Allan Mecham is probably one of my favorite investors to follow… Arlington Value has compounded at some 30ish% – here's his annual letters from 08, 11, 12, 13, 14, 16, and 17

Happy reading! https://t.co/1CRV95feSy pic.twitter.com/8CjnjRKvTf

— Andrew M. Kuhn (@FocusedCompound) September 21, 2018

This article is authored by MOI Global instructor Nils Herzing. Nils is an investment professional at Active Ownership Capital, a partner-managed investment company that acquires significant minority stakes in publicly listed, undervalued small- and mid-size companies in German-speaking countries and the Nordics.

This Investment Philosophy frames the general thinking about investing and describes my investment style. It is not a fixed set of rules, it is more an evolving collection of thinking patterns.

The aim of my investing is to generate long-term outperformance (over a time period of more than 5 years). Thus I don’t aim or a low volatility or other fancy things; the sole goal is to maximize the performance in real money terms.

I don’t believe in efficient markets, as I think that markets are “Voting Machines” in the short-term but “Weighing Machines” in the long term. I believe that the highest irrationality in stock prices, especially in the short run, exists in small- and mid-capitalized enterprises which have a low free float. Furthermore, I believe that an undervaluation in the long run can occur in large-caps, as most investors only think within a timeframe of 3 years. By taking a long-term investment approach which exceeds 3 years and thinking in time frames of 5, 10, or even 20 years, you are able to outperform the market even in large-caps.

I don’t believe in over-diversification, or in holding more than 20 stocks as it doesn’t add value and destroys performance. On the opposite, I believe that it is possible to get an investment edge via the two following ways:

a.) Informational edge – More information than every normal market participant has. This means doing field research, visiting companies and speaking with customers and competitors.

b.) Behavioral edge or “longer time horizon” – by taking a time horizon of more than 3 years, investors can see the value of long-term growth and are able to go against short-term pressure / noise / “pain”.

To participate from short-term irrationalities, it is necessary to have an investment process which is focused on the long-term value creation of a company, thus the value of growth is essential for my investing approach. To pursue this type of investment strategy, it is necessary to find long-term capital and co-investors who think like owners.

The only possibility to increase my returns towards a level of above 15%, which I would like to achieve in the long-run, is in my opinion:

a.) Have a less diversified portfolio of only 8 to 15 companies.

b.) Avoid a permanent loss of capital, which can be achieved by using quality filters such as good management, strong balance sheets and the use of “Owner Earnings”.

c.) Use a higher discount rate and thus have fewer potential investment candidates.

d.) Shorten the time frame of value realization, e.g., until the undervaluation is uncovered and the market price reaches the fair valuation of a business

e.) Take a long-term view of more than 5 years and invest in real compounders, which have an outstanding management / capital allocator, really early in their life.

Last but not least, I would like to achieve this goal by investing in an ethical and sustainable manner. I believe so, as I think that sustainability and ethical thinking is equal to a rational view on the long-term time axis.

How Ingraining Books into Research Leads to Non-Consensus Views

September 21, 2018 in Diary, Equities, IdeasThis article is authored by MOI Global instructor Adam Crocker, Chief Investment Officer of Logbook Investments, based in New York.

I look forward to presenting at European Investing Summit 2018, hosted by MOI Global. In order to frame the discussion, it may be useful to describe Logbook’s investing philosophy and how ingraining books into a research process leads us to different approaches of studying businesses and developing non-consensus views on key issues.

What is Logbook Investments?

Logbook is a fund that gleans insights on core positions from books. What does this mean? We believe that there is a vast pool of knowledge generally untapped by the investor community that can be unearthed by reading the work of literary experts. In a practical sense, once we find an investment idea meriting deeper research, we look for books that may augment our understanding beyond company filings, analyst reports, primary research, transcripts, et cetera. The types of books sourced could include:

• Biography of company founder or senior executive

• History of company

• History of industry

• Behavioral writings that are relevant to investment situation

• Seemingly unrelated book that “rhymes” with situation at hand

In my experience, insights from these non-Wall Street sources often provide perspective that other investors may overlook. It is also useful to learn from a source that has no interest in selling you anything, and often minimal awareness of the business as an investment. The information extracted from books is often more unbiased and unfiltered.

This process also requires a certain discipline, because not every book provides a profound insight. Just because we have devoted the time to read a book about a subject does not mean it merits a position in the fund—being willing to pass after a sinking time into deeper research is an important part of the process. However, when insights appear, they are often very clear and provide a strong basis for differentiated opinion. A brief sampling of books that have informed past Logbook decisions include:

The insights gleaned from books underpin our investment writeup that incorporates valuation, competitive dynamics, unique company attributes and so forth. At our last presentation to the Manual of Ideas in January 2017, Logbook cited Mondo Agnelli, referencing the parallels in business model and management style between the leaders of Fiat Chrysler and Peugeot. As an example of how the lessons from books can be evergreen, that research informed certain aspects of our upcoming presentation. This Manual of Ideas talk will provide further examples of the added dimensions books can provide to an investment thesis.

Why are investment writeups important?

The name Logbook refers to a pilot’s logbook, which must be completed every time before operating an aircraft. We believe the same checklist-based rigor should apply to investing. At Logbook, our checklist takes the form of an investment writeup, whose components have been assembled over many years. A sampling of the questions we ask ourselves include:

• Would anyone care if this company didn’t exist?

• What is the nature of its competitive advantage?

• What are key risks? Likely culprits if we have made a mistake?

• How has capital been allocated in the past?

• Any notable changes to risk factors or management incentives?

• What is our estimate of valuation, and how do current multiples compare to history?

These questions are the basis for a roughly fifteen-page report that serves as the template for our investment. More importantly, throughout the course of owning a business, this document is the primary reference point to compare unfolding events versus our initial expectations. It is much harder to delude oneself when reading your own words from a past writeup.

When share prices move up or down based on events not contemplated in our writeup, we are much more likely to move on from a position, booking a gain or loss. However, if results have been consistent with our initial probability distribution, it is likely that Logbook will remain invested in the particular situation. We can be much more confident in our original analysis when we predicted the possibility of unfolding events, instead of justifying surprises as they appear as “reflected in valuation.”

Book summary document

As a supplement to Logbook’s direct investing process, we try to read broadly to improve overall thinking, and also because it makes life more interesting. Beginning over a decade ago, I began compiling a document that is basically a “greatest hits” of books read in recent years. As Steven Johnson notes in Where Good Ideas Come From,

The great minds of the period—Milton, Bacon, Locke—were zealous believers in the memory-enhancing powers of the commonplace book. In its most customary form, “commonplacing,” as it was called, involved transcribing interesting or inspirational passages from one’s reading, assembling a personalized encyclopedia of quotations.

While reading a book, I write and underline a lot, and every couple years go back and type up the underlined parts worth remembering. This document serves as a wonderful refresher about favorite books, useful themes and pitfalls to avoid. It safeguards vital knowledge from fading too far into memory to be useful. As noted in The Atlantic,

The key thing was to write the words in your own hand—by this means, by laboriously and carefully copying out the insights of people smarter than you, you could absorb and internalize their wisdom. Call it osmosis-by-handwriting. Commonplace Books: The Tumblrs of an earlier Era; 1/23/12

Over time, by continuing to learn from the wisdom of great minds, Logbook aims to develop investment insights that benefit our partners.

NOTA DEL EDITOR: Estas ideas de inversión son obtenidas de una carta trimestral de Horos Asset Management.

* * *

La cartera cuenta con 33 valores y con cuatro temáticas que aglutinan el grueso de la misma. La principal está compuesta por compañías vinculadas a las materias primas (23%), especialmente acero inoxidable, petróleo y uranio. Otro bloque importante es el que engloba a valores emergentes olvidados (20%) o poco seguidos por la comunidad inversora, fundamentalmente de Asia. La inversión en plataformas tecnológicas (13%) con poderoso efecto de red que aún cotizan a precios muy atractivos para invertir y en compañías del Reino Unido (11%), impactadas por el brexit, serían las otras dos temáticas importantes de inversión.

Por último, la liquidez de la cartera a cierre de trimestre se sitúa en el 14%., aunque esperamos ir reduciéndola paulatinamente las próximas semanas hasta dejarla por debajo del 10%.

Continue reading »

This article by MOI Global instructor John Lewis is excerpted from a letter of Osmium Partners, based in Greenbrae, California.

Rosetta Stone Inc.[1], together with its subsidiaries, provides technology-based learning products in the United States and internationally. It operates through three segments, Enterprise & Education, Literacy and Consumer. The company develops, markets, and supports a suite of language-learning, literacy, and brain fitness solutions consisting of software products, Web-based software subscriptions, online and professional services, audio practice tools, and mobile applications. Rosetta Stone’s current market capitalization is approximately $361 million. The company generated $192 million in sales for the LTM ending September 30th, 2017. (RST is a holding across all funds.)

