This post is authored by MOI Global instructor Sam Sheldon, research analyst at Punch & Associates Investment Management, based in Saint Paul, Minnesota.

Sam is an instructor at Best Ideas 2022.

Great investors seek out businesses with strong and sustainable competitive advantages, giving these companies the opportunity for sustained success without too much competition. The challenge is that many investors are looking to own these types of businesses, and when priced for perfection, these shares may offer little value. A simple screen will uncover some of the widest-moat companies in the market: however, these often are companies with the richest valuations. Perhaps “wide moat plus easy-to-fi nd” is not the best formula for identifying opportunities across the market cap spectrum.

Beware of Buying Great Companies

To be successful for our clients, we fi nd what we believe are great businesses and hold them long enough for others to arrive at the same conclusion. We generally hold companies for three to five years. Also, to minimize risk, we should be reluctant to overpay.

Many investors construct portfolios using companies identified through quantitative screens with limited consideration of any qualitative factors. Anyone can run a screen, and this overly simplistic approach is perhaps the reason for the proliferation of the ETF. By contrast, it is more difficult to identify the companies that these screens might miss. An example of a company a screen may overlook is one that allows a mature legacy product to run off while seeding a dynamic growing business. The only way to determine whether to invest in a business or not is to develop a deeper understanding of the business and its prospects.

When we think we have found a compelling investment at a discount, we are repeatedly asking ourselves questions like, “What am I missing?” (Or, alternatively, “What am I getting away with?”) The best way to fi nd answers is to talk to management and research the company’s competitors. Many investors don’t bother to take this qualitative step, and quantitative screens only go so far. Our goal is to have other investors gravitate toward our idea overtime as our company gains recognition, because a permanently undiscovered company is of no value to our clients.

Usually, there is a clear reason for finding a company so cheaply priced. Have we considered all the reasons? How temporary or permanent are the reasons? Of course, investors will never have perfect information; part of an investor’s job is to make an assessment with imperfect information. But, to skew the odds in our favor, we look in areas where we know there are structural reasons that result in mispriced, higher-quality businesses.

Small companies and forced selling situations are fertile hunting grounds. Index kick-outs, company spin-offs, taxloss harvesting, and companies emerging from bankruptcy are also examples where owners’ reasons for selling are not tied to the underlying fundamentals of a business. Finally, companies in transition and those recovering from a failed initial public offering can present steep discounts to their intrinsic value.

