This article is authored by MOI Global instructor Ashish Kila, Director at Perfect Group, based in New Delhi, India.

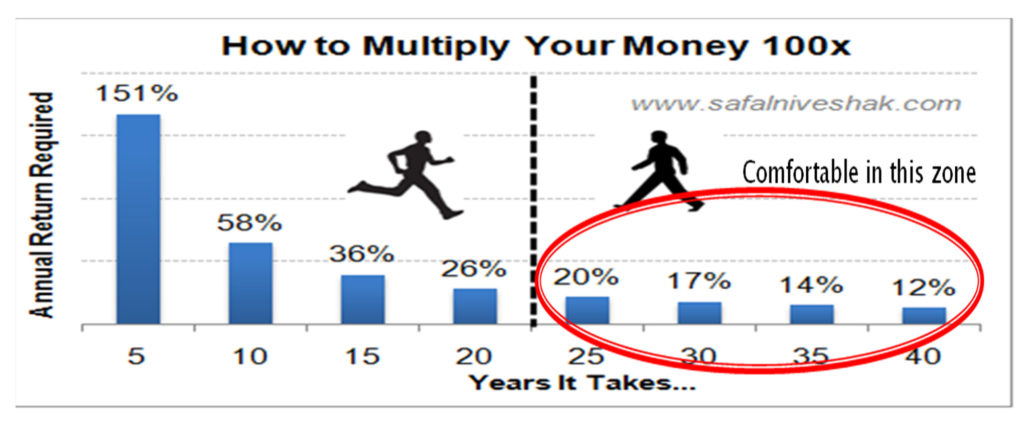

Over time we have shifted our focus to studying great businesses. There is less stress per unit of return and you don’t suffer reinvestment risk. There are other benefits like power of compounding, freedom to pursue other business, family and personal interests. Ultimately it all boils down to the hurdle rate. See the picture below – which basically says ‘why to run & fall in risk when you can walk your way to financial independence.’

Earlier we used to run screeners for cheapness (e.g. IFB Industries) and try to understand if the business is sound. But now we start with great business models (e.g. Info Edge (India) Ltd.) and look for reasonable returns in the long term. Margin of safety is more in quality than in price and mistakes tend to be more of opportunity cost rather than loss of capital.

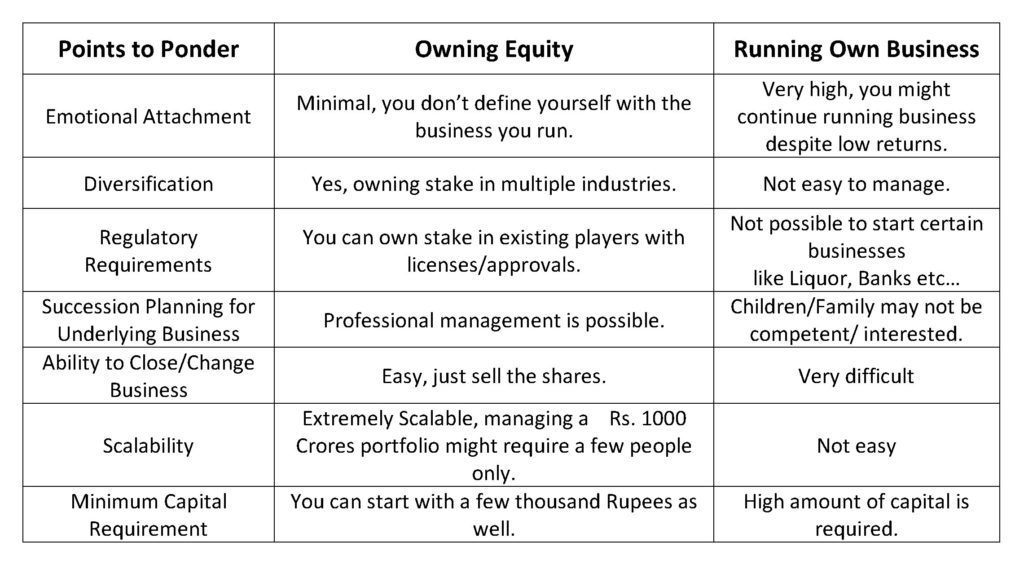

Owning Equity V/s Running Own Business

Our rationale behind the thought process is that owning equity is like owning a business where a hired CEO is working for us and will quarterly report to us by con-calls and/or investor presentations. Also owning equity has many benefits over running own business, which are described in the table here:

In owning equity, we get another benefit which is the potential to multiply the scarce resource of “Time”. As Tim Ferris says, “Be neither the boss nor employee, but the owner. To own the trains, and have someone else ensure they run on time.” Meaning owners of business are not limited by the amount of time they put in the business. The best doctor also can’t work for more than 15-16 hours a day. But in business we can multiply man hours by delegating, because here a hired CEO is working for us and we don’t need to manage business every day and night.