Please see below for the transcript of the most recent earnings call where I spoke with CEO John Hass:

We believe RST is growing intrinsic value in Lexia at about $4.00 per share per year, and Lexia alone is worth $12-13 per share in 2018. Our low-end, sum of the parts, distressed valuation now is $24 (using 1x sales for Consumer, Enterprise, and K-12 Language, which is a -75-80% discount to M&A multiples). Using this valuation is not reasonable as Rosetta Stone Consumer brand is known by 80% of Americans (250 million people), Duolingo is doing rounds at 20x revenue or a $800 million valuation with $40 million in sales, Rosetta Stone grew subscribers 11% quarter over quarter to 417,000. Enterprise signed the largest deal in company history for 10,000 seats and $1 million a year from a global Fortune 500 company.

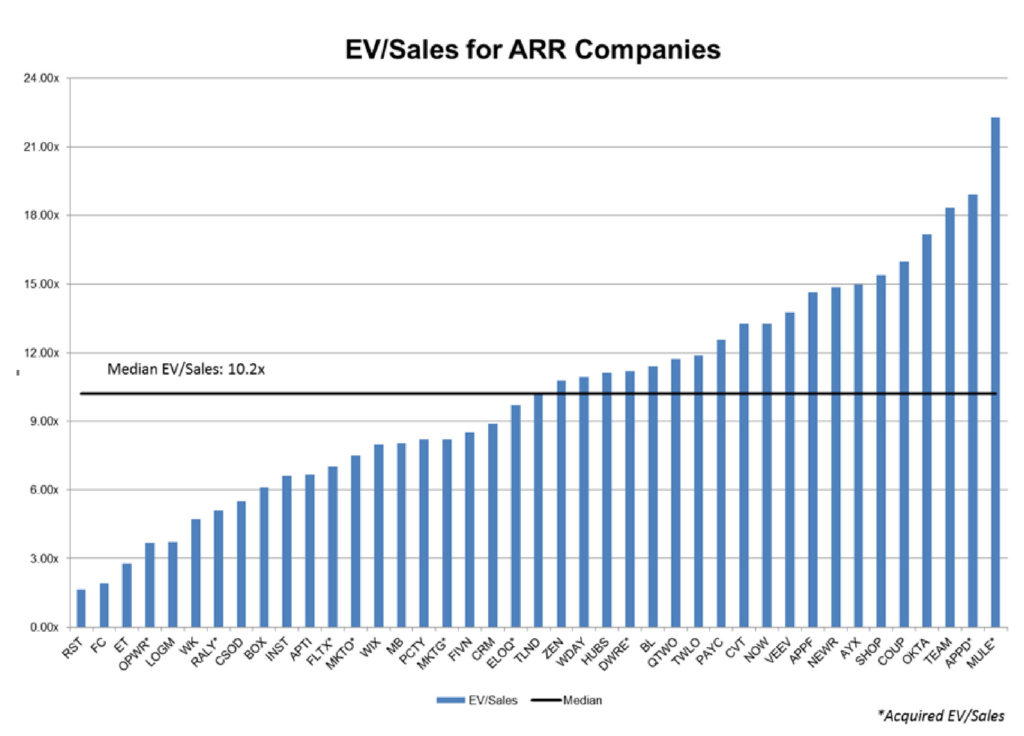

Shown below are Annual Recurring Revenue business models (typically software) with usually 80%+ gross margins, 90%+ annual renewal rates, and typically substantial growth. At first glance, the valuations seem quite high, but given these are very sticky, high margin, high growth businesses we believe these valuations are not unreasonable.

We added FC as the company’s All Access Pass has 85% gross margins and 90%+ annual renewal rates, with substantial growth. RST and FC are the two lowest valued businesses on our chart below.

Rosetta Stone continues to hire strong talent with the most recent hires from Amazon, Microsoft, Gartner group, and iTutorGroup. Jerry Huang was formerly the Global COO of iTutorGroup with a $1 billion+ valuation, and recently joined Rosetta Stone to expand internationally. iTutorGroup had 25,000 tutors in 80 countries. Both the online tutoring and international expertise should really help RST. [link]

Rosetta’s Seattle Office made some key hires and is growing very nicely[2]:

• Christine Chambers, VP of Finance, joined Rosetta Stone from RealNetworks and also worked previously for the Bill & Melinda Gates Foundation.

• Roya Salehi, VP of literacy customer success has been an executive at education companies Achieve3000 and Kaplan;

• Greg Spils, VP of product for the language division, worked at Microsoft, Amazon, Rhapsody and Shazam before joining Rosetta Stone in March;

• Dan Holmes, senior VP of global sales and marketing, spent 14 years at research and consulting powerhouse Gartner.

______

[1] Market price as of the date of dissemination of the letter

[2] https://www.geekwire.com/2018/beyond-yellow-box-rosetta-stone-reinventing-help-growing-seattle-office/

Certain factual and statistical (both historical and projected) industry and market data and other information contained herein was obtained by Osmium Partners from independent, third-party sources that it deems to be reliable. However, Osmium Partners has not independently verified any of such data or other information, or the reasonableness of the assumptions upon which such data and other information was based, and there can be no assurance as to the accuracy of such data and other information. Further, many of the statements and assertions contained herein reflect the belief of Osmium Partners, which belief may be based in whole or in part on such data and other information. The information contained herein is provided for informational purposes only. This is not an offer to sell, or a solicitation to buy, limited partnership interests in Osmium. An investment in Osmium is not suitable for all investors. Graphs/charts are provided for illustrative purposes only and should not be relied on to form an investment decision. Stocks mentioned in the newsletter do not constitute a recommendation to buy or sell the individual securities.

Update on Dundee: Steep Discount to Intrinsic Value, CEO We Trust

September 20, 2018 in Equities, Ideas, LettersThis article is excerpted from a letter by MOI Global instructor Jim Roumell, partner and portfolio manager of Roumell Asset Management (RAM), based in Chevy Chase, Maryland. Jim is a valued participant in The Zurich Project.

(Note: All figures in Canadian dollars)

Dundee reported a loss of $1.34 per share and NAV of $8.70 per share in the second quarter (down from $10.01 as of 3/31/18). The company is continuing to focus on repositioning its overall investment portfolio. CEO Jonathan Goodman stated that what was once a portfolio of about 100 investments is current at approximately 75 with a goal to get down to a manageable 30 in the not-to-distant future. The company has been unambiguous that everything in the portfolio is up for sale at the right price. That is, there are no sacred cows.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Disclosure: The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients, and the reader should not assume that investments in the securities identified and discussed were or will be profitable.

The Case for Europe – Myths vs Reality

September 19, 2018 in Commentary, Europe, European Investing Summit 2018, MacroThis article is authored by MOI Global instructor Stuart Mitchell, Investment Manager at S.W. Mitchell Capital, based in London.

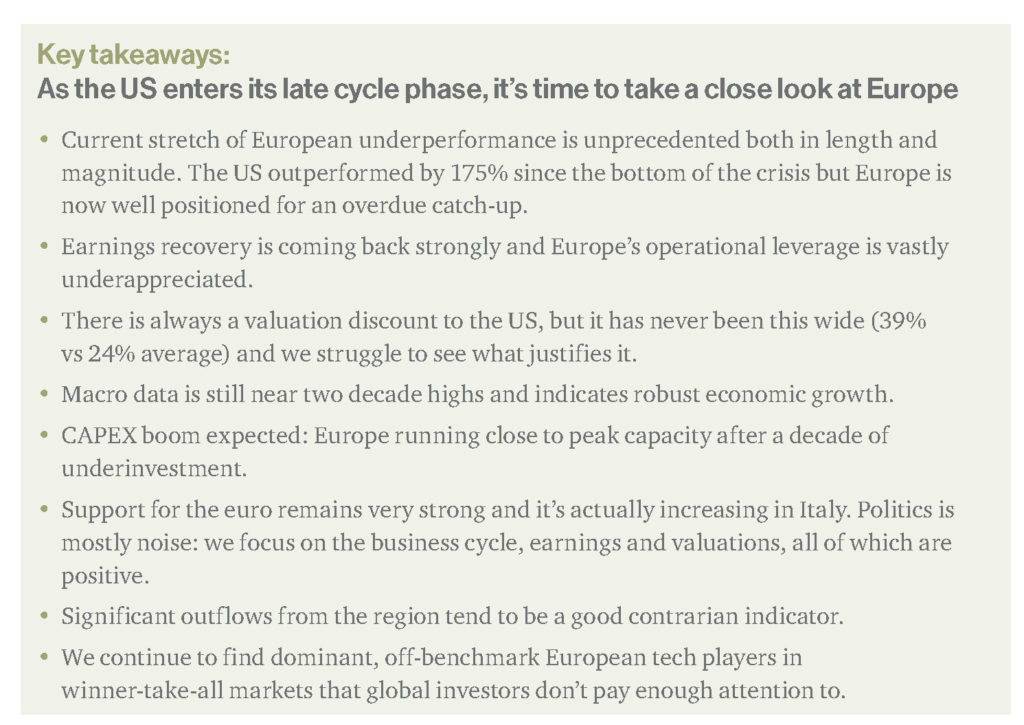

Over the last few weeks we met with a series of US investors to discuss why we believe the current opportunity in European equities is uniquely compelling. While on the one hand we’re seeing unprecedented interest in our strategies, we realize that many misperceptions still linger about Europe. Our goal for this piece is to recap our recent conversations and highlight why we think the outlook for European equities is the brightest it has been in over a decade.

