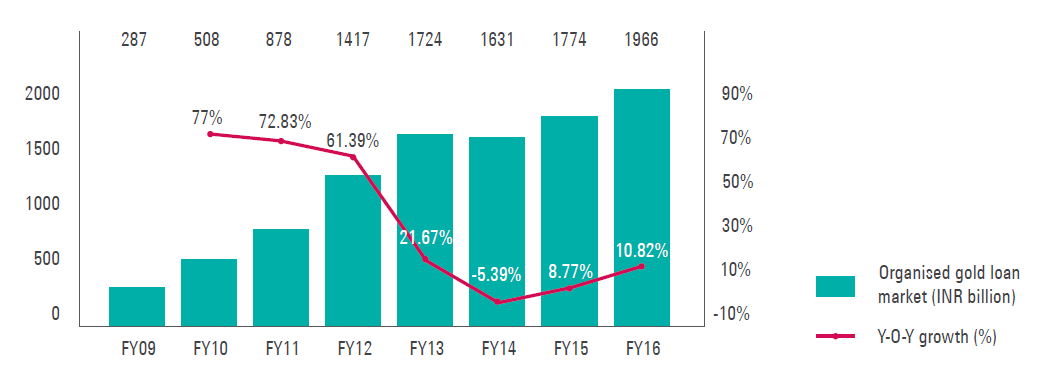

The Organized market is almost 25% of the total gold loan market and around 3-4% of the total gold holding. The organized segment continues to grow at 10%+ levels and has a long runway ahead of itself as it has barely scratched the surface.

Value of organised gold loan market in India

Source: KPMG – India’s gold loan market: Is the glitter fading.

Players in Gold Loan Industry: Advantage Gold Loan NBFCs

There are two gold loan focused NBFCs in this space – Muthoot finance and Manappuram finance.

The two companies have grown faster than the rest of organized sector due to higher focus on this segment leading to better product design and wider distribution. In order to understand the value proposition from the customer’s viewpoint, we can compare the unorganized sector with the banks and the NBFC.

Source: Manappuram finance Q3 2018 investor presentation.

Banks provide a low-cost product compared to the other channels but is limited in terms of their service levels and need a much higher level of documentation, which is often not available with the borrower.

The local money lenders provide a high level of convenience but charge a much higher rate of interest.

The gold loan NBFCs provide a product which can combine the cost advantage of the banks (to a certain degree) with high service levels and flexibility of the unorganized sector. Thus, these companies have been able to create a niche for themselves in the market by being focused players and developing products which fit the needs of the market much better than the other players.

Manappuram Finance: A history of profitable growth

Manappuram finance was started by the current MD & CEO – Mr. VP Nandakumar as a single store in the state of Kerala in India. The company expanded to around 70 stores in the first ten years of its operations.

The turning point came in the mid-2000s, when the company was able to raise around 5 Billion rupees from Temasek holdings, Singapore. With access to capital, the company has been growing rapidly in the last 12 years and now has a pan India presence with 3318 branches.

It has grown its loan book at a CAGR of around 38% over the last 11 years as shown below.

The company has maintained an average ROE of 20% during this period and has thus been quite profitable during this growth phase.

Source: Manappuram finance annual report.

The misperception around gold loans

Lending to low income borrowers at the bottom of the pyramid may appear to be risky, but the numbers show a very different reality. Manappuram finance has had an average NPA of less than 1% for the last 10 years in spite of all sorts of macro and regulatory shocks

The actual loss given default is even lower as the average LTV is 70% and due to the short tenure of the loans (less than a year with average being 3-6 months), the company is usually able to recover almost 100 cents on the dollar.

The gold loans business is thus quite profitable with interest spreads in the range of 13-15% and these companies have been able to earn 20%+ on equity with much lower leverage than other financial institutions.