Why the need to think differently for valuing great stocks?

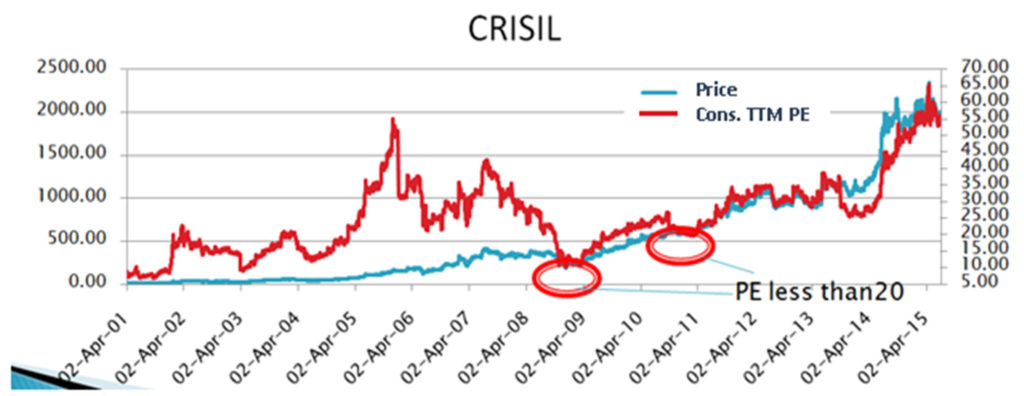

For expensive stocks valuations in the near term one can wait for some opportunities as temporary underperformance corrects the stock but when you wait there is a chance you might miss the stock. Look at CRISIL chart below, in last 10 yrs it gave 2 brief opportunities to accumulate below a trailing PE of <20.

To explain why standard valuation matrix is not the best measure to value such great businesses, we take some examples below:

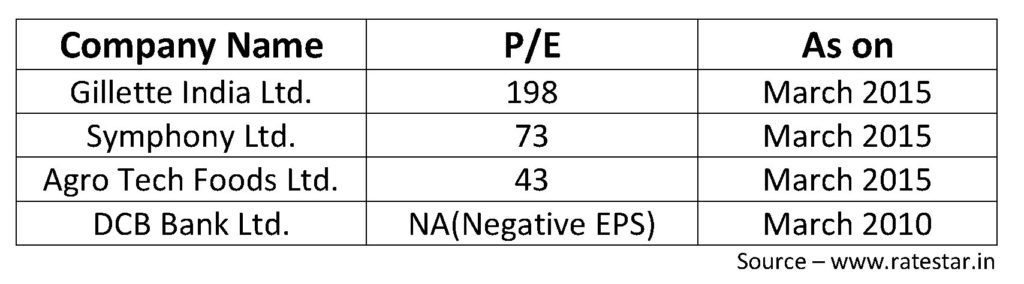

I. Use of P/E multiple: In the given example if we look at P/E multiple then we might not invest in any of the companies above because they all look so expensive and we might miss a great business like DCB Bank.

II. Not using P/E multiple: If we don’t look at P/E and we say that I buy all great businesses, then we might end up buying Gillette also which is extremely overvalued (will discuss more on it later).

Solution to such problems:

There are 3 aspects:

I. Moats: How durable and wide the moats are?

II. Size: Small size in relation to the addressable size.

III. Limited downside: When no earnings are there.

Let us discuss all of them below:

I. Durable Moats: It is important to judge the depth and longevity or durability of moat and if the moat shrinks and disappears, a buy and hold strategy will not save you. In a nutshell, can you visualize whether company’s product/services shall be in demand 10/20yrs down the line & can we think that despite competition, company has some competitive advantage vis-à-vis others to serve that demand?