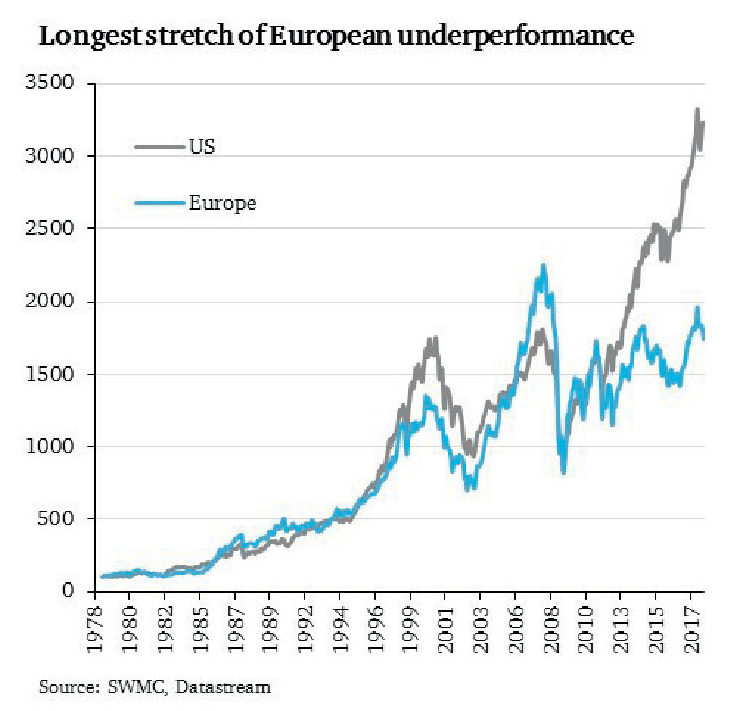

Myth: Europe always underperforms the US.

Reality: Not true historically and the current stretch of underperformance is unprecedented.

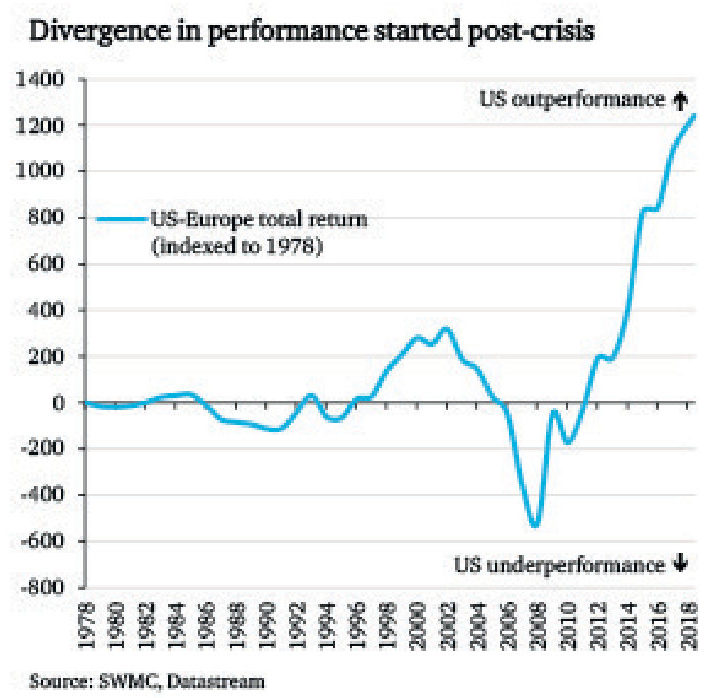

Europe and the US have moved in lockstep for decades and the stretch of significant European underperformance since the 2008 financial crisis is highly atypical.

However, even if we include the crisis, in dollar terms European equities outperformed the S&P 500 in 8 out of the last 15 calendar years.

Over the long term, during years of outperformance Europe is on average 13% ahead of the US.

Myth: European earnings are not growing as fast as the rest of the world.

Reality: No longer true and the operational leverage of the region remains underappreciated.

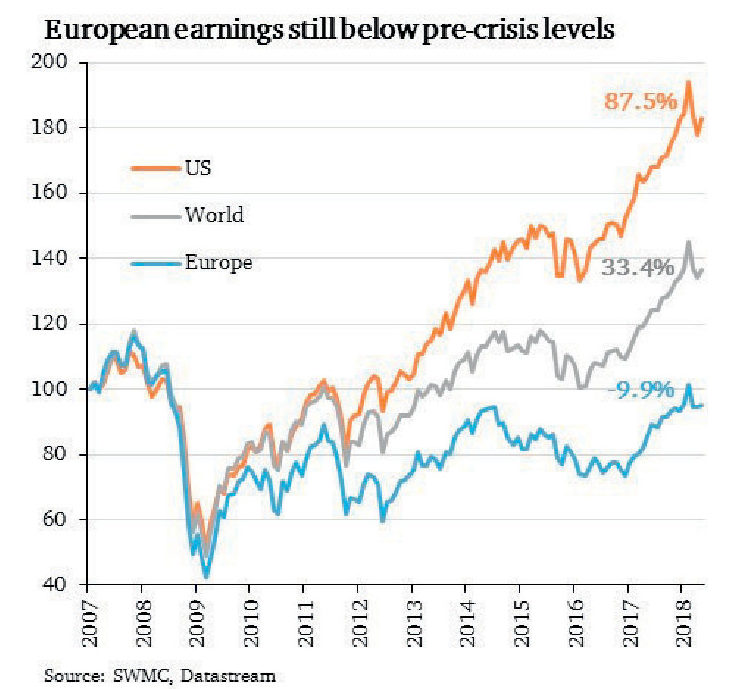

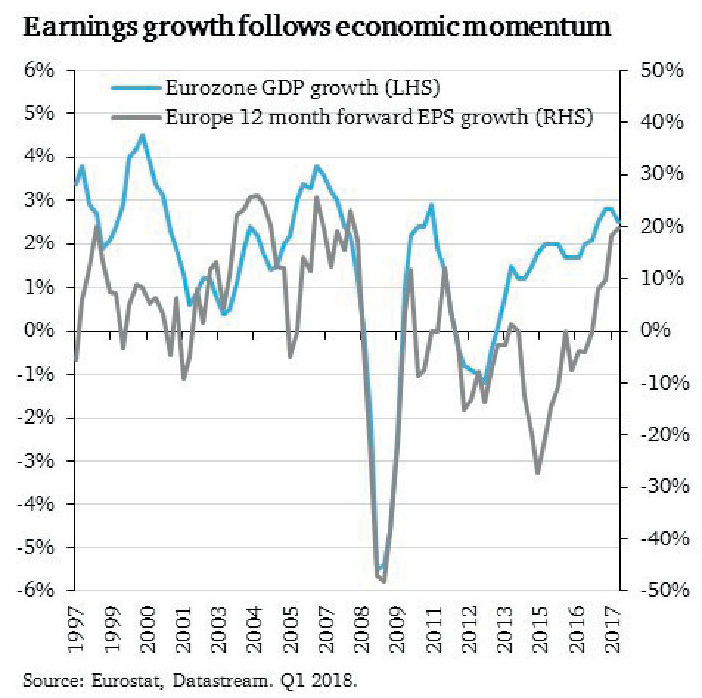

The earnings argument is valid, but backward looking. We believe that the single biggest reason for Europe’s post-crisis underperformance relative to the US has been the lack of earnings recovery.

From the bottom of the crisis (March 2009), US equities returned 290%, whereas Europe is only up 115%. During the same time European earnings doubled, but US earnings almost quadrupled.

European earnings are still below pre-crisis levels, while the US is nearly 90% higher and the rest of the world also grew 33%.