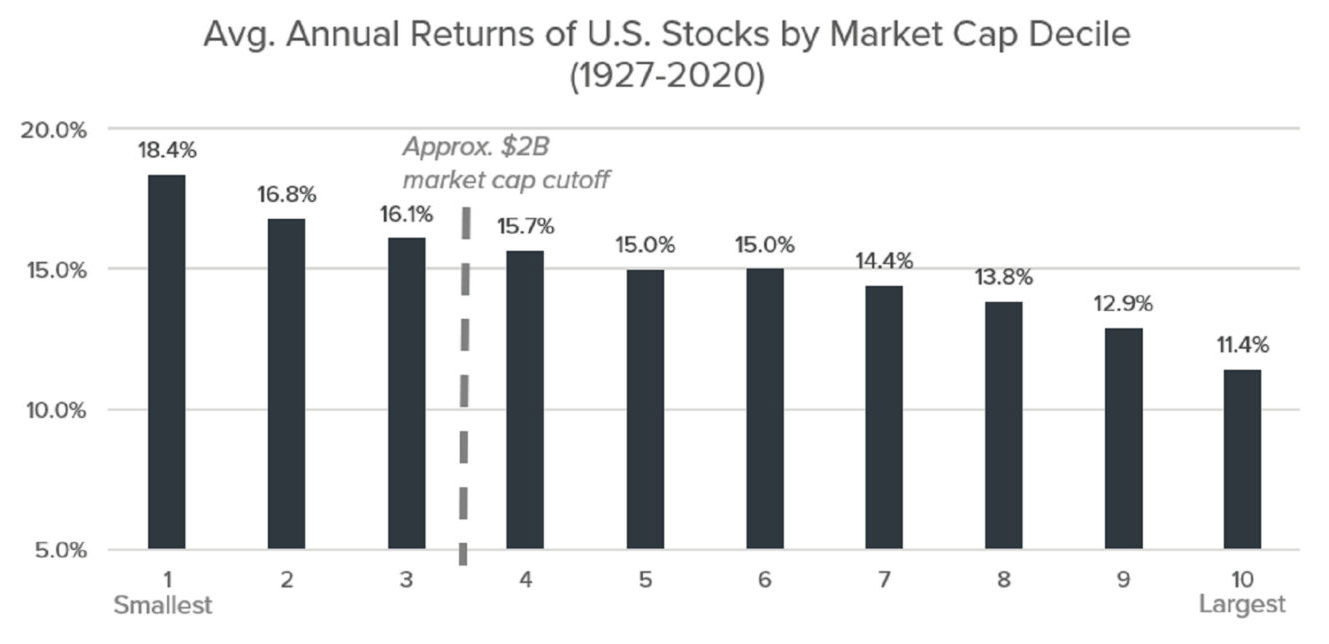

Smaller Small Caps

Small cap companies – and, more specifically, the smallest small caps – can offer compelling opportunities that few investors are willing to research because of liquidity concerns and a lack of information about the company. Investors willing to do the hard work of reviewing SEC fi lings, talking to management and competitors, and methodically building a position can uncover many great businesses in this market cap range. With less capital targeting this segment of the market, stocks are less efficiently priced, and often opportunities are more plentiful. On the other hand, an investor needs to be more patient and willing to tolerate a higher level of volatility. The data below confirms our belief that smaller companies, in the aggregate, outperform over time.

Source: Kenneth French Library, value weighted returns from 1927-2020.

Source: Kenneth French Library, value weighted returns from 1927-2020.

Kick-Outs

Every June, the Russell 2000 Index reviews its holdings and will drop or add approximately 100 to 200 stocks. Companies usually fi nd themselves on the kick-out list after, for example, a decrease in their market cap. This decrease could either be due to challenges the company is experiencing in its business or something like a stock buyback (which reduces the outstanding share count and, therefore, the market capitalization of the company) or some other shareholder-friendly action. Dropped securities come under selling pressure from passive funds and active managers who may be restricted from owning companies that are not in the index. Opportunity arises from substantial selling pressure that is not directly tied to the underlying fundamentals of these businesses (which may not be deteriorating as much as the falling share price would suggest).