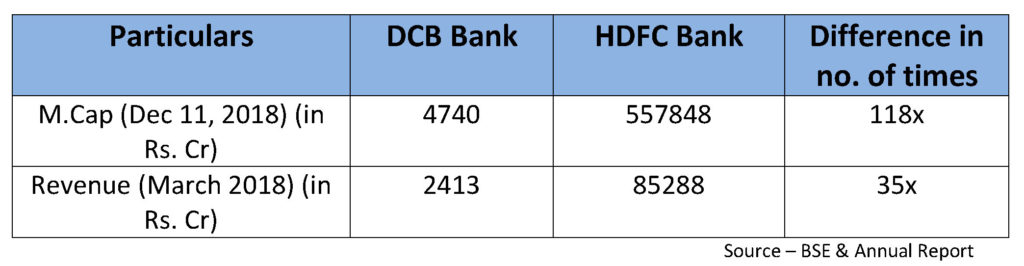

II. Size: Small size in relation to the addressable size: Let us take two examples here:-

A) – comparing two private banks; the leader in that space ‘HDFC Bank’ is less than 10% of total advances whereas ‘DCB Bank’ is not even a fraction of HDFC Bank.

HDFC bank a 100 times larger in size can grow its loan book at 20%, one can clearly see that DCB Bank has just scratched the surface in the Banking Industry and can continue doubling its Balance Sheet every 3-4 years for a long time.

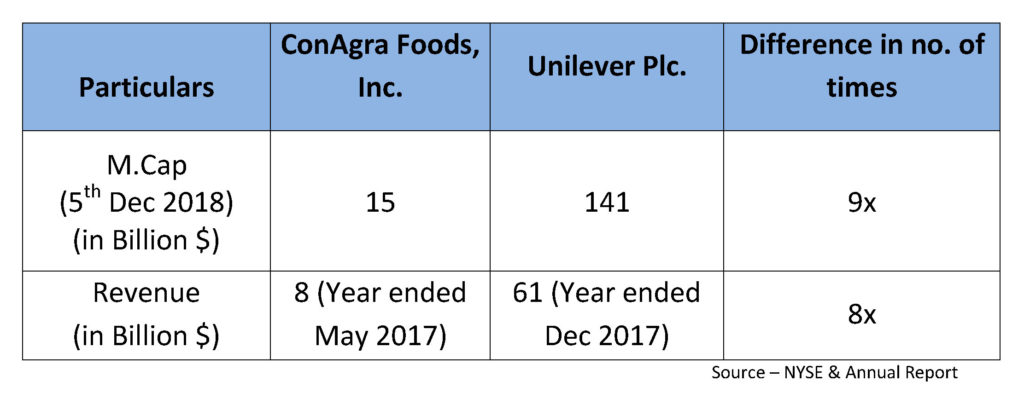

B) – Let us compare two multinational companies – ConAgra Foods Inc. and Unilever Plc.

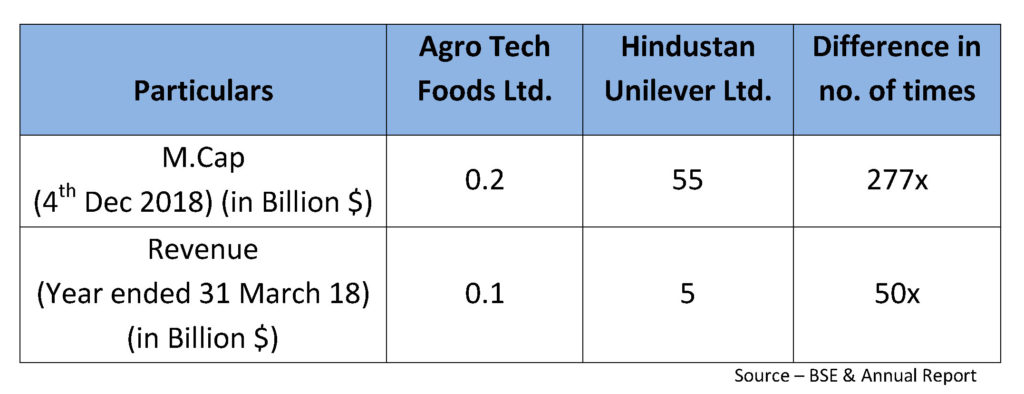

Now let’s compare their Indian Subsidiaries – AgroTech Foods and HUL, One can clearly see that AgroTech has just scratched the surface in India.

The difference in the size of their parents compared to the Indian subsidiaries is low and it shows the potential opportunity for AgroTech Foods in India.