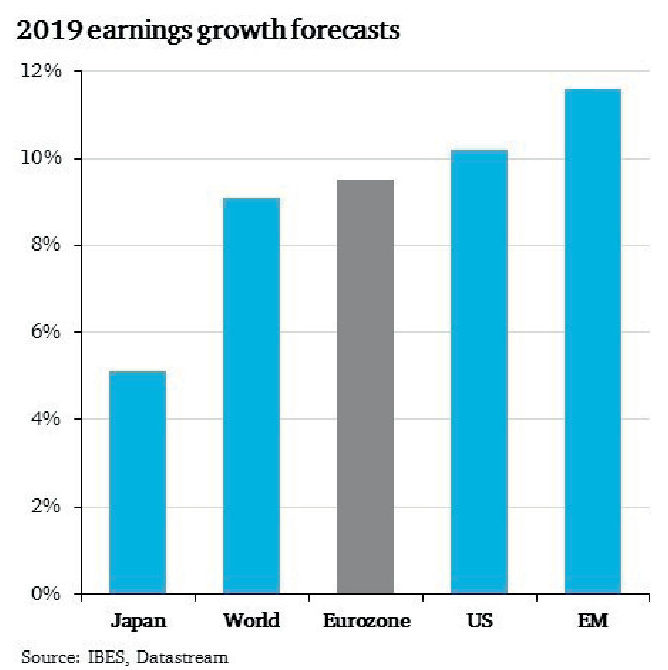

Looking ahead, analyst consensus now expects European EPS to grow at a similar rate to the rest of the developed world, at around 10% in 2019.

We think there is significant upgrade potential to these consensus numbers, based on what we are seeing in our own portfolio from a bottom up perspective and what macro data suggests.

Historic data and current operational leverage implies a 6x earnings multiplier on GDP growth, which should result in EPS growth closer to 15%.

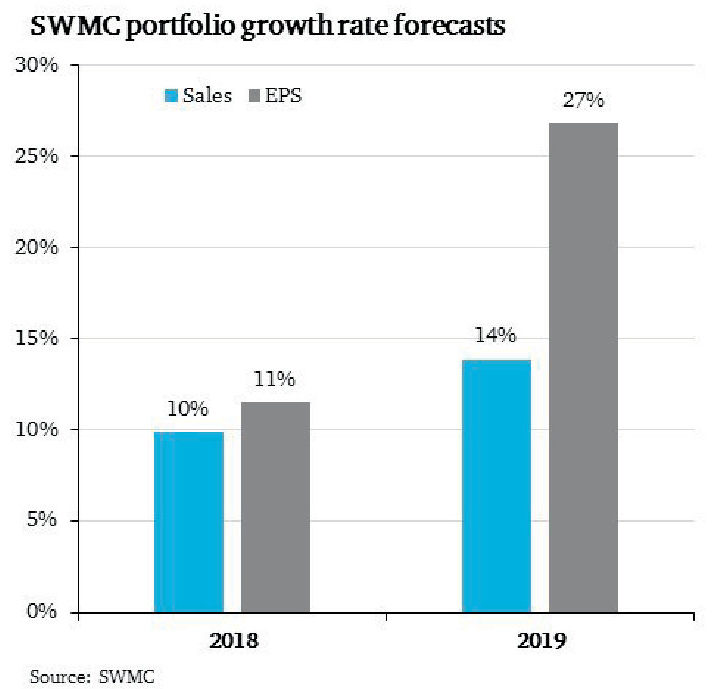

We are seeing a particularly strong earnings inflection in 2019 in many of our value- oriented names.

At the same time the rapid growth of our technology related names is showing no signs of deceleration.

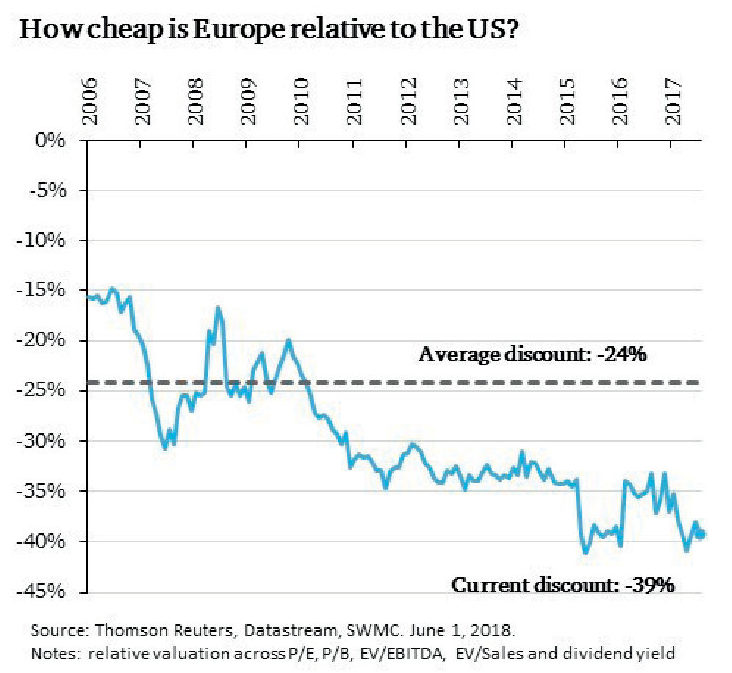

Myth: Europe is always trading at a discount to the US.

Reality: Yes, but the current discount is well above average and close to the widest on record.

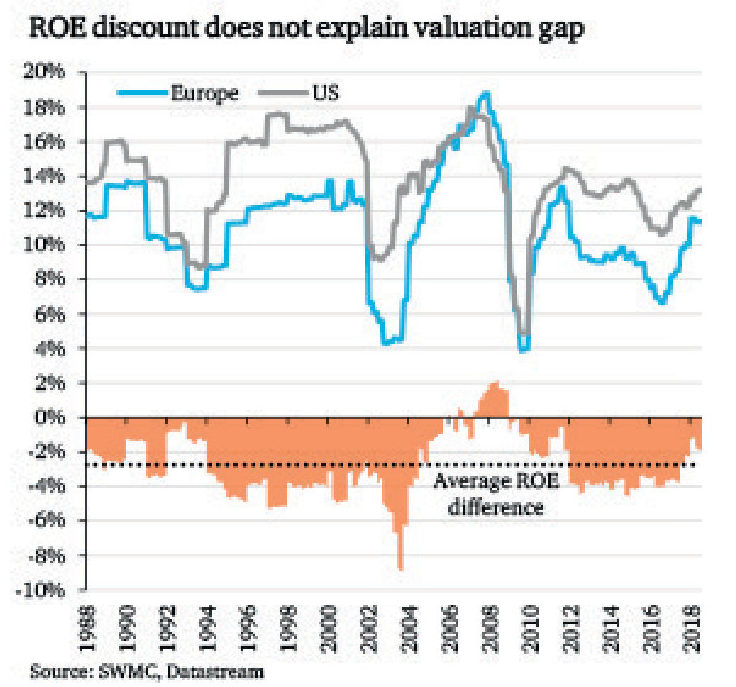

Investors are aware that Europe is trading at a discount to the US, and the usual reaction is that the US valuation premium is justified given higher growth, higher margins and better return on equity.

While we agree that some discount to the US is warranted, we are finding it very hard to explain why Europe is trading close to the deepest historic discount, while earnings are expected to grow at the same pace as the US and the margin and ROE gaps are actually narrower than their long-term averages.

We believe that as soon as operational leverage starts showing in Europe next year, a significant valuation rerating can take place.

A rerating to the average historic discount alone would offer 50% upside from current levels.