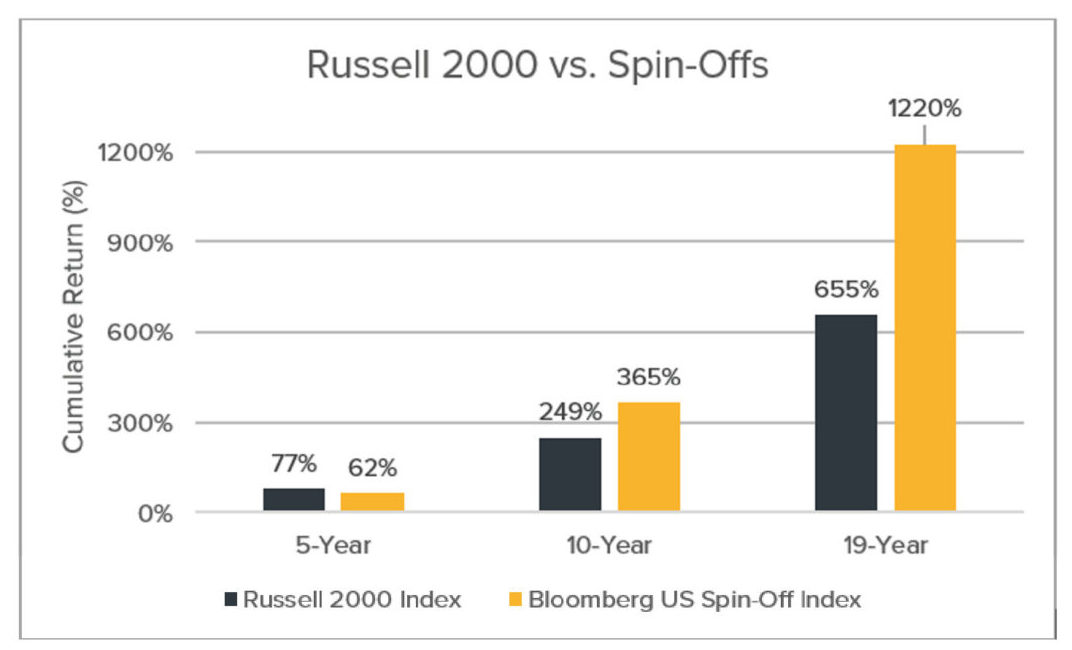

Spin-Offs

A spin-off occurs when a parent company determines that a subsidiary is better off as an independent entity and distributes the business unit to current shareholders. The new company may be so small that its new shareholders might sell it indiscriminately. This selling could be due to constraints of time, capital, or the number of positions allowed in a portfolio. Portfolio managers might also sell the new shares because they do not align with the manager’s objectives. The new company might have attractive characteristics which previously went unrecognized because it was part of a larger organization. As a standalone company, the newly created entity has the freedom to focus on its core business.

Source: Bloomberg data. Cumulative returns as of December 27, 2021.

Source: Bloomberg data. Cumulative returns as of December 27, 2021.

Investors end up dismissing businesses with great potential without much thought, and some businesses trade at illogical valuations temporarily. In addition, the opportunity can remain undiscovered for an extended period, as spin-off s typically don’t “screen” well. Also, the financial information for the company is not always easy to find and therefore not accurately entered into financial databases. While the effect of spin-off s is well-documented, they continue to outperform the market in general as shown above.