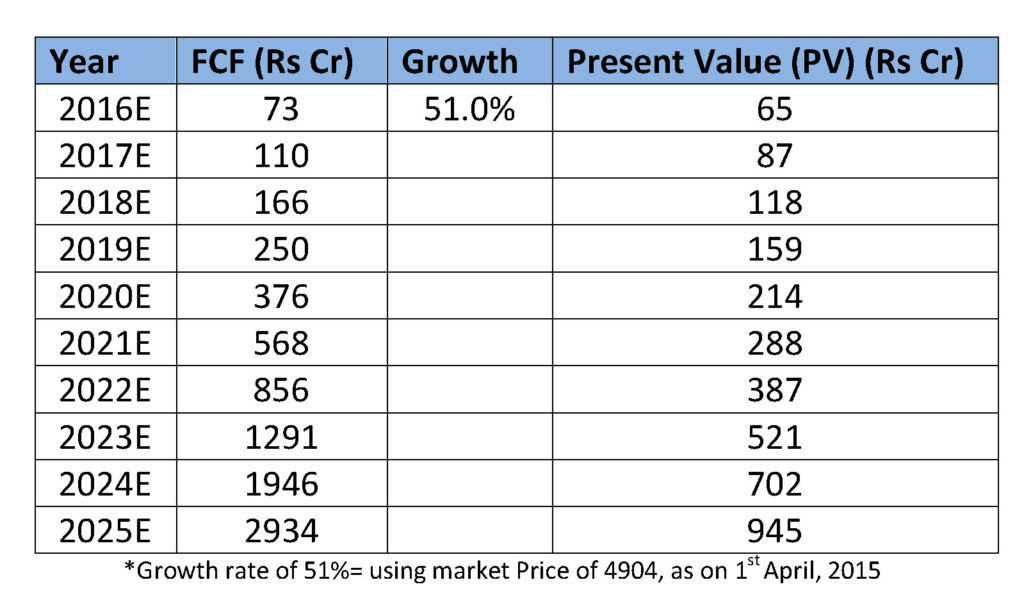

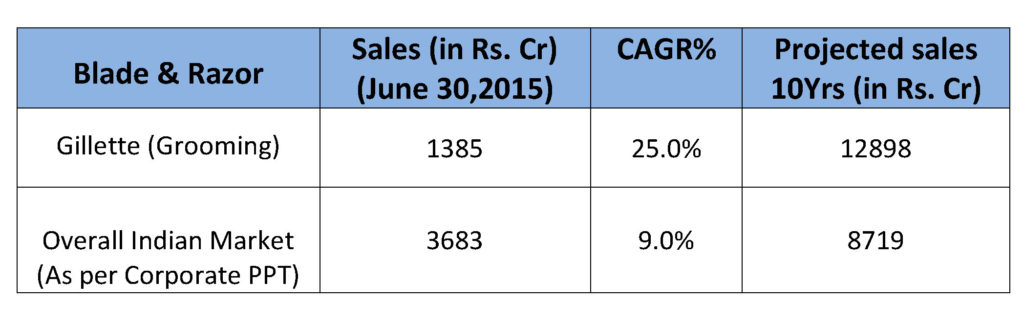

We take another example of Gillette and for simplicity sake we just focus on Blades and Shaving segment which accounts for all the profit of the company currently and add back the capex done in the oral care segment.

We then use Reverse DCF on it i.e. what is the growth rate in Free Cash Flow (FCF) implied by the market in the current valuation of the company.

Under reasonable assumptions of Terminal Growth Rate of 4% & Discount Rate of 12%, we get to know that implied growth rate of FCF for Gillette is about 51%. And if FCF of Gillette has to grow by 51% then its sales should grow by at least 25-30%. And if it grows by 25% what happens is given below in the table, Gillette becomes even bigger than market size, which is impossible. So this framework, kind of gives a ceiling to the valuations for a company.

In a nutshell, to summarize the framework for a great business we see:

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Disclaimer: We are not SEBI registered analysts. This is an educational post only and not a stock recommendation. Any stocks discussed in this letter are for illustrative purposes only. The content of this letter is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth in this letter. Perfect Group’s officers, directors, employees, principals and/or contributing authors may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated in this letter.

About The Author: Ashish Kila

Ashish Kila is a rank holder CA and MBA from MDI Gurgaon. He has worked with leading investment banks like Goldman Sachs & Morgan Stanley in their equity research division and now is the Director at Perfect Group. Ashish looks after the strategic functions at the group and manages the family office fund. Ashish regularly speaks at various business schools like MDI Gurgaon & investor forums like CFA Society India, Indian Investing Conclave, October Quest, Flame Investment Lab - Alumni Meets, TIA meet, NIRC (ICAI), IIF, etc.

More posts by Ashish Kila