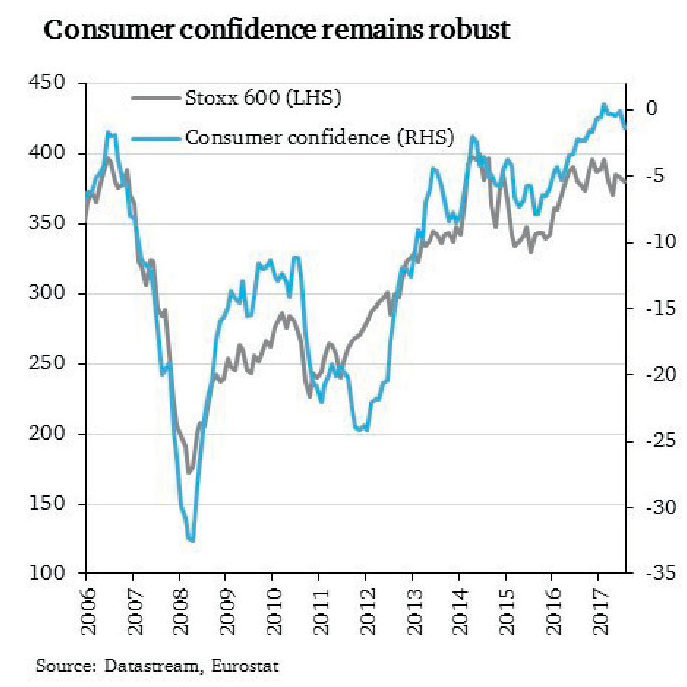

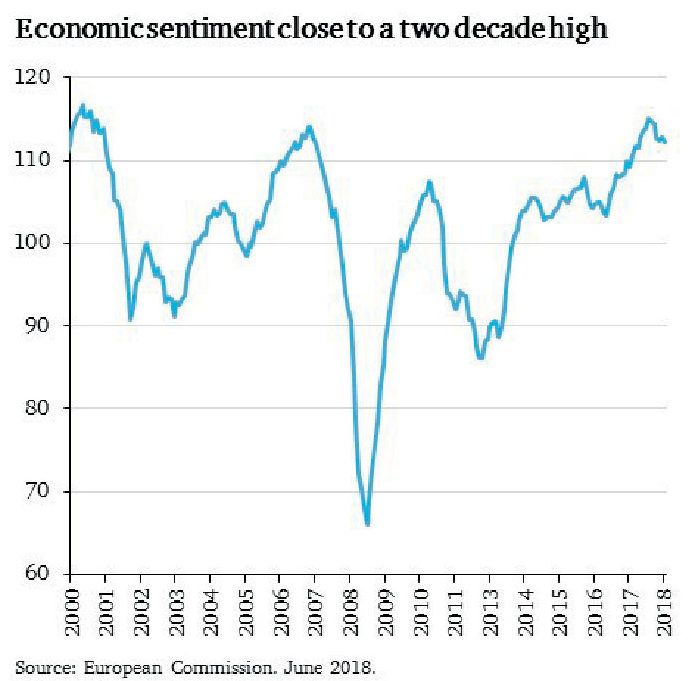

Myth: The recovery in European economies is running out of steam.

Reality: Macro data still near two decade highs and supportive of robust growth.

Across both hard and soft data European macro continues to impress.

In our view, the only thing that has slowed is the rate of change, and while growth is no longer accelerating (from a low base), the most recent readings of PMIs, retail sales, industrial production, credit growth, unemployment, and the

European Commission’s broader economic sentiment indicators all point to robust GDP growth for the next 24 months.

Consumer confidence remains at a two decade high and we see no reason why the market should not rerate to a level implied by the consumer’s bullish outlook.

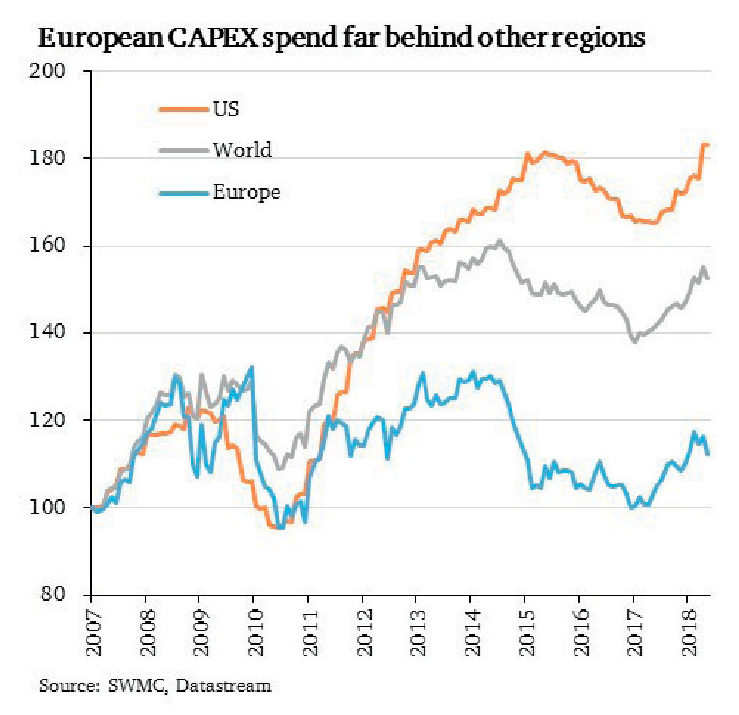

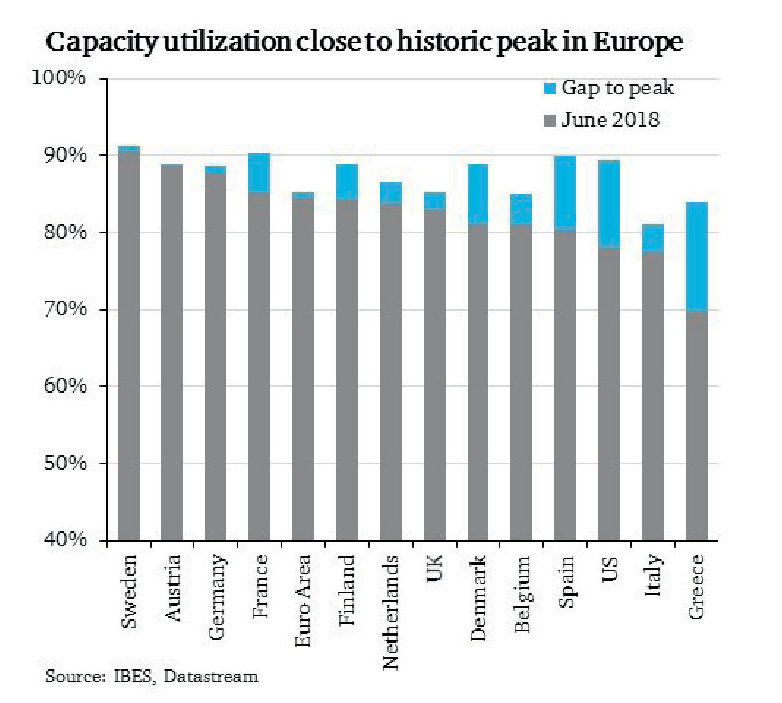

Myth: CAPEX remains muted – European CEOs are concerned about the outlook.

Reality: Capacity utilization is nearing peak levels and there’s strong pent-up demand from a decade of underinvestment.

Capital expenditure has indeed stagnated in Europe post-crisis on both an absolute and a relative basis.

The reason we believe that spending will pick up in the next 12 months is that many industries are now close to full capacity. This is something we picked up on in our conversations with executives over the last year and we’re now seeing it reflected in official data as well.

Tight labor markets and increasing automation are also supportive of a CAPEX boom.

The pent-up demand from a decade of underinvestment cannot be met overnight – we think we’re at the beginning of a multi-year spending cycle that should add further support to the already robust economic growth on the continent.

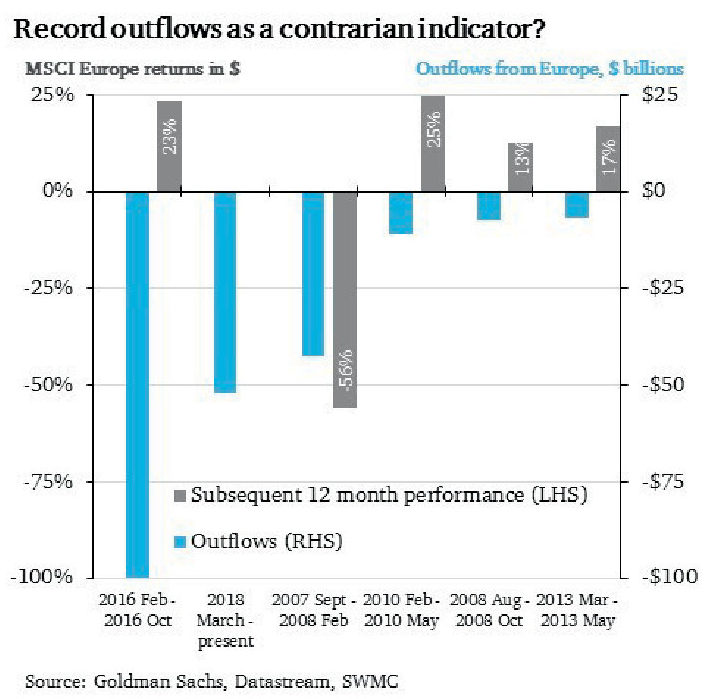

Myth: Outflows are a leading indicator of poor performance.

Reality: The 5 largest streaks of outflows were followed by positive returns outside 2008.

Since March we have now seen 18 weeks of consecutive outflows from Europe, totalling more than $50bn.

This is the second largest outflow streak on record behind 2016, when $100bn was pulled from Europe over 38 weeks.

It is worth noting, however that outside the financial crisis in 2008, the 5 largest streaks of outflows were followed by strong positive returns over the next 12 months.

Even on a relative basis, today’s levels of outflows have subsequently seen Europe outperform by 5% on a six month view.