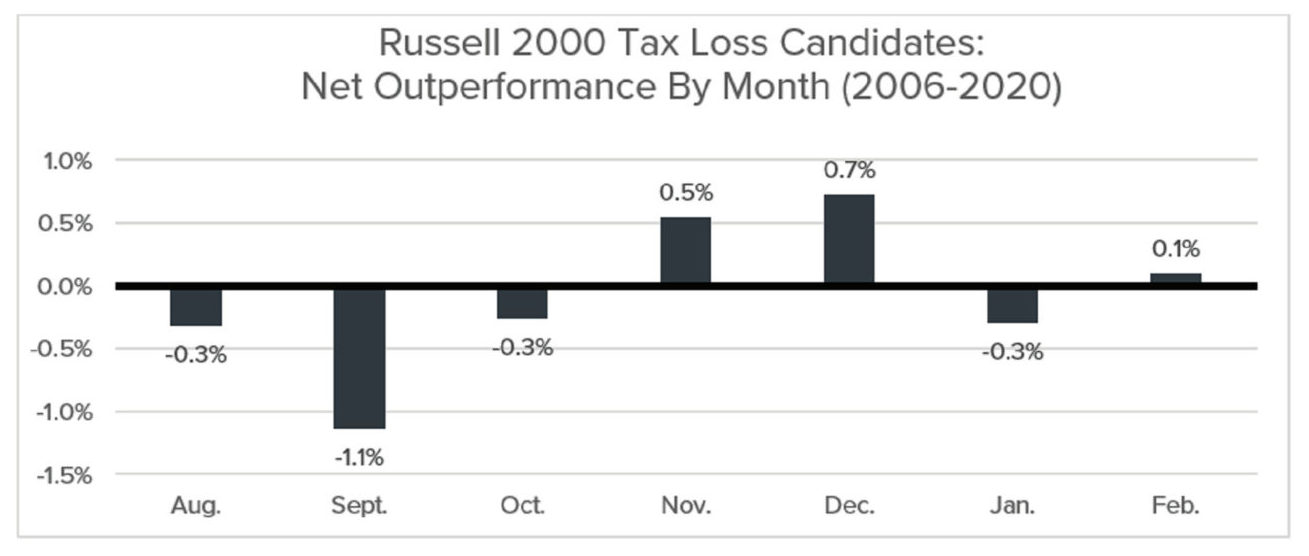

Tax-Loss Harvesting

A common practice among certain investors is tax-loss harvesting. This is the practice of selling a security that fell in value since the initial purchase, waiting the necessary time to avoid tripping IRS “wash sale” rules, and then repurchasing the same securities at a later date. The goal for investors is to realize the losses in a portfolio to help off set any gains. During the last few months of the calendar year this practice can accelerate, as investors naturally start to think about their tax liability. This practice meaningfully impacts small cap stock prices, and opportunities can arise from selling pressure not tied to the underlying fundamentals.

Source: Bloomberg data and Punch & Associates.

Phoenixes

Companies emerging from the ashes of bankruptcy usually have new shareholders that once were creditors. Given that many managers of credit strategies have a mandate to only hold debt in their portfolios, they have an eagerness to sell out of the equity as soon as practical. It is worth noting that some companies go into bankruptcy because of a capital structure issue and not a permanent impairment of the underlying business. Post-bankruptcy, balance sheets are usually much improved, and selling by unwilling equity holders can temporarily depress the valuation of a solid business with a much-improved capital structure. The new cost structure is usually not easily discovered by a simple screen and can take several months before the improvements are readily apparent.

Broken Deals

What behavioral finance refers to as “anchoring” also creates a pocket of investment opportunity. When a company sells shares to investors in an offering, the price at which the transaction occurs can stick in the minds of both parties. If a share price falls below the initial public offering price, post-offering it becomes known as a “broken deal.” Often, broken deals can be caused by miscommunication during the deal’s marketing process or inexperienced public executives’ faux pas on early earnings calls as a public company and not a deterioration of the business fundamentals. Rather than patiently own an immature company that may be going through some growing pains, many investors will decide that the initial buy thesis was “wrong” and arbitrarily sell the position rather than risk further losses.

Metamorphosing Enterprises

Businesses in transition may also create an investment opportunity. Many companies that have mature legacy products or services provide the cash for another part of the business that is growing. Because these mature product lines are shrinking, the company likely won’t “screen” well during the transition. Revenue growth may not reach expectations, resulting in some investment managers avoiding the company in search of faster-growing companies. Profitability may look compressed as the company is feeding its undiscovered growth engine, sometimes resulting in value managers avoiding the investment. If the pivot is a success, the tangential business can become a meaningful contributor to overall profits, and the market may eventually reward this effort. We recognize that there is a risk to investing in businesses in transition and, instead of value, we may find “value traps.” However, the only way to know if the pivot is likely to be a success is to fully understand the transition inside the company, which often requires old fashioned boots on the ground research of meeting with management teams, touring facilities and speaking with competitors. These qualitative insights cannot be found on a screen.

Conclusion

Active investing is difficult work, and there is no guarantee of success. If you screen for perfection, you may overpay for an investment, which is why investors should be suspicious of the “obvious” opportunities. Looking in underresearched or overlooked areas of the market can increase the probability of identifying a great business with a suboptimal valuation but identifying where to look is only step one of the process. Our job is to find companies where mispricing might be temporary, and we gain confidence when we fi nd companies with positive characteristics which are not currently reflected in financial databases. Most importantly, we must make a judgement call as to whether the company might someday exhibit the same characteristics as others with which we’ve enjoyed success in the past (healthier balance sheets, simplified business models, better predictability, more transparency, and, ultimately, greater recognition from a broader audience). If a company becomes better recognized by other investors, it can turn into an attractive investment for our clients.

About The Author: Sam Sheldon

Sam Sheldon joined Punch & Associates as an intern in June of 2016, while attending the University of St. Thomas where he also lead the University’s Investment Club. After graduating in May of 2018 with a BA in Financial Management, he joined the team full-time as an investment research analyst. In his free time, Sam enjoys boating on White Bear Lake, cheering for the Green Bay Packers and playing an occasional round of golf.

More posts by Sam Sheldon