This article is authored by MOI Global instructor Chris Colvin, founder and portfolio manager at Breach Inlet Capital, based in Dallas, Texas.

Chris is a featured instructor at Best Ideas 2021.

Are we in a stock market bubble? I think you first need to define the “market”. During the five years ended in October 2020, the price of the Large Cap Growth (“LCG”) index[1] more than doubled leading to a 16% annualized return. The same cannot be said for Small Cap Value (“SCV”). Its index[2] gained only 20% over this timeframe equating to a paltry 4% annualized return. Said differently, LCG outperformed SCV by 86% for the five years ended in October 2020.

While a LCG bull may point to the dominant market share and significant cash flow generated by the FAAMG, there are many examples where this is not the case. As I write this, DoorDash (NYSE: DASH) closed its first day of trading at ~$190 per share or more than double its initial IPO price range. The market is ascribing a value to DASH that exceeds Chipotle and Domino’s combined. DASH burned over $0.5b in cash last year, but…it has enormous growth potential. Investors’ obsession with growth has come at the expense (pardon the pun) of disregarding profitability. Given today’s investing environment, it is not surprising many market pundits believe value investing, especially SCV investing, is “dead”. Yet, I want to share a different perspective.

Despite the consensus chorus again echoing that “this time is different” and LCG’s outperformance is sustainable, I choose to side with Howard Marks. He reminds us: “Investment markets follow a pendulum-like swing: between euphoria and depression, between celebrating positive developments and obsessing over negatives, and thus between overpriced and underpriced.” The sentiment pendulum also swings across subsets of the equity markets, such as from LCG to SCV. Was November evidence of the pendulum swinging toward SCV?

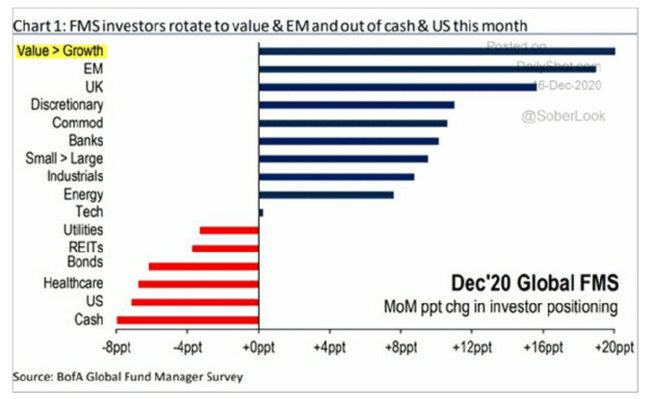

Last month, SCV gained 19% while LCG rose only 10%. This trend continues in December. Though not specific to small caps, inflows into value ETFs also recently outpaced inflows into growth ETFs by the widest margin ever[3]. As more evidence, fund managers have been rotating from growth to value stocks according to the BofA Global Fund Manager Survey in December[4]. Two months cannot be called a sustainable trend, but history provides a useful guide.

During the last five years of the tech bubble (Mar-95 to Mar-00), SCV underperformed LCG by 219%. Similar to today, prognosticators claimed SCV investing was “dead”. During the five years following the tech bubble bursting (Mar-00 to Mar-05), SCV beat LCG by 139%. More importantly, SCV outperformed LCG by 116% over that full decade (Mar-95 to Mar-05) highlighting that valuations matter and patience can be rewarded.

Even if SCV’s recent outperformance proves temporary, I believe SCV will continue to provide fertile grounds for a Long/Short strategy. Many investors associate SCV with broken business models and stretched balance sheets. This is partially true and leads to compelling candidates for Short positions. On the flip side, the SCV market also includes industry leaders that dominate niche markets and have long runways to grow. These are the types of companies we target for Long positions. For instance, Rent-A-Center (NASDAQ: RCII) is a member of the SCV index (RUJ). It is a market leader, quadrupled EBITDA in the past three years, and expects to sustain rapid growth through e-commerce & its FinTech platform (Preferred Lease). From February 2017 to October 2020, RCII gained over 250% despite the SCV index (RUJ) falling 2% over that timeframe. Hence, RCII highlights that you can identify rewarding SCV investments even when SCV is broadly “out of favor”.

A small cap strategy benefits from the ability to repeatedly exploit a persistent dynamic. Relative to large caps, I believe small caps is a less efficient market because there are far more companies covered by far fewer sellside and buyside analysts. Also, I think small caps can be more efficiently researched because they are often simpler businesses and provide greater access to senior management. This access is also more critical and meaningful at smaller companies where executives’ decisions are often more impactful to value-creation than decisions by executives at large, multi-national conglomerates. In sum, a less efficient market coupled with more efficient research results in small caps being a compelling opportunity set.

Going a step further within small caps, I think focusing on “value” is more attractive than “growth”. The primary reason is that many “growth” small caps have limited visibility to generating earnings, which ultimately drives value. Meanwhile, a SCV investor can aim to own companies that are growing earnings and thus, increasing intrinsic value. That is our focus for Long positions. Revenue growth without a tangible pathway to profitability is a recipe for disaster. Furthermore, “growth” companies are typically priced at high revenue multiples. A “growth” company’s share price may have far to fall if growth expectations are not met and there is not an earnings yield to provide support.

To conclude, I believe “you can have your cake and eat it too” by investing in companies that are sustainably growing profits yet are trading at “value” multiples (i.e., low price-to-earnings). Given the information inefficiencies in small caps, a SCV investor can repeatedly identify such opportunities. I think the prospects for SCV have never been more attractive. If history is any indication, SCV is positioned to materially outperform in the coming years. While we are confident in our ability to compound capital in any market, we would certainly welcome better sentiment towards SCV.

[1] Large Cap Growth (“LCG”) Index = S&P 500 Growth Total Return

[2] Small Cap Value (“SCV”) Index = Russell 2000 Value Total Return

[3]

[4]

Disclosure: Any investments discussed in this letter are for illustrative purposes only and there is no assurance that Breach Inlet Capital will make any investments with the same or similar characteristics as any investments presented. The investments are presented for discussion purposes only and are not a reliable indicator of the performance or investment profile of any client account. Further, you should not assume that any investments identified were or will be profitable or that any investment recommendations or that investment decisions we make in the future will be profitable. There is no guarantee that any investment will achieve its objectives, generate positive returns, or avoid losses. THE INFORMATION IN THIS LETTER IS NOT AN OFFER TO SELL OR SOLICITATION OF AN OFFER TO BUY AN INTEREST IN ANY INVESTMENT FUND OR FOR THE PROVISION OF ANY INVESTMENT MANAGEMENT OR ADVISORY SERVICES. ANY SUCH OFFER OR SOLICITATION WILL BE MADE ONLY BY MEANS OF A CONFIDENTIAL PRIVATE OFFERING MEMORANDUM RELATING TO A PARTICULAR FUND OR INVESTMENT MANAGEMENT CONTRACT AND ONLY IN THOSE JURISDICTIONS WHERE PERMITTED BY LAW.

About The Author: Chris Colvin

Chris Colvin, founder and portfolio manager at Breach Inlet Capital is an investment manager who runs a concentrated portfolio of small caps undergoing transformations.

More posts by Chris Colvin