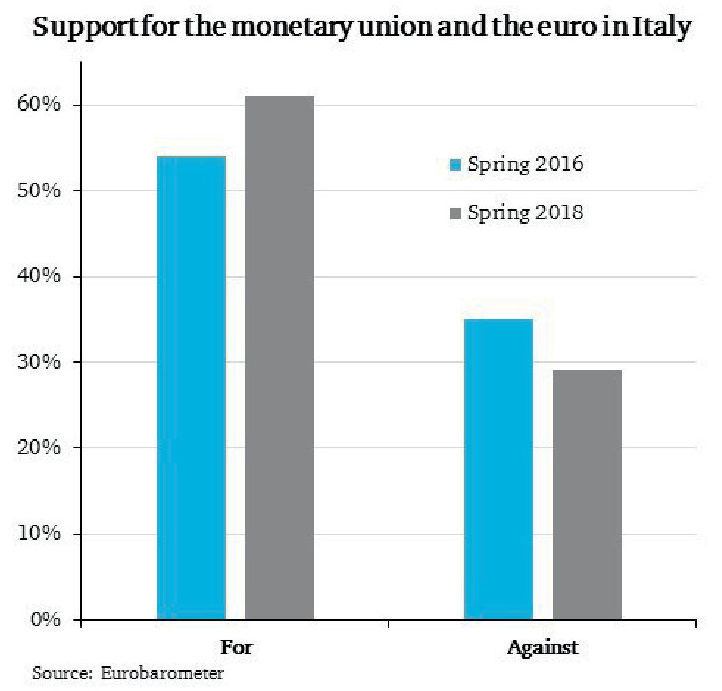

Myth: Italy is on the verge of leaving the euro and causing the collapse of the currency union.

Reality: Support for the euro has increased in Italy and there’s room for macro surprises.

The Italian election created significant volatility over the last few months as the market struggled to understand the implications of a government led by the two main populist parties (Five Star Movement and Northern League).

We closely monitored the evolution of the Italian coalition’s economic and political priorities and were pleased to see that many of the more extreme policies that each party included in early manifestos – such as a referendum on the euro – have been abandoned.

In our view, the shift from such a polarizing idea made perfect sense, as the majority of Italians is in favor of the euro and the monetary union. In fact, support for the common currency has strengthened over the last few years.

Italians also understand that their own savings, overwhelmingly held in euro denominated debt products, would be at huge risk should they abandon the common currency. Such a risk was never part of the Brexit referendum.

We believe that the populist shift in Italy does not present real systemic risk, and some of the more unorthodox proposals of the government could even offer a much needed boost to the stagnant Italian economy.

The core features of the government’s program are tax cuts and a universal income for Italy’s poorest households, both of which have the potential to lift Italian economic activity in the near term.

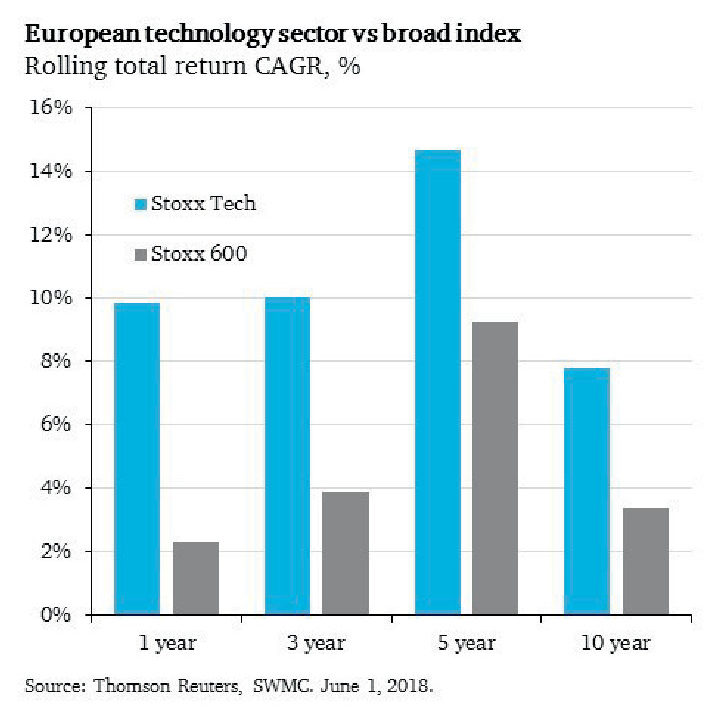

Myth: Technology dominates market performance but Europe is structurally underexposed.

Reality: True for the index, but not for our strategy. Tech has been the biggest contributor to our outperformance.

A frequent pushback against European equities is that the region has been unable to produce any dominant, global technology winners over the last few decades, while the US and China have generated trillions of dollars in shareholder value through innovative companies like the FANG stocks and emerging markets giants like Tencent and Alibaba.

While there is merit in this argument, we think the issue is more nuanced and highlights the danger of equating a region’s equity market with its market cap-weighted index.

The ascendancy of technology stocks has been a key driver of post-crisis global equity market returns. As a result, technology’s weight in the S&P 500 is now 25%, and realistically over 30% based on our calculations that include ‘hybrid’ companies like Amazon. Similarly, in China and EM the index weight of Information Technology is now over 30%.

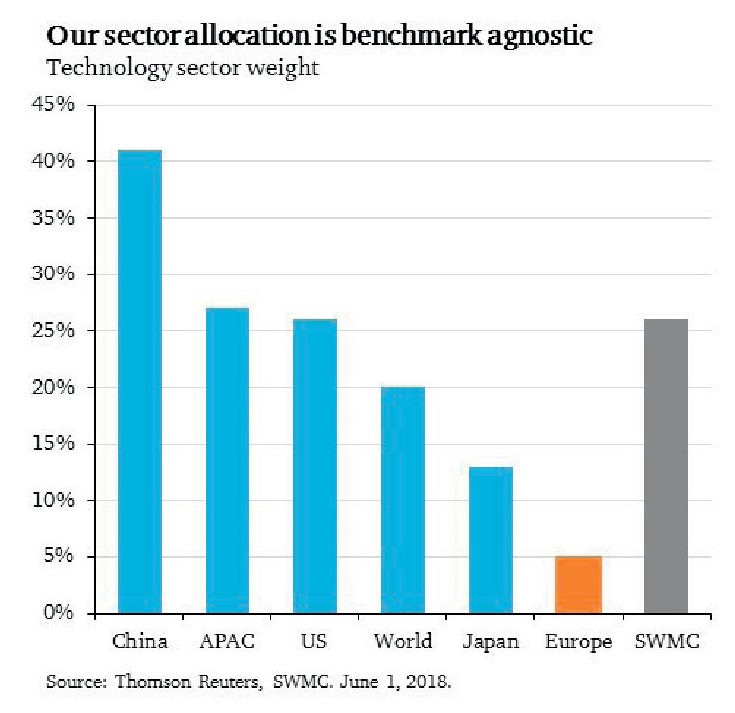

Europe’s Stoxx 600 on the other hand only has a 5% exposure to technology. Just two companies, SAP and ASML, account for almost half of the index weight.

We think this highlights a clear flaw in passive investing, which myopically focuses on investing in the largest companies, regardless of their quality and growth prospects.

Even though European technology stocks have significantly outperformed the market over the last 1, 3, 5 and 10 years, a passive investor benefitted very little from those returns due to their small index weights.

As we are completely benchmark agnostic, our portfolio weights are driven entirely by bottom up stock picking. This approach has resulted in having 13% average exposure to technology over the last 10 years, often through companies not captured by the benchmark. If we add ecommerce and other ‘hybrid’ companies that straddle technology and other traditional sectors, our average exposure moves closer to 20% and our current allocation is 26%.