What does not kill me, makes me strong

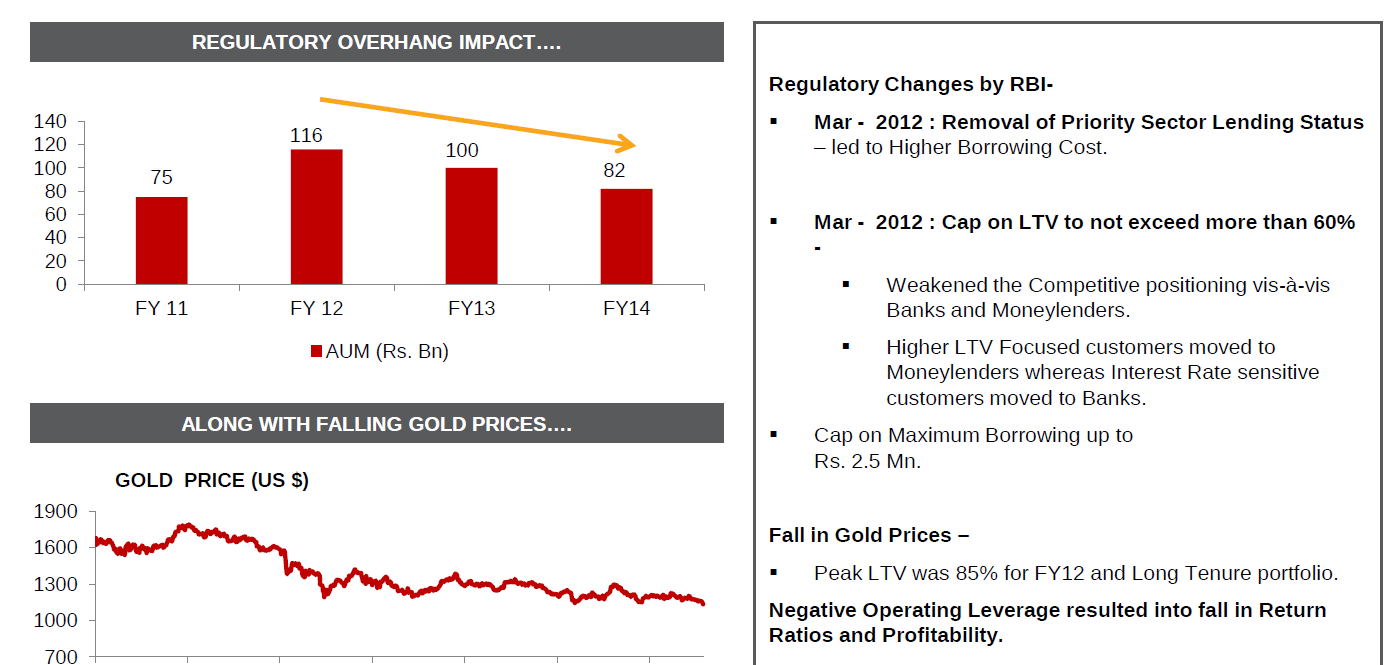

The journey for the company has not been a smooth un-interrupted one. The period from 2012 to 2014 stand outs for the de-growth in business and drop in profitability due to multiple shocks to the gold loan segment as shown below.

Source: Manappuram finance Q3 2018 investor presentation.

Inspite of the regulatory shocks and drop in gold prices, the company continued to be profitable during this period.

The management changed its operating model during this period by reducing the LTV ratios, dropping the tenure of the loans to 3-9 months and finally enhanced its marketing effort to reach more customers.

This resulted in normalization of the business till Nov 2016, when demonetization of high value currency caused a disruption in the SME sector which in turn accounts for a majority of borrowers for these companies. As a result, the gold loan growth was again impacted over the last one year.

In addition to the above macro events, the company was hit with several store level thefts in early 2017, which resulted in loss of the customer gold. Although the losses were insured, a repeat of such incidents could result in loss of trust in the long run.

The company increased the security at the branch level at the cost of 1600 Mn rupees or almost 20% of the profits. The management is now planning to migrate to technology led solutions and thus reduce this cost in the next 1-2 years.