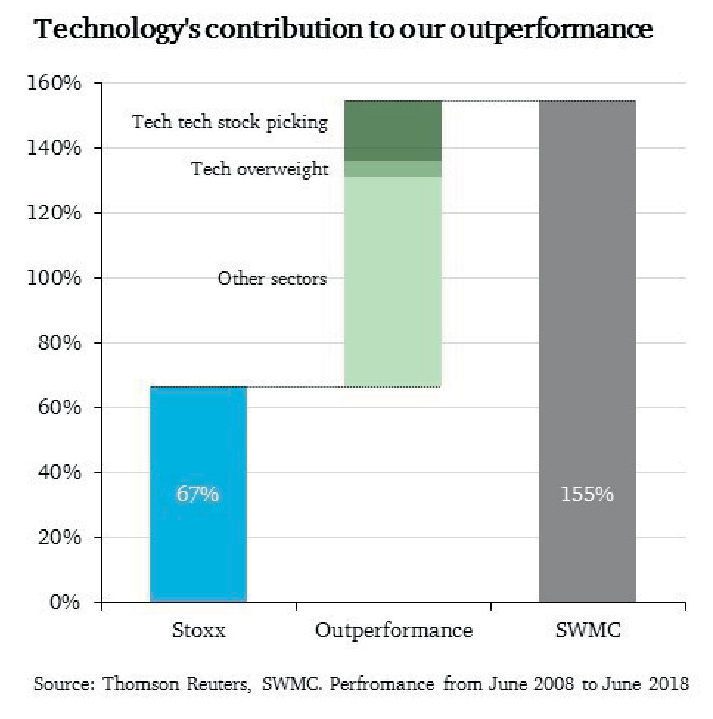

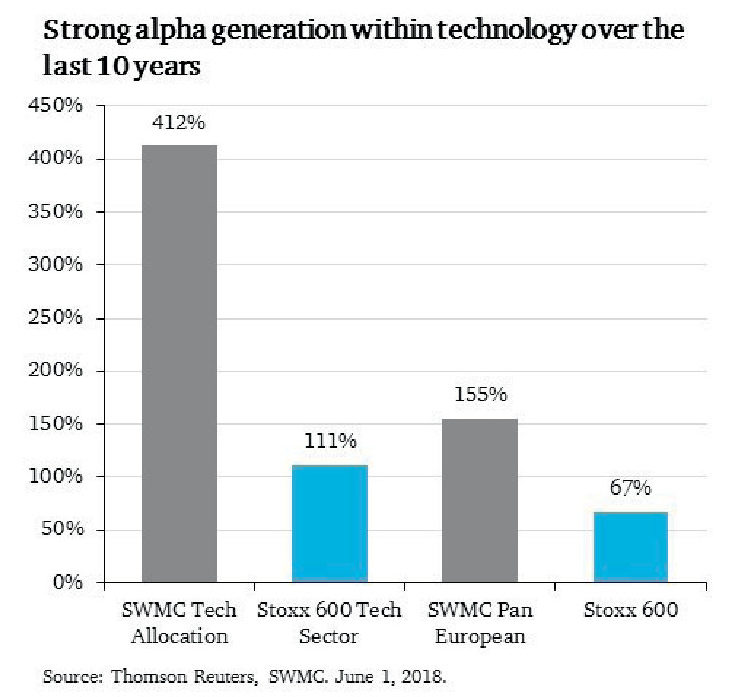

Having almost three times the index’s exposure to technology has tremendously benefitted our investors over the last decade. On a rolling 10-year basis our Pan European strategy generated 155% in gross returns, compared to 67% for the benchmark.

Information Technology has been the top contributor to our 89% outperformance, with roughly 24 percentage points of relative returns. It is important to highlight that our overweight allocation only accounts for 5 percentage points of that, and the bulk of our outperformance comes from stock selection within tech, which added a further 19 percentage points.

The benefit of an active approach is easy to see: while the index returned 67%, the tech sector of the benchmark was up 115%, and by ignoring index weights and constituents and investing only in the most innovative companies, our tech bucket outperformed by almost 4x, delivering 412% during the same 10-year period.

We have a very strong pipeline of potential new tech positions and there plenty of European companies that embody some or all of the key characteristics we look for in tech investments: dominant position in a winner-take-all market that’s favourably positioned on the adoption curve, unique IP, and strong network effects.

This thought piece is a confidential communication issued by S. W. Mitchell Capital LLP and is for information only. It was prepared by S. W. Mitchell Capital LLP only for, and is directed only at persons that qualify as Professional Clients or Eligible Counterparties under the FCA rules, including appropriate institutional investors and intermediaries. It is not intended for the use of and should not be relied on by any person who would qualify as a Retail Client. No person receiving a copy of this newsletter may copy it for transmission to another person. This document has been prepared from sources which are believed to be accurate, however in producing it S. W. Mitchell Capital LLP may have relied on information obtained from third parties and accepts no liability for the accuracy or completeness of such information. It is the responsibility of every person reading this document to satisfy himself as to the full observance of the laws of any relevant country, including obtaining any government or other consent which may be required or observing any other formality which needs to be observed in that country. Past performance should not be seen as an indication of future performance and will not necessarily be repeated. The value of investments and the income from them may fall as well as rise and is not guaranteed. The investor may not get back the original amount invested. Changes in rates or exchange may cause the value of investments to fluctuate. S. W. Mitchell Capital LLP is a Limited Liability Partnership registered in England No. OC312953. Registered address 38 Jermyn Street, London SW1Y 6DN. Regulated and authorised in the UK by the Financial Conduct Authority. The material provided herein has been provided by S. W. Mitchell Capital LLP and is for informational purposes only. S.W. Mitchell Capital LLP serves as investment sub-adviser to one or more mutual funds distributed through Northern Lights Distributors, LLC member FINRA/SIPC. Northern Lights Distributors, LLC and S.W. Mitchell Capital LLP are not affiliated entities.

This article is authored by MOI Global instructor Ori Eyal, Founder and Managing Partner of Emerging Value Capital Management.

This white paper emerges from conversations that I have been having on longevity with Guy Spier, Maya Elhalal and others. It presents my current thinking on this topic. While it’s pretty clear to me that many of us (or at least our children) will most likely live for 1,000 years or more, my experience has been that even when it comes to intelligent and thoughtful others, this probable reality has yet to dawn on them.

I wanted to set down my thoughts as a way of educating my friends and others within my network for four reasons.

a. To help the reader to understand why extreme longevity is inevitable.

b. To start conversations about the implications of this.

c. To learn from others who might contribute to my knowledge on this topic.

d. To help increase the resources (financial, brain power, political support, etc) that society allocates towards this important goal.

It goes without saying that this paper is the product of my own reading and research. While it has been extensive, it has not been systematic. This paper represents the current state of my evolving understanding of the areas covered. Thus, there are likely to be gaps in my knowledge and understanding of many of the topics.

With this in mind, to the extent that you have thoughts, comments and suggestions, please don’t hesitate to email me: [email protected], and I will incorporate them into an updated version of this document and recirculate.

Why We Will Live For At Least 1,000 Years (And Probably More)

My thesis is that medical technology will develop ways to reverse and repair the accumulated damage in our bodies that we call “aging”. Doing so will also prevent the various illnesses of aging such as cancer, diabetes, alzheimer’s and heart disease. While our technological progress will be punctuated and irregular, each advance will incrementally extend our human lifespan. For most of us, these advances should be sufficient, each time, to increase out lifespan long enough to allow time for the next advance, such that our healthy lifespan should be, effectively, infinite (but let’s call it 1,000 years).

Explanation

While this may be a startling claim, I hope to show you that it is not at all unreasonable and ultimately inevitable.

We start with the claim that the human body is just a machine. Indeed, an extraordinarily complex one, but at the end of the day, a machine that is subject to the same universal laws of physics, mechanics, chemistry and biochemistry. In other words, there is nothing mystical or magical about how the human body works.[i]

Given sufficient technology, knowledge, time and resources, there is nothing, in principle, that will prevent us from maintaining the human body in the same way that we can maintain other machines. And in the same way that any other machine, given the right care and replacement parts, can be maintained forever, so can our human bodies.

When viewed in this way, we can understand medicine as simply a form of highly complex engineering applied to the human body. Once we have mastered the relevant technologies and techniques, the challenges will not be insurmountable.

Indeed, medicine is rapidly transforming into information science. This is a process which started with gene sequencing and has moved on to new technologies like iPS cells and CRISPR – where we are increasingly mastering our ability to synthesize the tools and materials we need. Moreover, as more and more of medicine becomes information science, it will benefit from exponential, rather than linear, progress.[ii]

Understanding Aging

The best way to understand aging is to consider it a gradual accumulation of different types of damage in the body.

In order to understand the concept of accumulated damage, let us use the analogy of a laptop computer. When it is new, the hard drive is mostly empty, it has few programs installed and runs rapidly and faultlessly. But over time, the hard drive gets filled up and fragmented, more and more software gets activated on startup, malware and spyware creep in, the registry gets cluttered, etc. Moreover, dust enters the casing, the cooling fan slows down and the springs in the keyboard get worn out.

These are all forms of “accumulated damage” which result in the laptop becoming slow and faulty. After accumulating all this damage, we can say that the laptop has “aged”. Many aspects of the laptops functionality degrade until it succumbs to old age (too much accumulated damage) and dies.

When it comes to a laptop, we understand how to rejuvenate it: we can de-fragment, or reformat the hard-drive, or even replace it. We can add and replace memory and faulty keys – or even the whole keyboard. We can reinstall the operating system from scratch and remove unneeded software. We can use an anti-virus program to remove malware. And we can even replace and upgrade the CPU and/or the motherboard. In doing so, we can stop and even reverse the aging of the laptop, and can, in principle, keep it running forever.