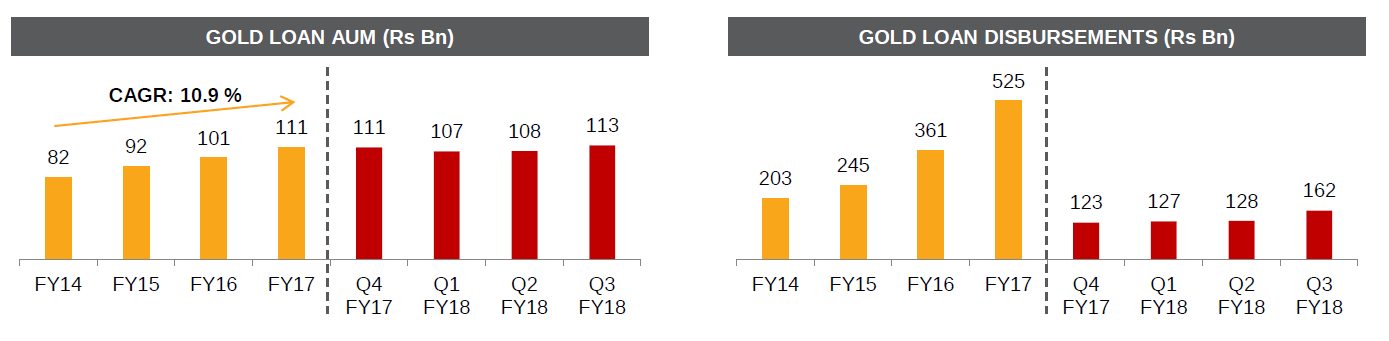

A return of growth

The shocks from the demonetization event have now dissipated and the borrowers are returning back as can be seen from the growth in disbursements in the recent quarters. The loan book has started growing and the company expects to grow the gold loan portion at low double digits.

Source: Manappuram finance Q3 2018 investor presentation.

At same time, Manappuram is no longer a single product – gold loan company, but slowly evolving into a multi-product firm to leverage its brand and distribution network.

It is now expanding into vehicle financing, housing finance and micro finance via its subsidiary -aashirvad finance. These products are targeted to the same customer segment as the gold loan business. This portion of the loan book is growing at 20%+ and is being targeted to reach 25% of the total loan book in the next 1-2 years.

If we combine the low double-digit growth of the gold loan book and 20%+ growth of the other products, it is easy to see the company growing its revenue line in excess of 15%+ for a long time.

The company has earned an ROE of 20%+ in the past and this is likely to continue, if not improve as the new products mature and reach scale.

Valuations

The macro shocks and misperceptions about the economics of the gold loan business means that the company has been mispriced relative to other financial services companies.

A combination of topline growth from new initiatives, normalization of macro conditions and finally reduction in security expenses means that the company should be able to double its profits in the next three years. A company growing at 20% + rate with an ROE of 20%, cannot continue to sell at 13 times earnings when comparable firms sell at 20 times or higher.

We can expect above average returns from the stock even if the company delivers sector level growth. We do not have to make any heroic assumptions in the case of manappuram finance to see a material upside.

About The Author: Rohit Chauhan

Rohit Chauhan is an Engineer / MBA with 20+ years of experience in different functions in large corporations in India and abroad. Rohit was introduced to the Investment world in the mid-90s when he started managing his family’s Finances. He learnt the basics by reading financial newspapers and books, and from his mistakes in the early days. Rohit’s approach towards investing changed when he came across the book ‘The Warren Buffett Way’. He got interested in Value Investing and started reading books from legendary investors like Benjamin Graham, Philip Fisher and other greats in this field. Their teachings have formed the bedrock of his investment philosophy. Over the years, Rohit has also learnt to apply the behavioural aspects of investing to his process. Rohit has followed the ‘Value Investing’ philosophy for the last 15+ years in managing his capital.

More posts by Rohit Chauhan