Similarly, the illnesses of aging are either caused by, or are a direct manifestation of damage accumulated in the human body. For example: Heart disease is mostly caused by the accumulation of plaque in the arteries. If we were able to remove that plaque, we would largely remove heart disease. Similarly, Alzheimers is believed to be mostly the result of accumulated junk in and between brain cells as well as the loss of neurons. All of these forms of accumulated damage are, in principle, reversible.

Aubrey de Grey [iii] and others have already identified the seven types of accumulated damage in the human body that we call “aging”. He has also identified plausible methods by which medical science, or medical engineering will be able to stop and reverse all of these seven types of accumulated damage. Researchers are already working on methods and cures to stop and reverse all these.

For example, one type of accumulated damage is the gradual loss of cells over time. This can, in principle, be repaired by introducing embryonic stem cells into the target areas of the body. Extensive research and development is already being done in this area. Another type of accumulated damage is the accumulation of junk between the cells of the body. This type of accumulated damage can, in principle, be repaired by teaching the body’s own immune system to attack and eliminate this accumulated junk.

Strategies To Combat Aging

Once we understand that aging is essentially the accumulation of damage at the organ, cellular and molecular level within our bodies, four interconnected strategies become apparent to combat aging:

1. Slowing down the accumulation of damage in the body

2. Reducing, delaying or bypassing the effects of accumulated damage in the body

3. Repairing the accumulated damage in the body

4. Replacing body parts that have accumulated too much damage

All four strategies are already being pursued in parallel. Because they are interconnected, it is likely that success and progress on any of the four strategies will help inform and promote progress on the other three strategies. From my reading and analysis, I believe that only strategy #3 will lead to an indefinitely long healthy lifespan – sadly this strategy receives, by far, the fewest research dollars. It is my hope that this whitepaper will help drive more money and resources towards strategy #3 possibly via donations to the nonprofit leading this type of research – www.sens.org.

Conclusion

Over the next few decades, medical science – increasingly called medical engineering will provide ways to both stop and reverse the accumulation of damage in the human body that we call aging. As a result, healthy life expectancies will increase rapidly until reaching the tipping point where healthy life expectancy increases by more than one year every year at which point death due to aging becomes improbable. If we exclude horrific dystopian futures such as a global nuclear war, or similar overwhelming disasters, I see no credible future scenario where an essentially infinite healthy lifespan for humans does not happen.

The only significant uncertainty from my perspective is timing.

Objections or Q & A

1. New medical developments will be available only for the super-rich:

Like all new technologies, new medical solutions will rapidly filter down from the rich to the middle class to the poor as economies of scale reduce costs.

2. Progress may take much longer than we expect.

Initially, progress may well be slower than what we expect and our lives might end before sufficient progress is achieved.

But the predictions above have significant margin of safety.

• A lot of research is already being conducted in this area[iv]

• As mentioned before, medicine is becoming an information/ engineering science subject to exponential progress.[v]

• We are making progress on other technologies which will also help – including nanotechnology, artificial intelligence, artificial organs and others.

• Incremental progress will increase lifespan, buying more time for more progress.

• We ourselves can accelerate progress by donating money to sens.org and similar foundations and by voting for leaders that support scientific research and progress.

• Lastly, as progress is made and more people realize the truth of this thesis, an enormously large amount of society’s resources will be allocated towards these goals.

3. Extending life span beyond 120 and reversing aging may be an “all or nothing” endeavor.

Until we can stop and repair all seven types of accumulated age related damage in the human body and cure all age related diseases, making partial progress may be of limited value since it just means something else will kill us soon after. For example, it has been argued that curing cancer would only add about 3 years to the average human lifespan as those that would have died from cancer end up dying from some other age related illness soon after.

• This is possibly true but does not break the thesis, just delays it.

• We are already working on methods to stop and revere all seven types of accumulated damage and curing all age related diseases.

• Age 120 seems to be the age where we are likely to suffer from all age related illnesses simultaneously. In other words, at age 120 most humans would suffer from terminal cancer, terminal Alzheimer’s, terminal diabetes, terminal heart disease, etc all at the same time. Therefore, breaking beyond the 120 age limit may indeed be all-or-nothing. However, extending healthy lifespan up to 120 is probably not all-or-nothing with partial progress having meaningful life extending impact.

• For myself and many others, age 120 is still a long time away – thus there should be sufficient time to make progress on all fronts.

• Partial and even limited progress on all fronts will buy us more time to make further progress.

4. Radically extending lifespan will cause severe problems of overpopulation, social unrest, mass unemployment, pollution, water shortage and other problems

• As life expectancy increases, birth rates will rapidly decline.

• We are well on the way to solving energy, water, pollution, food and other problems via advanced technology. Once these issues are solved, overpopulation will no longer be a problem. The earth can sustainably host tens of billions of humans.

• Mass human unemployment is inevitable due to the rise of AI, regardless of lifespan extension. With universal basic income, this becomes a positive as humans are freed from the bondage of working to survive and can, instead, devote their time to leisure activities.

[i] Several early readers of this whitepaper have tried to argue that the human brain is somehow “magical” or beyond the laws of physics. There is zero evidence to support such claims.

[ii] http://www.kurzweilai.net/the-law-of-accelerating-returns

[iii] https://www.amazon.com/Ending-Aging-Rejuvenation-Breakthroughs-Lifetime/dp/0312367074

[iv] http://www.sens.org/

[v] https://singularityhub.com/2016/10/26/medicine-will-advance-more-in-the-next-10-years-than-it-did-in-the-last-100

NOTA DEL EDITOR: El siguiente texto es obtenido de una carta de Solventis EOS.

* * *

El refrán “Hasta el cuarenta de mayo, no te quites el sayo, y si junio es un ruin, hasta el fin” nos advierte que no retiremos la ropa de abrigo de nuestros armarios, ya que el frío y la lluvia pueden sorprendernos incluso en el mes de junio. Al igual que el tiempo nos desconcierta en ocasiones, hay personas que también lo hacen, y éste es el caso del señor Donald Trump, nacido casualmente un mes de junio.

El máximo mandatario de Estados Unidos se caracteriza por no dejar a nadie indiferente, tanto con sus palabras, como con sus acciones. Si en 2017 fue Corea del Norte y su ansiada reforma fiscal, este 2018 han sido las relaciones comerciales. Empezando por China y terminando por Europa. A este último lo ha atacado en uno de los pilares de la economía, en un sector que emplea a 12 millones de trabajadores y representa el 4% del PIB: la automoción. ¿Resultado de esta política? Diversas reducciones de previsiones (“Profit Warning”) de Daimler [ETR: DAI], Osram [ETR: OSR] o ElringKlinger [ETR: ZIL2]. Esta situación nos ha afectado directamente al representar el sector auto un 12% de la cartera, principalmente en dos nombres: Renault [EPA: RNO] y Peugeot [EPA: UG]. A pesar de ello, tan solo vemos que puede afectar a Renault, por la parte que tiene en Nissan [TYO: 7201], pero no en Peugeot, ya que no vende nada en Estados Unidos. ¿y que hemos hecho? Pues incrementar nuestra exposición en Renault un 1% hasta el 4%. Pensamos que una guerra comercial provoca una situación que no es de equilibrio, ya que ambas partes pierden (el famoso dilema del prisionero de Nash).

Pero además, a precios actuales, y haciendo una suma de partes, hace que nos regalen el negocio automovilístico, tanto Renault como en Peugeot.

Continue reading »

Ed Wachenheim on Investing with a Contrarian Mindset

September 15, 2018 in Audio, Diary, Latticework, Latticework New York, Podcast, TranscriptsWe continue our superinvesting series with insights from Edgar Wachenheim III, chairman of Greenhaven Associates, a firm Ed founded in 1987. Greenhaven had assets under management of more than $9 billion as of early 2024, having handily beaten the major market indices over nearly four decades. Ed is also the author of Common Stocks and Common Sense.

In this rare fireside chat, held at MOI Global’s Latticework summit in 2018, Ed shares timeless insights into the art of contrarian, value-oriented investing. This approach, while neither popular nor particularly exciting, has served Ed and his investors spectacularly well over several decades. In a get-rich-quick world that ultimately fails to deliver, Ed has succeeded in building massive wealth slowly and methodically over time.

Ed spoke about his investment philosophy with fellow fund manager and MOI member Saurabh Madaan, founder of Manveen Asset Management and former managing director of Markel Corporation.

The audio recording is a special episode of the Latticework Podcast.

Members, log in below to access the restricted content.

Not a member?

Thank you for your interest. Please note that MOI Global is closed to new members at this time. If you would like to join the waiting list, complete the following form:

Click here for much more on Ed Wachenheim’s investment philosophy.